Want to access your retirement savings before 59½ without penalties? A Roth conversion ladder might be the solution. Here's how it works:

- What It Is: Gradually transfer funds from a Traditional IRA or 401(k) to a Roth IRA over several years. After five years, you can withdraw the converted amounts tax- and penalty-free.

- Why It Works: Avoid 401(k) withdrawal penalties, take advantage of lower tax rates in early retirement, and enjoy tax-free growth in your Roth IRA.

- How to Start: Plan conversions at least five years before you need the funds. Convert manageable amounts each year to stay in lower tax brackets. Pay taxes using outside funds to maximize growth.

This strategy helps early retirees bridge the gap before Social Security or Required Minimum Distributions kick in. Start early, track your conversions, and follow IRS rules to make the most of your retirement savings.

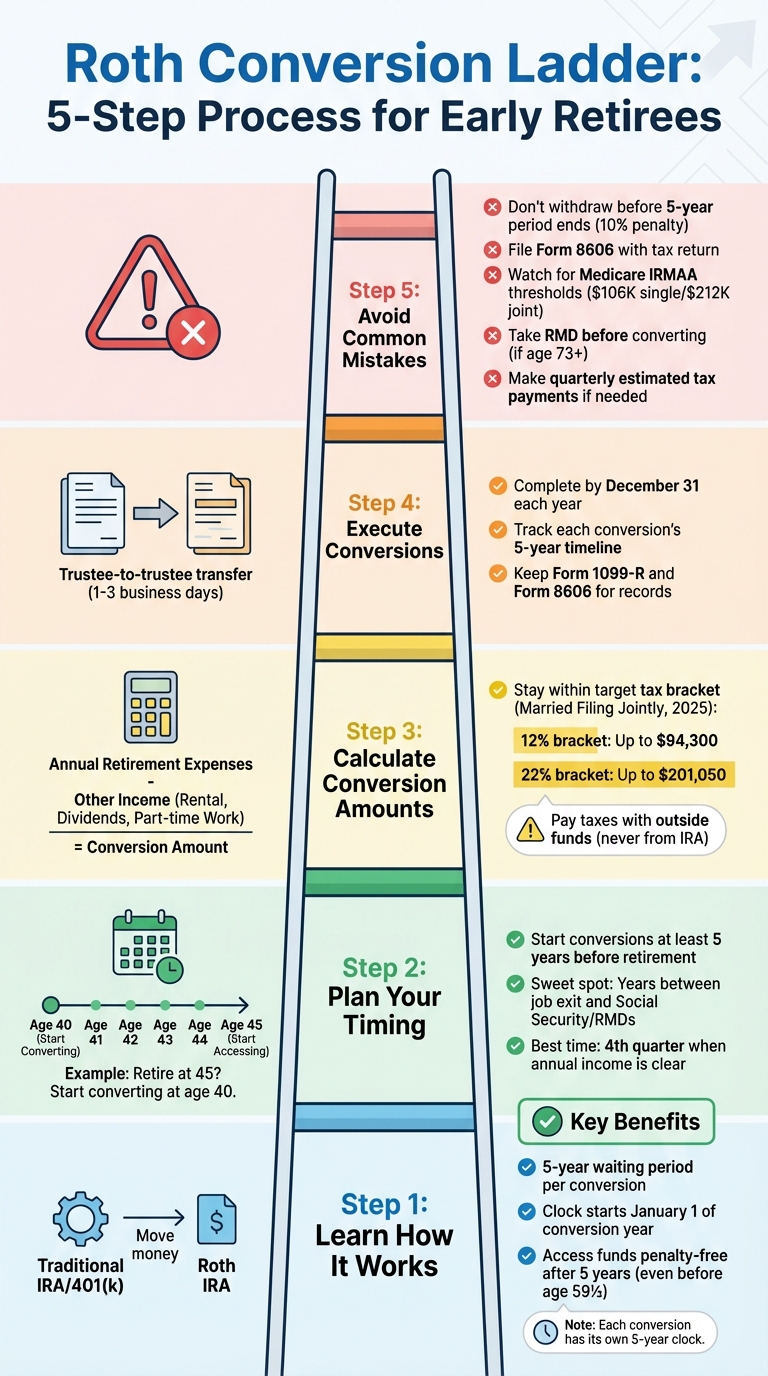

5-Step Roth Conversion Ladder Strategy for Early Retirement

Step 1: Learn How a Roth Conversion Ladder Works

What is a Roth Conversion Ladder?

