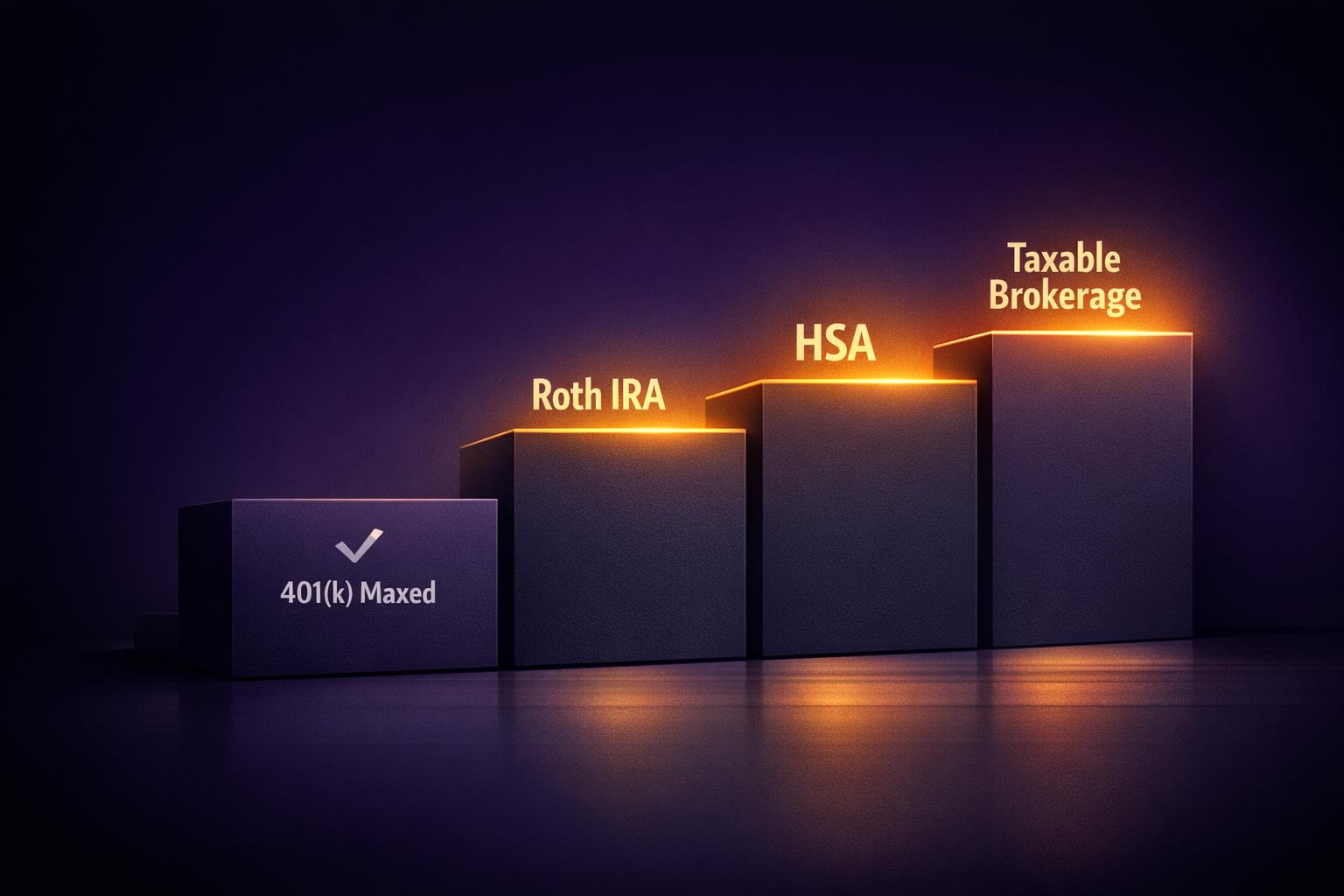

If you've already maxed out your 401(k) contributions for 2026 ($24,500 or $32,500 if you're 50+), here’s what to do next:

- Roth IRA: Contribute up to $7,500 ($8,600 if 50+). Offers tax-free growth and withdrawals in retirement. If your income exceeds the limit, consider a backdoor Roth conversion.

- Health Savings Account (HSA): If you have a high-deductible health plan, contribute $4,400 (individual) or $8,750 (family) for triple tax benefits (tax-deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses).

- Taxable Brokerage Account: No contribution limits, high liquidity, and ideal for early retirement or non-retirement goals.

