An IDGT may move future asset growth out of a taxable estate while leaving the income tax bill with the grantor. That is the basic tradeoff.

If I were boiling this down fast, I’d say this article covers five things:

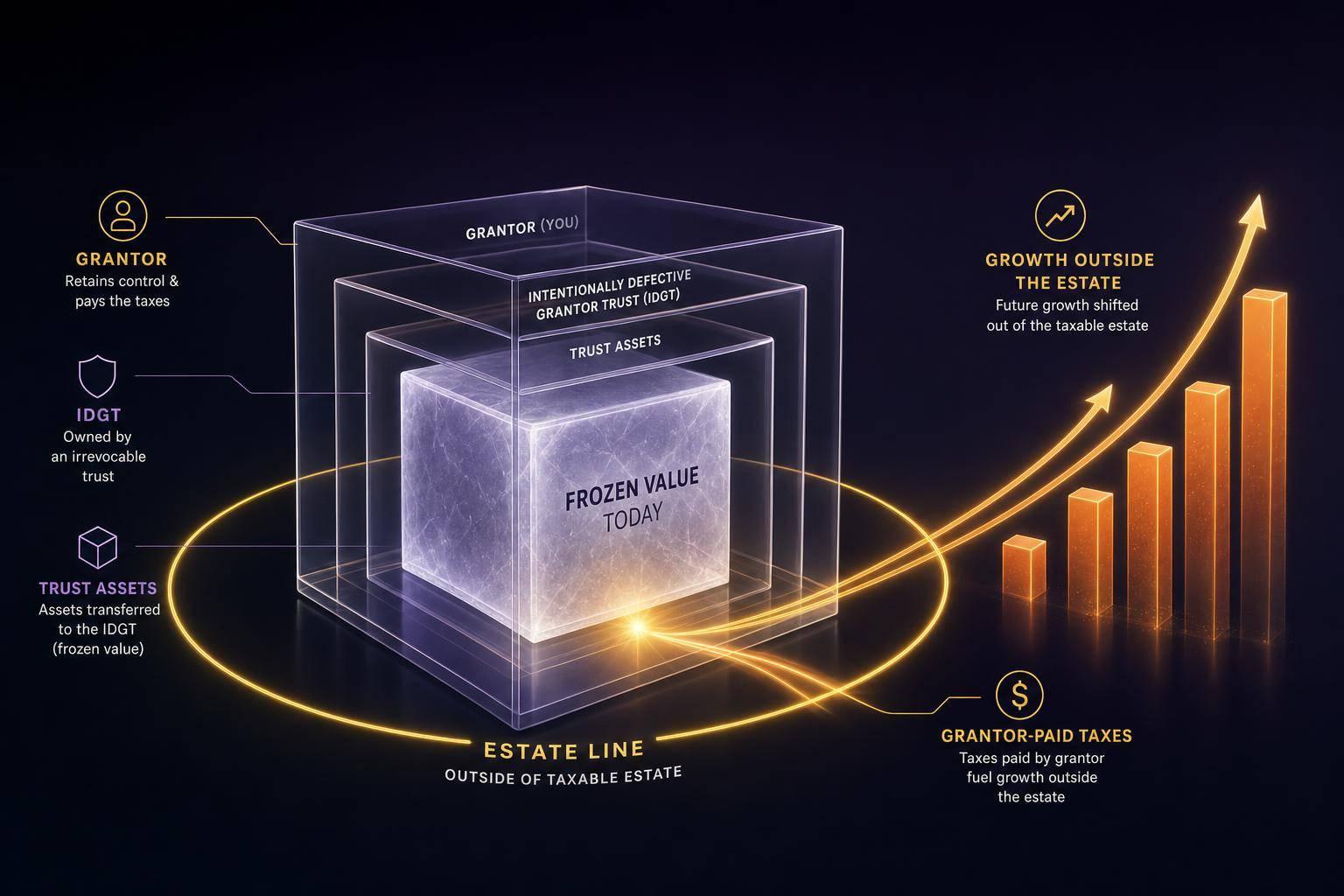

- What an IDGT is: an irrevocable trust with one tax treatment for estate and gift tax and another for income tax