A Roth conversion ladder is a long-term strategy where you move money from tax-deferred accounts, like Traditional IRAs or 401(k)s, into a Roth IRA over several years. Each time you convert funds, a five-year waiting period begins. After those five years, the converted amount can be withdrawn without penalties, even if you're under 59½.

The IRS has a specific order for Roth IRA withdrawals. First, your contributions are taken out (these are always penalty-free), followed by converted amounts (starting with the oldest), and finally, earnings. This sequence makes it possible to access each "rung" of your conversion ladder in the order you created it.

Timing is everything when it comes to the five-year rule. The clock starts ticking on January 1 of the year you make the conversion, no matter if you complete it in January or December. For example, converting funds in December 2026 means you can access them penalty-free starting January 1, 2031.

| Feature | Traditional IRA / 401(k) | Roth IRA (via Conversion) |

|---|---|---|

| Initial Tax Treatment | Tax-deferred | After-tax (taxed at conversion) |

| Early Access (<59½) | 10% penalty usually applies | Principal penalty-free after 5 years |

| Growth | Tax-deferred | Tax-free |

| RMDs | Required starting at age 73 | None during owner's lifetime |

Grasping these details is key to understanding how the Roth conversion ladder can work as an effective tool for early retirement planning.

Why Use a Roth Conversion Ladder in Early Retirement

For those retiring early, a Roth conversion ladder helps bridge the gap between early retirement and the age when penalty-free withdrawals from retirement accounts become available. For example, if you retire at 40, this strategy can cover the 19 years until you turn 59½.

But the benefits go beyond just avoiding penalties. Early retirement often comes with lower taxable income, especially if you’re not earning a salary or receiving Social Security yet. This creates a prime opportunity to convert funds at lower tax rates. For instance, in 2025, married couples filing jointly can stay within the 12% federal tax bracket with taxable income up to $94,300. These lower rates make conversions during this period particularly appealing.

"Moving funds gradually to a Roth IRA now could mean saving on taxes in retirement." - Renee Collins, CFP and CPA, Retire Ready Inc.

Step 2: Plan When to Do Your Roth Conversions

Understanding the Five-Year Rule

Every Roth conversion you make starts its own five-year countdown. For example, if you convert $40,000 in 2026 and another $40,000 in 2027, each amount comes with its own waiting period before it can be withdrawn without penalties. Importantly, the clock for each conversion begins on January 1 of the year the conversion takes place.

If you withdraw the converted principal before the five-year period ends and you're under 59½, you'll face a 10% early withdrawal penalty. However, once you hit age 59½, this rule no longer applies for penalty purposes, giving you unrestricted access to your retirement funds. This timing is crucial when planning your conversion strategy. For instance, starting a conversion ladder after age 55 may not be as efficient. Funds converted at 55 won’t be penalty-free until age 60 - just six months after you could access traditional retirement accounts without penalties anyway.

The next step is figuring out the best time to begin your conversion ladder based on your retirement timeline.

When to Begin Your Roth Conversion Ladder

Timing your first conversion is key to ensuring penalty-free access when you retire. The strategy revolves around working backward from your planned retirement age. For example, if you want to retire at 45, you’ll need to start your first conversion at age 40 so those funds are available when you stop working. One retiree followed this approach by converting $40,000 annually starting at age 45. By age 50, her first conversion was penalty-free, and over a decade, she had converted $400,000. This method helped bridge the gap to age 59½ while keeping her tax burden manageable.

