If I want early retirement without a bare-bones budget or a luxury target, Chubby FIRE may sit in the middle.

For many U.S. households, that may mean:

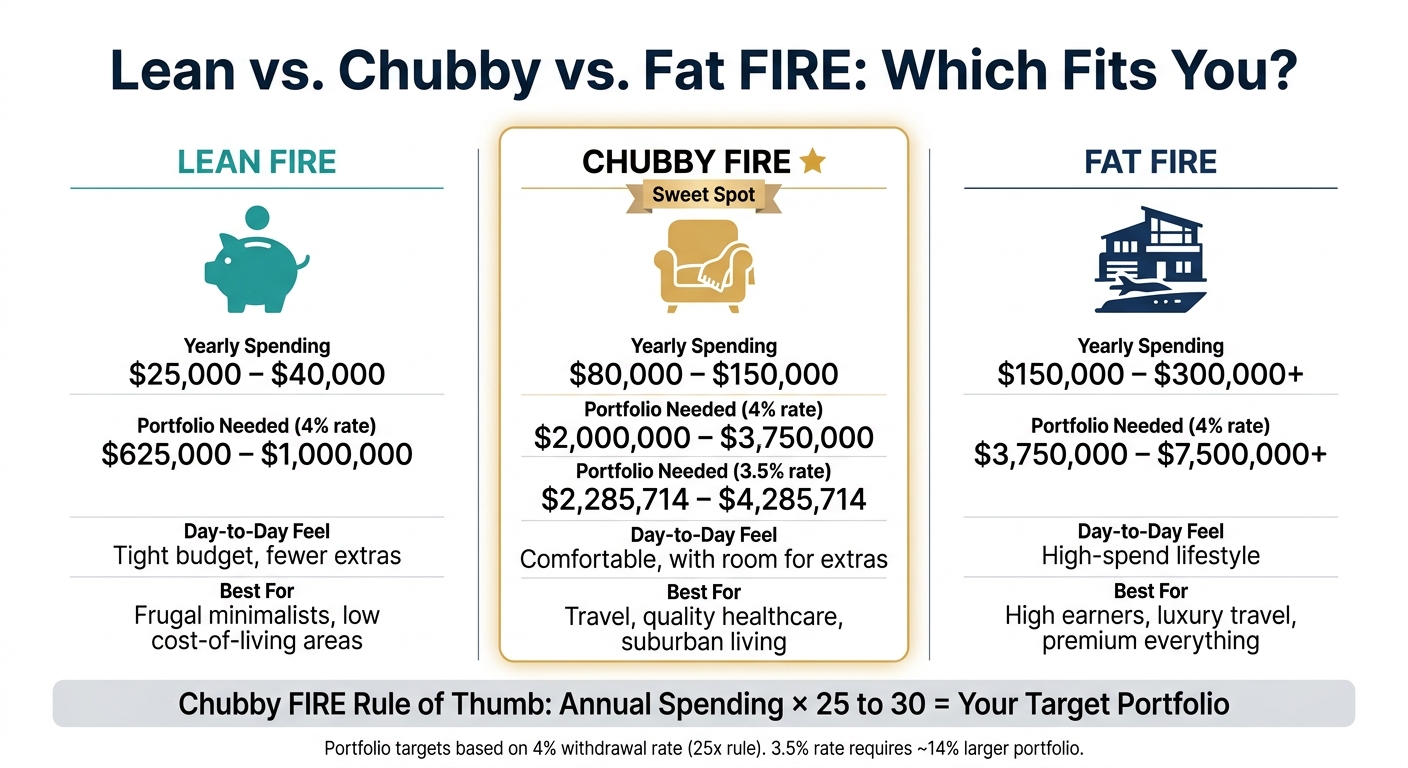

- spending about $80,000 to $150,000 a year

- building roughly $2 million to $3.75 million at a 4% withdrawal rate

- aiming closer to $2.86 million for $100,000 a year at a 3.5% rate

- keeping about 10% to 15% of spending flexible for weak market years

- planning around big cost items like housing, healthcare, taxes, and location

Here’s the short version: Chubby FIRE may offer more room than Lean FIRE for travel, healthcare, and housing choice, but it may stop short of the higher spending tied to Fat FIRE. The tradeoff is simple: a more comfortable budget may call for a bigger portfolio, more tax planning, and a longer runway.

