If I donate long-term appreciated stock to a donor-advised fund before selling it, I may avoid federal capital gains tax on the gain and may still claim a charitable deduction if I itemize. That setup may work best for shares held over one year in a taxable brokerage account, not for short-term shares or positions sitting at a loss.

Here’s the short version:

- Best fit: long-term appreciated stocks, ETFs, and mutual funds in a taxable account

- Main tax angle: I may avoid up to 23.8% federal tax on embedded gains in some cases

- Deduction rule: I may deduct fair market value if IRS rules are met and I itemize

- Limit to know: stock gifts to a DAF are generally capped at 30% of AGI; cash is generally 60%

- Timing rule: the shares may need to arrive at the DAF by December 31, 2026 for a 2026 deduction

- Big mistake to avoid: if I sell first and donate cash after, the capital-gains edge may be gone

- When cash may be better: short-term shares and losing positions may call for different handling

A simple example from the article shows why the asset choice may matter: a $25,000 cash gift and a $25,000 stock gift may produce the same income-tax deduction, but the stock gift may also avoid tax on a $20,000 gain. In that case, the gap may be about $4,760.

Donating non-cash assets to a donor-advised fund | Fidelity Charitable

Quick Comparison

| Funding method | Capital gains tax on built-in gain | Deduction amount | AGI limit | Fit |

|---|---|---|---|---|

| Cash | None tied to the gift | Cash amount donated | 60% of AGI | Simpler giving, loss positions sold first |

| Long-term appreciated stock | May be avoided if donated before sale | Fair market value, if rules are met | 30% of AGI | Large unrealized gains in taxable accounts |

In other words: the same dollar gift may lead to a different tax result depending on whether I give cash or shares.

When donating appreciated stock to a DAF makes sense

This approach may fit best with long-term appreciated shares held in a taxable brokerage account for more than one year. In plain English: the best fit may be long-term shares in a taxable account.

Assets that work best: long-term appreciated stocks, ETFs, and mutual funds

Publicly traded stocks, ETFs, and mutual funds are usually the easiest assets to donate. And if the unrealized gain is larger, donating instead of selling may let you avoid more tax.

When choosing which shares to give, some investors start with the lowest-cost-basis lots first. Those shares usually have the biggest built-in gains. You may also use the cash you would have donated to buy the shares back, which may increase your cost basis and may reduce future taxes.

Short-term shares or positions that have gone down in value may follow different tax rules.

When cash or a different asset may be the better choice

If a position has fallen in value, donating it directly may not be the best move. Some investors sell the losing position first, realize the capital loss to offset other gains, and then donate the cash proceeds instead.

Short-term shares held for one year or less usually may not qualify for a fair-market-value deduction. That means they may lose the main tax edge tied to donating stock to a DAF. In those cases, some people donate cash instead.

Once you pick the right shares, the transfer may be mostly paperwork.

How a donor-advised fund transfer typically works

Once you've picked the shares, the transfer itself may be pretty straightforward. You may open a DAF or use one you already have. Before anything moves, check the sponsor's minimum contribution and confirm that it accepts the security you plan to donate.

From there, you would initiate a direct, in-kind transfer from your brokerage account to the DAF. The shares move directly, without a sale. Once the assets arrive in the DAF, the gift becomes irrevocable, and the sponsoring organization takes legal control. You may recommend grants and investments, but the sponsor keeps final authority. Your deduction is triggered in the tax year when the DAF receives the shares. That receipt date also sets when the deduction begins.

The sequencing rule that matters most: donate before you sell

This is the part people tend to watch closely: if you sell first, you may lose the capital-gains benefit.

If you sell the shares yourself and then donate the cash, you may already have realized the capital gain. At that point, the DAF receives cash, not appreciated stock, and the main capital-gains tax edge may disappear.

The transfer needs to be a direct, in-kind move from your brokerage to the DAF before any sale takes place.

Paperwork and account data you will typically need

Transfers often stall for a pretty ordinary reason: missing delivery details. Before you reach out to your brokerage, it may help to have these items ready:

| What you need | Details to gather |

|---|---|

| Your brokerage info | Account registration (name on account) and account number |

| Security details | Ticker symbol or CUSIP, exact number of shares, and which lots to transfer |

| DAF delivery instructions | Sponsor name, DAF account name, DAF account number, and the sponsor's DTC number |

| Transfer form | Signed Letter of Authorization (LOA) or the brokerage's in-kind transfer form |

| IRS documentation | Form 8283 for noncash gifts over $500; written acknowledgment for gifts of $250 or more |

One practical timing note: start the transfer well before year-end, especially if you're hoping to claim the deduction for the current tax year. Processing delays may push the transfer past December 31, and the deduction counts when the sponsor receives the shares.