- Why people use it: to freeze today’s value and shift later growth on assets like a business interest, real estate, or stock

- How it often works: a seed gift, a sale to the trust, a promissory note tied to the AFR, and grantor-paid income taxes

- Who may look at it: families with estates near or above the $15 million federal exemption in 2026, especially when assets may grow fast

- What the tradeoffs may be: loss of control, tax bills paid from outside the trust, valuation work, IRS review, and no automatic step-up in basis

Here’s the plain-English version:

An IDGT is built to create a tax mismatch on purpose. For transfer-tax purposes, the trust may stand on its own. For income-tax purposes, the grantor may still be treated as the owner. That setup may let post-transfer growth sit outside the estate, while the grantor’s tax payments may reduce the estate over time without counting as extra gifts under Rev. Rul. 2004-64.

But the setup may not work well for everyone.

If asset growth does not beat the note rate, if outside cash flow is tight, or if irrevocability is hard to accept, the math may be less attractive. And with non-public assets, appraisals, discounts, and note terms may need close attention.

Bottom line: an IDGT may appeal to people with high-growth assets, outside liquidity, and a clear estate tax issue. The article then walks through the setup, the fit, and the main risks in simple terms.

Estate Tax Exemption Sunset 2026: Portability and IDGT Explained

How an IDGT works

How an IDGT Works: 3-Step Estate Planning Process

The mechanics usually come down to three moves: seed the trust, sell the assets, and pay the tax.

Step 1: Create and fund the irrevocable trust

The trust is drafted as an irrevocable trust with grantor-trust powers, such as a substitution power. That setup may make the trust separate for transfer-tax purposes while still being ignored for income-tax purposes.

To start, the trust is often seeded with cash or other liquid assets equal to about 10% to 20% of the planned sale value. That funding may give the sale economic substance and may support the view that it was a real sale.

Step 2: Transfer assets through a gift or installment sale

After the trust is funded, assets such as closely held business interests, real estate, or securities may be transferred to it by gift or installment sale. If the note pays less than the IRS Applicable Federal Rate (AFR), part of the transaction may be treated as a taxable gift.

The sale usually may not trigger current capital gains tax, and future appreciation above the note principal may stay outside the grantor's estate. With closely held businesses, lack-of-control and lack-of-marketability discounts may reduce the appraised value by 20% to 40%. That may lower the note principal and may preserve more of the grantor's lifetime exemption.

Step 3: Why the grantor's tax payments matter

The grantor reports the trust's income on a personal return and pays the tax personally. Under Revenue Ruling 2004-64, those tax payments are not additional gifts, so they may reduce the grantor's estate without reducing the trust itself.

That may let the trust grow without the same tax drag it might otherwise face, which may speed up the transfer of wealth to beneficiaries.

In practice, the structure may work by freezing value, shifting future growth, and reducing the grantor's estate through those tax payments.

Still, those mechanics may work only when the trust matches the grantor's liquidity, asset mix, and comfort with irrevocability.

When an IDGT makes sense

Once the trust structure is clear, the next step may be figuring out whether the assets, cash flow, and tax exposure make an IDGT worth considering.

Who typically considers an IDGT

IDGTs may fit estates that are likely to face transfer tax and hold assets with high expected appreciation. In plain English: this structure may make more sense when a family owns assets that may grow faster than the estate may be reduced by transfer taxes.

In 2026, the federal unified gift and estate tax exemption is $15 million per person. Families whose estates may exceed that threshold - or may cross it later as assets appreciate - are often the strongest candidates. That may include high-net-worth individuals, families focused on multi-generational wealth transfer, and owners of closely held businesses or professional practices.

Generation-skipping transfers may add another layer to the decision. If those transfers are part of the plan, added transfer taxes may further reduce what passes to heirs.

There’s also a simple math test in the background. If projected growth may not exceed the note rate and tax drag, the strategy may lose much of its appeal.