Lean vs Chubby vs Fat FIRE: Spending, Portfolio & Lifestyle Compared

Is Your FIRE Number TOO High? (Can You Retire Earlier?)

Quick comparison

| FIRE style | Yearly spending | Portfolio at 4% | Day-to-day feel |

|---|---|---|---|

| Lean FIRE | $25,000–$40,000 | $625,000–$1 million | Tight budget, fewer extras |

| Chubby FIRE | $80,000–$150,000 | $2 million–$3.75 million | Comfortable, with room for extras |

| Fat FIRE | $150,000–$300,000+ | $3.75 million–$7.5 million+ | High-spend lifestyle |

A simple way to think about it: cover the fixed bills first, then add a comfort layer that may be cut if markets turn bad. That framing may make Chubby FIRE easier to test before I attach a number to it.

How to set your Chubby FIRE spending target

Build a realistic annual budget for early retirement

Start with what you spend today. Track your actual expenses for three to six months, then adjust from there. Add costs that retirement may bring, like more travel, more complete health coverage, or hobbies you’ve put off. Subtract job-related costs you may no longer have. That adjusted total becomes the spending side of your FIRE target.

Most Chubby FIRE budgets tend to fall into three broad ranges:

| Budget Level | Annual Spending | What It Covers |

|---|---|---|

| Entry Chubby | $60,000–$80,000 | Comfortable living in moderate-cost areas |

| Classic Chubby | $80,000–$120,000 | Regular travel and comfortable housing in many U.S. suburbs |

| High-End Chubby | $120,000–$150,000+ | Upper-middle-class comforts in higher-cost metros |

A $120,000 budget may look something like this: 28% housing, 15% travel, 12% food, 12% healthcare, with the rest going to transportation, hobbies, and a buffer.

How housing, healthcare, and location change your number

Two budget items may affect your target more than almost anything else: housing and healthcare.

On the housing side, a paid-off home may give you a big edge. It may lower your fixed monthly costs in a meaningful way. If you still have a mortgage in retirement, some people aim to keep total housing costs - mortgage, property taxes, insurance, and maintenance - at 25% of their annual budget or less. Add another $10,000 here, and your target portfolio may need to be about $250,000 higher at a 4% rate.

Healthcare before age 65 may be the bigger wild card. Without Medicare, you may be buying coverage through the ACA Marketplace or paying out of pocket. A couple on a Silver plan may pay $10,800 to $18,000 per year before subsidies, and a family of four may run $18,000 to $30,000. Those costs may climb over time, so some people build inflation into the plan. Add another $10,000 here, and the target portfolio may also need to be about $250,000 higher at a 4% rate.

Location may matter just as much. A $120,000 budget may go much further in Boise than in San Francisco. Moving from a high-cost state like California or New York to a no-income-tax state like Texas, Florida, or Washington, or to another lower-cost area, may reduce the FIRE number you’d need over a long retirement.

These spending categories often shape the budget more than anything else, so they tend to set up the portfolio math that comes next.

Split fixed expenses from flexible spending

Once you have a budget number, split it into two buckets: fixed and flexible.

Fixed expenses are the harder-to-cut items, such as property taxes, basic insurance, utilities, and groceries. Some people try to keep these at 25% of the total budget or less. Flexible spending includes categories you may scale back without changing day-to-day life too much, like international travel, fine dining, club memberships, and luxury hobbies.

That split may give you more room in a weak market. Instead of cutting across the board, you may trim the flexible bucket and leave your core lifestyle mostly intact. Keeping discretionary spending separate also makes stress-testing easier. You may model a downturn, cut only the flexible side, and see whether the plan still appears workable.