The years between leaving your job and starting Social Security or Required Minimum Distributions (RMDs) are often the sweet spot for conversions. During this window, your taxable income is typically at its lowest, giving you the chance to convert funds while staying in lower tax brackets. Financial planners often suggest doing conversions in the fourth quarter of the year, as by then, your total taxable income is clearer, allowing you to manage your tax brackets more effectively.

Market conditions can also influence your timing. Converting during a market downturn lets you transfer more shares for the same tax cost, with any future growth happening tax-free in your Roth IRA.

"A Roth conversion ladder is a multiyear strategy to transfer pretax funds to a Roth IRA to kickstart future tax-free growth... you're paying taxes in smaller increments." - Preston Cherry, Founder and President, Concurrent Financial Planning

Step 3: Determine How Much to Convert Each Year

Calculate Your Retirement Income Needs

Start by listing all your expected annual retirement expenses - things like housing, healthcare, groceries, and travel. Then, figure out how much income you'll have from other sources, such as rental properties, part-time work, or dividends. The difference between your expenses and this income is the amount you’ll need to cover with withdrawals from your retirement accounts. This gap becomes the basis for your Roth conversion ladder.

Take Jennifer as an example. In 2025, at age 50, she had $600,000 in her 401(k) and received $25,000 annually from rental income. After applying the standard deduction of $29,200, her taxable income was $0 before any conversions. This allowed her to convert funds while staying in lower tax brackets.

When planning, don’t forget to account for all taxable income sources. For instance, part-time consulting income, interest, or dividends will fill up your lower tax brackets first, before your conversion amount is added. If you’re expecting a large one-time income boost - like selling a house or receiving a bonus - it’s wise to reduce or skip conversions that year to avoid moving into a higher tax bracket.

After identifying your income gap, use it to calculate how much you can convert without pushing yourself into an unfavorable tax bracket.

Stay in Lower Tax Brackets with Your Conversions

Once you know your income gap, focus on converting amounts that keep you within your target tax bracket. This is called a bracket-filling strategy. Subtract your current taxable income from the upper limit of your chosen bracket to determine your conversion cap.

For the 2025 tax year, the 12% tax bracket for married couples filing jointly tops out at $94,300, while the 22% bracket ends at $201,050. Many early retirees aim to stay within these brackets when converting. Jennifer, for example, converted $94,300 annually, filling the 12% bracket and paying about $11,316 in federal taxes each year. Over six years, she successfully converted $565,800, avoiding future Required Minimum Distributions that could have been taxed at rates exceeding 35%. By optimizing her annual conversions, she maintained a tax-efficient strategy for penalty-free withdrawals.

Be mindful of hidden costs that could make your conversions pricier than planned. For instance, Medicare IRMAA surcharges apply if your Modified Adjusted Gross Income (MAGI) exceeds $106,000 for single filers or $212,000 for joint filers in 2025. Additionally, if your MAGI surpasses $200,000 (single) or $250,000 (married), you’ll face a 3.8% Net Investment Income Tax. Even a small conversion over these thresholds can lead to unexpected expenses.

"Most clients don't plan for taxes, so they just assume that they're going to be in a lower tax bracket in retirement." - Renee Collins, CFP and CPA, Retire Ready Inc.

Finally, always pay the taxes on your conversions using cash from regular savings or brokerage accounts - never from your IRA. If you’re under 59½ and use IRA funds to cover the tax, that portion will be hit with a 10% early withdrawal penalty. Using outside cash ensures your Roth account retains its full growth potential, maximizing the benefits of the conversion in the long run.

Step 4: Complete Your Roth Conversion Ladder

Move Funds from Traditional Accounts to Roth IRAs

To start, reach out to your brokerage - whether it’s Vanguard, Fidelity, Schwab, or another provider - and request a trustee-to-trustee transfer from your Traditional IRA to your Roth IRA. Most brokerages simplify this process with a "Convert to Roth" button or an online workflow, which generally takes 1–3 business days to complete. This direct transfer method helps you avoid the 60-day rollover risk and prevents automatic tax withholding, which could complicate your tax planning.