For specialized goals, consider 529 Plans for education savings or municipal bonds for tax-free income.

Key Tip: Use tools like Mezzi to optimize contributions, manage taxes, and rebalance your portfolio efficiently.

Tax-Advantaged Account Comparison: 401(k), Roth IRA, HSA, and Taxable Brokerage

You Maxed Your 401(k)… Now What? Smart Next Steps!

Roth IRA: Your Next Tax-Advantaged Account

Once you've maxed out your 401(k), a Roth IRA is often the next smart move for your retirement savings. Unlike a 401(k), which taxes withdrawals during retirement, a Roth IRA offers tax-free growth and allows you to withdraw funds tax-free after age 59½, provided you've met the five-year holding rule. This means every dollar of growth in your account stays with you, untouched by taxes. It's a powerful way to boost the tax efficiency of your portfolio.

For 2026, the contribution limit for a Roth IRA is $7,500, or $8,600 if you're 50 or older. However, your ability to contribute depends on your Modified Adjusted Gross Income (MAGI). For single filers, contribution eligibility begins to phase out at $153,000 and disappears entirely at $168,000. For married couples filing jointly, the phase-out range is $242,000 to $252,000. If your income exceeds these limits, you can still use a backdoor Roth conversion by contributing to a Traditional IRA and then converting it to a Roth IRA.

One standout feature of the Roth IRA is the absence of required minimum distributions (RMDs). Unlike other retirement accounts that require you to start taking withdrawals at a certain age, a Roth IRA allows your money to grow tax-free indefinitely. This flexibility makes it a great option for preserving wealth for your heirs or maintaining control over your retirement funds.

Roth IRA vs. Traditional IRA: How They Compare

Deciding between a Roth IRA and a Traditional IRA often comes down to when you'd prefer to handle taxes - now or later. Here's a side-by-side comparison:

| Feature | Roth IRA | Traditional IRA |

|---|---|---|

| Tax Treatment | Contributions are made with after-tax dollars; withdrawals are tax-free in retirement | Contributions may be tax-deductible; withdrawals are taxed as ordinary income |

| 2026 Contribution Limit | $7,500 ($8,600 if 50+) | Same as Roth IRA |

| Income Restrictions | Phase-out starts at $153,000 (single) / $242,000 (married filing jointly) | No income limit to contribute, though deductibility may depend on workplace plan coverage |

| Required Minimum Distributions (RMDs) | None during the owner's lifetime | RMDs are required in retirement |

| Withdrawal Flexibility | Contributions can be withdrawn tax-free anytime; earnings are tax-free after age 59½ with the five-year rule | Early withdrawals before 59½ are usually subject to taxes and a 10% penalty |

If you think you'll be in a higher tax bracket during retirement or want more control over your taxes, a Roth IRA might be the better choice. Plus, because withdrawals from a Roth IRA don’t count as taxable income, they can help you manage your overall tax liability in retirement.

Now, let’s explore how Mezzi can help you make the most of your Roth IRA contributions.

How Mezzi Helps You Time Roth Contributions

Timing your Roth IRA contributions or conversions can get tricky, especially if your income varies year to year. Contributing when you're near the MAGI limit could lead to penalties or missed opportunities.

Mezzi simplifies this process by analyzing your income patterns and account activity to recommend the best timing for Roth contributions. If your income is close to the phase-out range, Mezzi might suggest waiting until later in the year, when you have a clearer view of your final MAGI. It also identifies opportunities for Roth conversions during lower-income years, helping you convert Traditional IRA funds to a Roth with minimal tax impact.

With read-only access to your financial accounts, Mezzi provides insights that traditionally would cost thousands in advisory fees. It’s a practical tool for optimizing your Roth IRA strategy whenever you need it.

Health Savings Account (HSA): Triple Tax Benefits

Once you've maxed out your 401(k) and Roth IRA, a Health Savings Account (HSA) becomes a smart next step - especially if you're covered by a High-Deductible Health Plan (HDHP). HSAs offer a standout feature: triple tax benefits. Contributions are tax-deductible, investments grow tax-free, and withdrawals for qualified medical expenses are also tax-free. If you use payroll deductions, you can save even more by avoiding the 7.65% FICA tax. Like a Roth IRA, a well-managed HSA can be a key part of a diversified, tax-efficient portfolio - an area where Mezzi’s AI tools shine.