Financial and operational requirements

Estate size is only part of the picture. A few practical pieces may need to line up too.

The biggest one is outside liquidity. The grantor may need enough cash flow outside the trust to cover income tax, capital gains tax, and similar tax liabilities over the long term without turning to trust assets for those payments. The other major constraint is irrevocability. After the transfer, the grantor may not reclaim the assets.

That’s why families may need to be comfortable with two things at once:

- Paying tax bills from outside the trust for years

- Giving up access to the transferred assets

Cost may matter too. Setting up the plan often brings legal, valuation, and trustee expenses. A formal business interest valuation typically runs $7,500 to $25,000, depending on complexity, and rush engagements may add a 25% to 50% premium. The process also often involves coordinating an estate attorney, a CPA, and in many cases a corporate trustee.

How Mezzi helps assess fit before implementation

Before legal drafting starts, the main question may be whether the full balance sheet can support the structure.

Mezzi connects brokerage, retirement, and taxable accounts through read-only access, giving you a full view of holdings in one place. From there, it may help spot concentrated positions, show tax drag across accounts, and model how a possible IDGT may interact with taxable assets and retirement accounts.

If you hold concentrated stock or a minority business interest, Mezzi may surface the context you need before that first estate planning meeting. That way, you may walk in with a clearer sense of where concentration risk sits and how the strategy may affect the rest of your long-term plan.

Benefits, risks, and tradeoffs

Once the structure is in place, the next question may be simple: do the tax savings outweigh the loss of control?

Key benefits: estate tax reduction and wealth transfer efficiency

An IDGT’s main appeal may be estate tax reduction paired with grantor-paid income taxes. Future growth on transferred assets stays outside the taxable estate. Over time, that tax-free compounding may widen the gap between the trust’s value and the value still counted in the estate. For closely held businesses, valuation discounts may also reduce the taxable value of the transfer.

| Strategy | Estate Tax Impact | Income Tax Responsibility | Best-Fit Situation |

|---|---|---|---|

| Non-Grantor Irrevocable Trust | Removes asset and future growth | The trust (at compressed rates) | Grantors who may not be able to sustain the income tax obligation |

| IDGT | Removes future growth; freezes value | Grantor (may reduce estate further) | High-growth assets; high-net-worth estates |

Key risks: irrevocability, tax burden, and IRS scrutiny

The same features that make an IDGT appealing may also create hard limits. Irrevocability may be the biggest one. Once assets are transferred, you may not simply pull them back. That loss of control may be permanent.

The ongoing income tax obligation may be the other main pressure point. You may owe taxes on trust earnings - ordinary income, dividends, and capital gains - on assets you no longer legally own. If personal liquidity gets tighter, that tax burden may still remain.

For installment sales, IRS scrutiny may also matter. Without proper seeding and a qualifying note rate, the IRS may recast the transaction as a taxable gift. If the asset being transferred is not publicly traded, a qualified appraisal may be needed. Penalties for valuation misstatements under IRC Section 6662 may reach 20% to 40% of the understated tax amount.

Pros and cons for the grantor and beneficiaries

The same features that may help beneficiaries may create tradeoffs for the grantor. The table below lays out the main factors on both sides.

| Factor | Description | Impact on Grantor | Impact on Beneficiaries |

|---|---|---|---|

| Income Tax Burn | Grantor pays taxes on trust income | Con: Ongoing liquidity drain | Pro: Assets may grow without tax drag; inheritance may be larger |

| Estate Freeze | Locks in asset value at time of transfer | Pro: May reduce future estate tax liability | Pro: Receives all post-transfer appreciation |

| Irrevocability | Trust cannot be easily changed | Con: Loss of direct ownership and control | Pro: Asset protection |

| Installment Note | Trust pays grantor interest on the promissory note | Pro: Retained income stream | Con: Trust may need to use cash flow to service the debt |

| Basis Treatment | No step-up in cost basis at grantor's death | Neutral: No direct tax impact | Con: Potential capital gains tax liability if assets are sold |

Substitution powers may help manage basis before death, but they may not remove basis risk. Those tradeoffs may come into sharper focus in the examples that follow.