Once the budget is split this way, the withdrawal-rate math tends to get simpler. Use this spending total as the input for your Chubby FIRE number.

How to calculate your Chubby FIRE number

Start with 25x to 30x your annual spending

A common starting point is to multiply your annual spending target by 25. That lines up with a 4.0% baseline withdrawal rate. Some people use 28x to 30x instead if they want more room for a retirement that may last 40 to 50 years.

For many Chubby FIRE plans, 25x may be the floor, not the finish line. If your target spending is $100,000 per year, that may point to roughly $2,500,000 to $3,000,000 in investable assets.

Compare 3.0%, 3.5%, and 4.0% withdrawal rates

The multiplier you use may depend on how much uncertainty you want to build into the plan.

| Annual Spending | 4.0% Rate (25x) | 3.5% Rate (28.6x) | 3.0% Rate (33.3x) |

|---|---|---|---|

| $80,000 | $2,000,000 | $2,285,714 | $2,666,667 |

| $100,000 | $2,500,000 | $2,857,143 | $3,333,333 |

| $120,000 | $3,000,000 | $3,428,571 | $4,000,000 |

| $150,000 | $3,750,000 | $4,285,714 | $5,000,000 |

Moving from 4.0% to 3.5% may require a 14% larger portfolio for the same spending level. For a lot of Chubby FIRE setups, 3.5% may feel like the middle lane - more conservative than 4.0%, but not as heavy a lift as 3.0%.

There’s also a tax angle that the table doesn’t show. Your withdrawal plan may need to be based on pre-tax withdrawals, not just net spending. So if you want $100,000 after taxes, you may need to pull $120,000 or more, depending on your mix of accounts and your tax picture.

Account for sequence risk and a long retirement

Sequence-of-returns risk may matter most in the first five years. If markets drop hard early in retirement, you may end up selling investments after prices fall just to cover day-to-day spending. Even if markets recover later, that early hit may leave the plan in a weaker spot.

Some households deal with this by keeping spending flexible. If you may trim $10,000 to $30,000 of optional spending during a downturn - like travel or high-end upgrades - you may avoid selling as many assets at a bad time. A 1- to 2-year cash buffer may also help during a rough patch by reducing the need to tap invested assets right away.

That’s one reason many Chubby FIRE households end up around a 28x to 30x planning number. The extra margin may make the plan hold up better if the early years don’t go smoothly.

Once the target is set, the next step may be figuring out which accounts to draw from first.

Build the portfolio and tax plan that supports Chubby FIRE

Once your spending target is set, the next step is building a portfolio and withdrawal plan that may support it.

Choose a diversified portfolio that fits your spending risk

A Chubby FIRE portfolio may need to balance growth for a 40- to 50-year retirement with enough stability to limit early drawdown risk. Many Chubby FIRE households diversify beyond U.S. large-cap stocks to include international developed markets, small-cap value, and REITs. Those additions may reduce concentration risk.

Hidden concentration is a common issue. If you hold several funds with similar holdings, you may own more of the same underlying companies than you think. That may matter even more if your portfolio also includes employer stock or other concentrated positions.

Portfolio structure matters. But withdrawal order may shape how much tax drag you end up keeping.

Plan withdrawals across taxable, traditional, Roth, and HSA accounts

Before Social Security and RMDs begin, some households use lower-income years to bridge spending and complete Roth conversions. For a $3.5 million portfolio at age 55, a rough split may look like this:

| Account Type | Target Range | Primary Role |

|---|---|---|

| Taxable Brokerage | $700K – $1M | Bridge funding before 59½; ACA income management |

| Traditional IRA / 401(k) | $2M – $2.5M | Main asset base; Roth conversion source |

| Roth IRA | $500K – $700K | Tax-free income smoothing |

| HSA | $50K – $100K | Healthcare-specific spending |

In the early years, taxable accounts may serve as the bridge. In 2026, long-term capital gains for married couples filing jointly are taxed at 0% up to $94,050 in taxable income, so careful sales from a taxable account may be more tax-efficient than many people expect.