If you're working with funds in a 401(k), you’ll likely need to roll the balance into a Traditional IRA first, unless your employer allows in-plan Roth conversions. Once the funds are in your Traditional IRA, you can proceed with the Roth conversion. To avoid the risks of market timing, consider in-kind transfers, which move your investments as-is, or liquidate them into cash before transferring.

"The more important thing is that you are getting that money into a completely tax-free vehicle with the Roth IRA. You're converting a lower amount, and we all know that the markets will eventually rebound, and all of that growth is going to be captured tax-free." - Ali Swart, CFP, Waldron Private Wealth

When it’s time to pay the conversion taxes, always use funds from outside your IRA - such as cash from savings or a taxable brokerage account. If you're under 59½, using IRA funds to cover taxes could trigger a 10% early withdrawal penalty. To avoid surprises, set aside enough cash for taxes based on your bracket calculations. If your tax liability increases significantly, you may need to make quarterly estimated payments using IRS Form 1040-ES.

Once your conversions are done, the next critical step is tracking your waiting periods.

Track Your Five-Year Waiting Periods

After transferring funds, it’s essential to track the five-year waiting period for each conversion. Each individual conversion starts its own five-year clock. To stay organized, create a spreadsheet to monitor your "ladder." Include details like the conversion amount, tax year, penalty-free date (January 1 of the fifth year after the conversion), and taxes paid. Setting calendar reminders for each maturity date can help you avoid costly errors.

"You don't want to implement the strategy and then get years mixed up and accidentally incur a 10% early withdrawal because you somehow voided that five years." - Ali Swart, CFP, Waldron Private Wealth

Keep copies of Form 1099-R and Form 8606 for your records and IRS compliance. Before making any withdrawals, double-check your documentation to ensure you don’t accidentally trigger penalties. This meticulous tracking is the backbone of your Roth conversion ladder, ensuring you can access funds penalty-free when you need them in early retirement.

Roth Conversion Ladder: Retire Early Tax & Penalty Free

Step 5: Avoid Common Mistakes and Stay Compliant

As you refine your conversion strategy, it's essential to steer clear of common errors and stay aligned with IRS regulations. Here's what you need to know.

How to Avoid Early Withdrawal Penalties

Withdrawing funds too soon can lead to costly penalties. The IRS imposes a 10% penalty on withdrawals made before the five-year holding period is up. Here's how the IRS prioritizes withdrawals from your Roth IRA: contributions come out first (and are always penalty-free), followed by converted amounts (on a first-in, first-out basis), and finally, earnings.

One key tip: always pay conversion taxes with funds outside of your IRA. If you're under 59½ and your brokerage withholds 20% for taxes from the conversion itself, that withheld amount is considered a taxable distribution - and it could trigger an additional 10% penalty. For example, if you convert $50,000 and $10,000 is withheld for taxes, you may face a penalty on that $10,000. To avoid this, use cash savings or a taxable brokerage account to cover the taxes.

IRS Reporting and Documentation Requirements

When you execute a Roth conversion, proper documentation is critical. File Form 8606 with your tax return to track your IRA basis and avoid being taxed twice. Your brokerage will also provide two important forms:

- Form 1099-R: Details the distribution from your Traditional IRA.

- Form 5498: Confirms the contribution to your Roth IRA.

Keep these forms organized for future reference.

Be mindful of the pro-rata rule, which applies if your Traditional IRA includes both pre-tax and after-tax funds. The IRS treats all your IRAs as a single account for tax purposes. For example, if you have $90,000 in pre-tax funds and $10,000 in after-tax contributions, converting $10,000 would result in 90% of that amount being taxable. To reduce the taxable portion, you could roll pre-tax funds into a 401(k) before converting.

If you're 73 or older, remember to take your full Required Minimum Distribution (RMD) before converting any additional funds. Skipping this step could result in penalties. As Ben Bowers, Managing Director at Bennett Thrasher, explains:

"The IRS states that an RMD cannot be converted into a Roth account. If someone tries to convert before withdrawing the RMD, the IRS will treat the conversion as an excess Roth contribution, which may result in penalty charges."