Examples and conclusion

Example 1: Selling closely held business interests to an IDGT

Two common IDGT uses involve closely held businesses and marketable securities.

Take a founder with a business valued at $5,000,000. Instead of moving the whole company, the founder sells a 30% minority interest to an IDGT. A qualified appraiser applies a discount and values that 30% stake at $900,000 rather than $1,500,000. That discounted amount becomes the actual sale price to the trust.

To support the sale, the trust receives a $90,000 seed gift and signs a $900,000 promissory note at or above the AFR. If the asset grows after the sale, that future growth may sit outside the taxable estate. The founder also continues paying income taxes tied to the trust's earnings, which may further reduce the estate without using more gift tax exemption.

There’s a practical catch: the business may need enough cash flow to cover the note interest. If it doesn’t, the seed gift may get used up, and the plan may lose some of its appeal.

Example 2: Transferring marketable securities with high appreciation potential

The same basic setup may also work for liquid portfolios when expected returns may exceed the AFR. This version still depends on grantor-trust treatment and grantor-paid taxes. In one example, Julia funded an IDGT with cash and marketable securities and kept the initial gift below her unused federal exemption, with the goal of avoiding out-of-pocket gift tax.

She also kept a substitution power. That power may support grantor trust status and may let the grantor exchange personal assets for trust assets of equal value.

Julia pays the trust’s taxes herself. That may allow assets to keep growing inside the trust while also reducing her taxable estate. If the securities grow faster than the note’s interest rate, the extra appreciation may pass to beneficiaries without estate or gift tax.

The main test is simple: returns may need to beat the AFR. If the securities underperform, the setup may produce limited estate tax savings. That’s why asset choice and follow-up review may play a big part here.

Conclusion: Key decision points before using an IDGT

IDGTs may fit larger estates, especially when the assets may grow fast, the grantor has outside liquidity, and giving up control may be acceptable. The assets transferred may need strong appreciation potential, and the grantor may need enough cash outside the trust to cover the trust’s income tax bill each year.

Before moving ahead, people often look at a few core issues.

| Decision Point | What to Evaluate |

|---|---|

| Estate size | Whether the estate may sit meaningfully above the $15 million exemption |

| Asset growth | Whether transferred assets may outpace the current AFR |

| Liquidity | Whether the grantor may pay the trust’s income taxes without financial strain |

| Control | Whether an irrevocable structure may be acceptable |

| No step-up in basis | Whether beneficiaries may be able to absorb potential capital gains at sale |

Implementation usually involves a coordinated group: an estate attorney to draft the trust, a tax advisor to model the income tax obligations, and a qualified appraiser for any non-publicly traded assets.

FAQs

How is an IDGT taxed?

An IDGT has split tax treatment. For income tax purposes, it’s “defective,” which means the grantor is treated as the owner and pays the trust’s income taxes. As a result, the trust assets may keep growing without being reduced by those tax payments.

For estate tax purposes, the trust remains effective: the assets and any future appreciation are removed from the grantor’s estate. Transactions between the grantor and the IDGT are also generally disregarded for income tax purposes.

What assets work best in an IDGT?

Assets with strong long-term appreciation potential may fit well in an IDGT. Common examples include stock in a successful family business or other closely held entities, along with marketable securities and real estate.

The idea is to move future growth outside your taxable estate by locking in the asset’s current value for tax purposes. If that growth happens later, it may pass to beneficiaries without added estate taxes.

What can cause an IDGT to fail?

An IDGT may fail if it isn’t set up and run under strict legal and tax rules.

Common problems include:

- inadequate trust funding

- unsupported asset valuations

- too much grantor control

- note interest below the AFR

- interest payments tied to asset income

Poor planning may also create liquidity problems if the grantor may not have enough cash to cover the trust’s income taxes.

Disclosures:

• This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

• Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.