For 2026, the contribution limits are $4,400 for individuals and $8,750 for families. If you're 55 or older, you can add a $1,000 catch-up contribution. To qualify for an HSA, your HDHP must have at least a $1,700 deductible for individuals or $3,400 for families, with out-of-pocket maximums capped at $8,500 and $17,000, respectively. You also can’t be enrolled in Medicare or listed as a dependent on someone else’s tax return.

Unlike Flexible Spending Accounts (FSAs), HSA balances roll over year after year - there’s no "use it or lose it" rule. Plus, your account remains yours even if you switch jobs or health plans. After age 65, the 20% penalty for non-medical withdrawals disappears. Non-medical withdrawals are taxed as ordinary income, but withdrawals for qualified medical expenses remain tax-free.

"These accounts are best used as retirement savings and investing vehicles rather than as 'checking accounts.'"

- Kim Curtis, CFP

A 65-year-old retiring in 2024 is estimated to need about $165,000 for healthcare expenses during retirement. Yet, only 13% of HSA holders invest their funds, with most treating their accounts like simple checking accounts. For example, if a couple maxes out family HSA contributions every year from age 30 to 65 and achieves a 7% annual return, they could accumulate around $1.1 million tax-free for medical expenses.

How HSAs Compare to Other Tax-Advantaged Accounts

HSAs have a tax profile that’s hard to beat. Here’s how they stack up against other accounts:

| Feature | HSA | Roth IRA (Note: Earnings taxed if withdrawn before age 59½) | Traditional IRA | Taxable Account |

|---|---|---|---|---|

| Contributions | Tax-Deductible | Post-Tax | Tax-Deductible | Post-Tax |

| Growth | Tax-Free | Tax-Free | Tax-Free | Taxed Annually |

| Medical Withdrawals | Tax-Free | Tax-Free | Taxed | Taxed (Capital Gains) |

| Non-Medical Withdrawals | Taxed (Penalty if under 65) | Tax-Free (earnings taxed if under 59½) | Taxed | Taxed (Capital Gains) |

| Required Distributions | None | None | Yes (at age 73+) | None |

Financial experts often recommend this contribution strategy:

- Contribute to your 401(k) up to the employer match.

- Max out your HSA.

- Max out your Roth IRA.

- Contribute any remaining funds to your 401(k).

Investing Your HSA for Long-Term Growth

With its tax perks in place, your HSA can work just as hard as your other retirement accounts. Instead of using it like a checking account, invest the funds for long-term growth. Pay current medical bills out-of-pocket and save receipts digitally - there’s no IRS deadline for reimbursing yourself. This "pay now, reimburse later" approach allows your HSA balance to grow tax-free for decades.

"Your HSA is not a medical spending account - it is a tax optimization engine. Treat it accordingly."

- Michael Torres, CPA, HSA Orbit

A practical rule of thumb is to keep one to two times your annual deductible in cash in your HSA for emergencies, then invest the rest. For a long-term horizon, consider aggressive investment options like 100% U.S. Total Stock Market index funds or a three-fund portfolio (60% U.S. stocks, 30% international stocks, 10% bonds). Choose providers offering low-cost index funds, no maintenance fees, and no minimum balance requirements for investing.

Mezzi can help you fine-tune your HSA investment strategy by analyzing your portfolio and suggesting the best asset allocation based on your goals and risk tolerance. It also flags uninvested cash in your account and recommends reallocating it into growth-focused investments - ensuring your HSA contributes meaningfully to your financial future.

Taxable Brokerage Account: Flexibility Without Limits

Once you've maxed out your 401(k), Roth IRA, and HSA, a taxable brokerage account is a great place for extra savings. Unlike retirement accounts, there are no contribution limits here (for reference, 401(k) contributions will cap at $24,500 in 2026). This means you can invest as much as you want, giving you unmatched freedom with your money.

These accounts are also incredibly liquid, making them perfect for short-term financial goals or early retirement. You can withdraw your funds anytime, for any reason, without penalties. For those retiring early, this flexibility can bridge the gap between leaving the workforce and accessing retirement funds penalty-free.

"Because you can take money out anytime, money saved in brokerage accounts can help early retirees bridge the gap to age 59½ when qualified distributions from retirement accounts typically begin."

- Fidelity Viewpoints

Taxable brokerage accounts also come with no required minimum distributions (RMDs), meaning you can keep your money invested indefinitely. This is a big advantage for estate planning, too. When you pass away, your heirs may benefit from a step-up in cost basis, which adjusts the value of inherited assets to their current market value. This can significantly reduce - or even eliminate - capital gains taxes on appreciated assets.