Maintaining accurate records ensures your conversion strategy stays compliant and effective. This is a key component of how to cut retirement taxes with Roth conversions over the long term.

Reduce Tax Costs and Unexpected Expenses

Large Roth conversions can significantly increase your Modified Adjusted Gross Income (MAGI), leading to unexpected tax consequences. For instance, if you're 63 or older, a higher MAGI could push you into higher Medicare IRMAA brackets. Starting in 2026, these surcharges kick in if your MAGI exceeds $103,000 for single filers or $206,000 for married couples filing jointly.

Similarly, if you receive Affordable Care Act premium tax credits, be aware that these subsidies drop off sharply when your household MAGI exceeds 400% of the Federal Poverty Level (around $58,320 for a single filer in 2025). A large conversion could push your income past this threshold, costing you thousands in lost credits.

To manage your tax liability, consider a bracket-filling strategy. Estimate the "air space" left in your current tax bracket by subtracting your projected taxable income from the bracket's upper limit. For example, in 2025, the 22% tax bracket tops out at $95,375 for single filers and $190,750 for married couples filing jointly. Converting just enough to stay within that limit can help you avoid moving into a higher tax bracket. If your conversion increases your tax bill by more than $1,000, use IRS Form 1040-ES to make quarterly estimated payments and avoid underpayment penalties.

Finally, complete all conversions by December 31 to ensure they count for that tax year. Since the 2018 tax law changes, Roth conversions can no longer be undone, so precise year-end planning is crucial. Many people wait until late in the year, when their annual income is clearer, to avoid converting too much. Additionally, converting during market downturns allows you to move the same number of shares at a lower tax cost, letting future growth compound tax-free.

Wrapping It Up

This guide walks you through the steps for building a Roth conversion ladder - a strategy that helps early retirees tap into retirement savings before age 59½ without penalty. While it demands strict adherence to IRS rules, it offers the dual benefits of tax-free growth and accessible funds.

The key is to start at least five years before you need the money. Convert smaller amounts annually to stay within lower tax brackets, and remember that the five-year clock for each conversion begins on January 1 of the conversion year. To maximize your Roth’s growth potential, pay taxes on conversions using external funds. Use trustee-to-trustee transfers to avoid mandatory withholding, and ensure all conversions are completed by year-end. Don’t forget to file Form 8606 with your tax return to properly document conversions and avoid double taxation.

Keep an eye on income thresholds to steer clear of surcharges or lost credits. Market downturns can be an ideal time to convert, as you can transfer more shares at a lower tax cost, setting the stage for tax-free growth in the future. If you’re 73 or older, make sure to satisfy your Required Minimum Distribution before converting additional funds. By following these steps, early retirees can create a penalty-free income plan that supports their long-term financial goals.

FAQs

How do I pick a safe annual conversion amount?

To determine a safe annual conversion amount for your Roth conversion ladder, aim to convert just enough to stay within your current tax bracket without pushing into a higher one. Many people focus on maximizing lower brackets, such as the 12% bracket, without exceeding its threshold. To do this effectively, evaluate each year's conversion based on your total income, deductions, and overall tax situation. This approach helps minimize your tax burden and keeps you from triggering higher tax rates.

What counts as the 5-year clock for each conversion?

When you convert funds from a traditional IRA or 401(k) to a Roth IRA, the 5-year clock begins on the date of that specific conversion. Here's an important detail: each conversion has its own separate 5-year period. This means that if you make multiple conversions, you'll need to track the timeline for each one individually.

To withdraw the converted principal without penalties - especially if you're under 59½ - you must wait five tax years from the date of that particular conversion.

How can conversions affect ACA subsidies and Medicare IRMAA?

Roth conversions can bump up your taxable income, potentially leading to higher Medicare IRMAA premiums for the following two years. On top of that, an increase in income might push you past the thresholds for ACA subsidies, affecting your eligibility. It's important to consider these potential ripple effects when planning a conversion to avoid any surprise expenses.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.