Moving money from a traditional IRA into a Roth while you're in the 12% or 22% bracket - before Social Security and RMDs push income higher - may reduce your lifetime tax bill. HSAs offer tax advantages and may be one of the most tax-efficient vehicles for healthcare costs in early retirement.

Another number to watch is the Medicare IRMAA threshold. In 2026, single filers with MAGI above $109,000 and joint filers above $218,000 face higher Part B premiums. Roth withdrawals do not count toward MAGI, which may make them useful for staying under that line.

Cross-account visibility may make these decisions easier to carry out.

Use Mezzi to check readiness and spot tax issues

Here’s the hard part: your 401(k), IRA, Roth, HSA, and taxable accounts usually live at different institutions. That makes it tougher to see the full picture.

Mezzi connects accounts across institutions, pulls allocation and tax exposure into one place, and flags overlap, Roth conversion opportunities, tax-loss harvesting candidates, and wash-sale timing. From there, it gives you a consolidated view of your Chubby FIRE readiness based on your actual balances. And if you sell a position to harvest a loss, Mezzi will flag when the 30-day wash sale window has cleared so you can rebuy without triggering a disallowed loss.

Conclusion: Is Chubby FIRE right for you?

Chubby FIRE may fit best if your spending sits between lean and fat. Think of it in two layers: a fixed base for housing, healthcare, food, and transportation, plus a comfort layer that you may trim if markets weaken. That buffer may matter more than luxury. It gives you room to cut spending in rough years without scrambling, which may make the plan more resilient when returns are uneven.

At $100,000 per year, Chubby FIRE may call for about $2.5 million using a 4% withdrawal rate or $2.86 million using 3.5%.

Chubby FIRE may still involve tax planning, though often less than Fat FIRE. Two of the bigger day-to-day risks may be lifestyle creep and healthcare costs. If you retire before Medicare eligibility, a couple using the ACA Marketplace may spend $10,800 to $18,000 per year on premiums alone.

A simple stress test may help: can you point to $10,000 to $30,000 you’d cut in a bad market year without changing daily life?

FAQs

How do I know if Chubby FIRE fits my lifestyle?

Chubby FIRE may make sense for people who want more room in the budget without going to either extreme.

It sits between lean, tightly managed early retirement and a more upscale version with far higher spending. In plain English: you may want comfort, a cushion, and a lifestyle that still leaves room for things like travel, dining out, and hobbies - without tracking every dollar all the time.

A few factors may shape whether it fits:

- Your current spending

- How much of that spending is discretionary

- Where you plan to live

- Whether you prefer more security over retiring as fast as possible

A typical Chubby FIRE budget may fall in the $80,000 to $150,000 per year range. That level of spending may be tied to a portfolio of about $2 million to $3.75 million.

Should I use a 3.5% or 4% withdrawal rate?

For Chubby FIRE, many people prefer 3.5% instead of the standard 4% rule.

The 4% rule may still serve as a starting point. But early retirements often last 40 to 50 years, and over that kind of time frame, a 4% withdrawal rate may have a lower success rate.

Using 3.5% may add more safety and comfort. The tradeoff? It also may mean needing a larger portfolio - typically about 14% more than a 4% approach.

How much should I budget for healthcare before Medicare?

Before Medicare at age 65, healthcare may be one of the bigger moving parts in a retirement budget.

For a single person, annual costs may land around $5,400–$8,400 with subsidies, or $12,000–$20,000 without them.

For a couple, full-price coverage may run $18,000–$30,000 per year.

ACA subsidy eligibility may also be tied to your Modified Adjusted Gross Income (MAGI). In some cases, keeping MAGI low enough for subsidies - including through Roth withdrawals - may reduce healthcare costs by a meaningful amount.

Disclosures:

• This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

• Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

• Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.