Those records may determine whether the deduction is allowed and how much you may claim.

Tax benefits, deduction rules, and the limits that affect your outcome

The two tax benefits that matter most

Once the shares reach the DAF, two tax rules may shape the outcome most.

The first involves capital gains tax. Transferring appreciated shares directly to a DAF may let you avoid up to 23.8% federal tax on the gain. Why? You aren't selling the shares yourself, so the gain generally isn't recognized by you.

The second tax rule involves the charitable deduction. If you itemize, you may generally deduct the fair market value of the shares when the DAF receives them, rather than your cost basis.

Here’s the basic idea:

Donating $50,000 of stock with a $20,000 basis may avoid capital gains tax and may produce a larger deduction than selling first and donating cash.

That may sound pretty favorable. But there’s a catch: deduction limits may reduce the near-term tax benefit or push part of it into later years.

AGI limits, carryforwards, and valuation

For appreciated securities donated to a DAF, the deduction is capped at 30% of adjusted gross income (AGI) in the year of the gift. Cash donations are generally subject to a 60% AGI limit instead.

If the gift goes over that 30% limit, the unused amount may carry forward for up to five additional tax years.

A few other rules may affect the final result:

- For 2026 itemized gifts, the first 0.5% of AGI is nondeductible.

- In the top bracket, each $1 of itemized deduction may reduce federal tax by no more than $0.35.

- For publicly traded stock, fair market value is generally the average of the day's high and low quoted prices on the transfer date.

If the deduction may be too large to use in one year, some donors use bunching. That means grouping several years of planned gifts into one DAF contribution. Doing that may make it easier to get past the standard-deduction threshold in a single year.

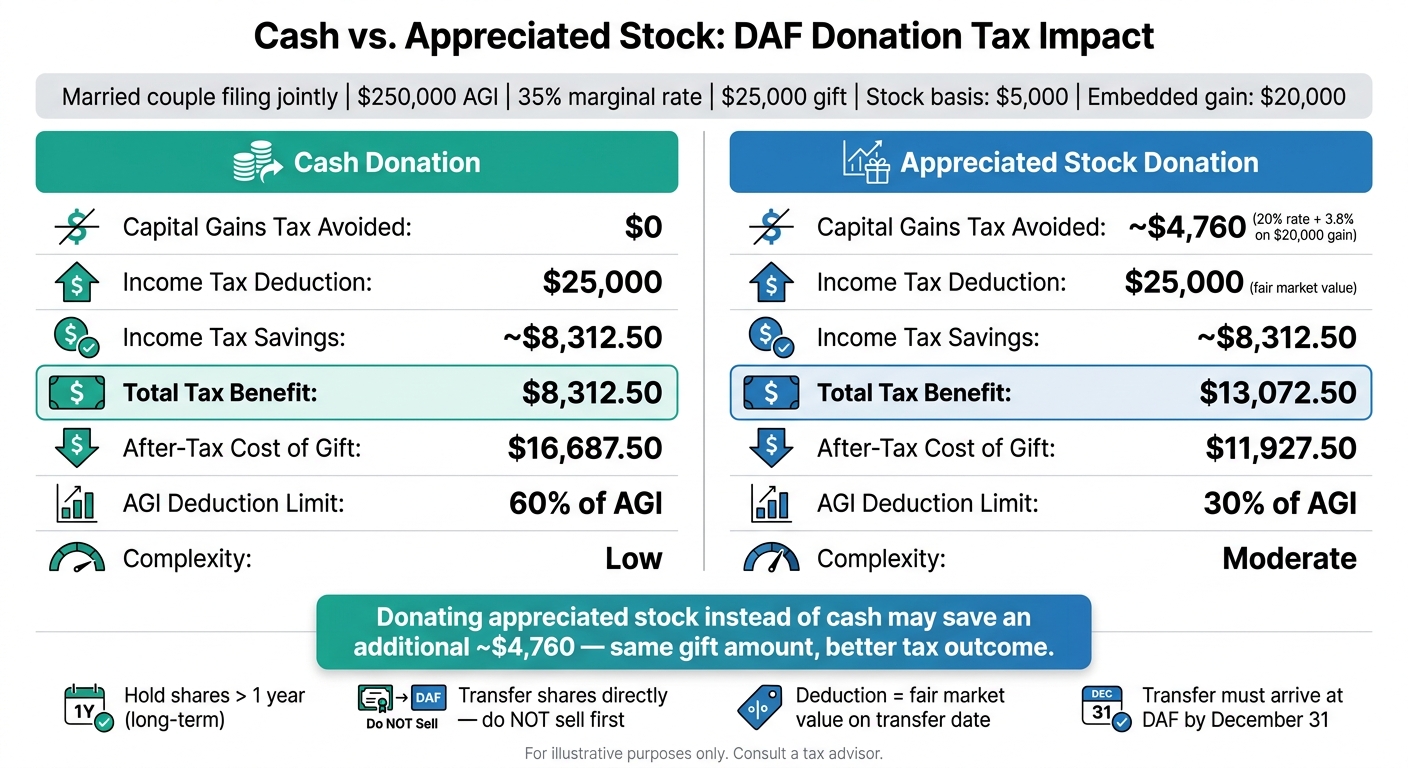

Cash vs. appreciated stock: a side-by-side comparison

Cash vs. Appreciated Stock DAF Donation: Tax Savings Comparison

How you fund a DAF may change the tax result.

Here’s the tax difference at a glance.

| Feature | Cash Donation | Appreciated Stock (Long-term) |

|---|---|---|

| Capital gains tax impact | None | Avoided entirely |

| Deduction basis | Dollar-for-dollar amount | Full fair market value (if held >1 year) |

| Common AGI limit | 60% of AGI | 30% of AGI |

| Administrative complexity | Very low | Moderate (requires brokerage transfer) |

| Best use case | Recurring gifts; loss positions sold first | Highly appreciated long-term holdings |

What the comparison shows

Take a married couple filing jointly with $250,000 of AGI, a 35% marginal tax rate, and stock worth $25,000 with a $5,000 cost basis. That means the shares carry a $20,000 gain.

If they donate $25,000 in cash, no capital gains tax applies because nothing was sold. Their income tax savings from the deduction may come to about $8,312.50. Total tax benefit: $8,312.50. After-tax cost of the gift: $16,687.50.

If they donate the appreciated shares straight to the DAF, the $20,000 gain may never be recognized. That may mean avoiding about $4,760 in federal capital gains tax based on a 20% rate plus the 3.8% NIIT. The deduction may still be $25,000, which matches the cash gift, so the income tax savings may remain about $8,312.50. Total tax benefit: $13,072.50. After-tax cost of the same $25,000 gift: $11,927.50.

That’s a difference of about $4,760 from one choice: which asset gets donated. Same gift amount, different tax result.

Put simply, the asset may matter just as much as the amount.

Conclusion: a short checklist before you transfer shares

Before you move shares, run this final checklist:

- Confirm the holding period. The shares may need to be held long term. Short-term shares may only deduct basis.

- Verify itemizing still beats the standard deduction.

- Confirm the sponsor accepts the security. Publicly traded stocks, ETFs, and mutual funds are commonly accepted. Restricted stock or private equity may not be.

- Check your calendar. Broker-to-broker transfers may take two to six weeks. Leave enough time for the gift to settle by December 31.

Donate before you sell. If you sell first and donate the cash, you may trigger a taxable event and may lose the main tax edge tied to donating appreciated shares.

Use your actual lots, dates, and tax return before you transfer.

FAQs

Can I donate stock from an IRA or 401(k)?

No. You generally may not donate stock held inside an IRA or 401(k) straight to a donor-advised fund. For a stock donation, the shares usually need to sit in a taxable brokerage account first.

If you're age 70½ or older, you may use a Qualified Charitable Distribution (QCD) from an IRA to an IRS-qualified public charity, up to $105,000 per year. A QCD may not go to a donor-advised fund.

How do I know which tax lots to donate?

Focus first on tax lots you've held for more than one year, along with securities that have the largest gains. If you're eligible, that approach may let you avoid capital gains tax on the appreciation while still claiming a deduction for the full fair market value.

It may also make sense to look at whether you might have sold the asset anyway, and how giving it away may affect your long-term portfolio allocation. Before you transfer shares, review your account statements and overall finances with your tax advisor.

What if my stock transfer misses December 31?

If your stock transfer isn’t completed by December 31, you may miss the tax deduction for that calendar year. The deduction is generally based on when the donor-advised fund sponsor legally receives the assets, not when you begin the transfer.

Appreciated securities may take time to process, so waiting until the end of the year may increase the chance of missing the deadline. Some donors coordinate early with their financial advisor or custodian to confirm timing.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.