Taxable vs. Tax-Advantaged Accounts: Key Differences

Here’s a quick comparison between taxable brokerage accounts and retirement accounts:

| Feature | Taxable Brokerage Account | Retirement Accounts (401(k)/IRA) |

|---|---|---|

| Liquidity | High; withdraw anytime without penalty | Limited; early withdrawals often incur penalties |

| Contribution Limits | None; invest as much as you like | Capped annually (e.g., $24,500 for 401(k) in 2026) |

| Tax Treatment | Taxes on dividends, interest, and realized gains annually | Tax-deferred or tax-free growth |

| Investment Choice | Almost unlimited (stocks, bonds, ETFs, options, cryptocurrency, etc.) | Often limited to pre-selected funds |

| Mandatory Withdrawals | None; funds can remain invested indefinitely | RMDs usually start at age 73 |

The trade-off is simple: you give up the upfront tax benefits of retirement accounts in exchange for complete investment control and flexibility. This makes taxable accounts ideal for long-term goals and bridging early retirement gaps.

Managing Taxes in Your Brokerage Account

To make the most of a taxable brokerage account, smart tax management is essential. These accounts are subject to annual taxes on dividends, interest, and realized gains. Holding investments for over a year can help you benefit from long-term capital gains rates (0%, 15%, or 20%), which are lower than short-term rates taxed at your regular income level.

Another strategy to manage taxes effectively is tax-loss harvesting. By selling investments that have underperformed, you can offset gains from other assets, reducing your tax bill. Tools like Mezzi can help identify these opportunities while also flagging risks like wash sales, which occur if you repurchase the same or a similar security within 30 days.

Asset location is another key consideration. For instance, tax-efficient investments like index funds or municipal bonds are well-suited for taxable accounts. On the other hand, tax-inefficient assets, such as high-turnover active funds, are better held in tax-advantaged accounts. Mezzi’s X-Ray tool can analyze your portfolio for overlapping holdings and provide year-round tax optimization tips, ensuring you don’t pay unnecessary fees for duplicate exposures.

"Vanguard's index funds have managed to be particularly tax-efficient because the firm's ETFs are share classes of its funds."

- Christine Benz, Director of Personal Finance and Retirement Planning, Morningstar

For investors in higher tax brackets (24% or more), municipal bonds can be an excellent fixed-income choice. Their interest is often exempt from federal and state taxes. Meanwhile, equity ETFs and index funds are great for growth since their in-kind redemption process minimizes capital gains.

While Mezzi doesn’t execute trades or move money, it offers read-only insights to help you optimize your portfolio. Whether it’s spotting tax-loss harvesting opportunities, recommending rebalancing strategies, or advising on asset location, Mezzi provides the kind of guidance you'd expect from a high-cost advisor - without the hefty price tag.

Other Tax-Efficient Savings Options to Consider

Expanding beyond traditional retirement accounts and standard brokerage options, there are additional savings vehicles designed for specific financial goals. Two noteworthy options - 529 college savings plans and municipal bonds - offer tax advantages that can complement your overall portfolio strategy.

529 Plans for Education Expenses

If you're setting money aside for a child’s education, 529 plans provide significant tax benefits. Contributions grow tax-deferred, withdrawals for qualified education expenses are tax-free, and many states offer tax deductions or credits for contributions. These plans cover both college and K-12 expenses, allowing up to $10,000 annually for tuition and a $10,000 lifetime limit for student loan repayment.

One of the standout features of a 529 plan is its flexibility. You can change the plan's beneficiary to another family member - such as a sibling or cousin - without triggering tax penalties. Additionally, individuals can contribute up to $19,000 per beneficiary annually (as of 2025) without incurring gift taxes. For those with higher incomes, there’s even an option to "superfund" a 529 plan by front-loading five years' worth of contributions - up to $95,000 for individuals or $190,000 for married couples.

"529 plans stand out as one of the most effective tax-advantaged savings options. The key advantages of 529 plans are their triple tax benefits: contributions grow federally tax-free, withdrawals for qualified expenses are tax-free, and most U.S. states offer tax deductions or credits for contributions."

- Jeffrey Trull, Writer, Savingforcollege.com

It’s important to note that many states require you to use their in-state plan to qualify for state tax benefits. Tools like Mezzi can help you calculate how much to save based on your child’s age, target schools, and expected education costs, ensuring you stay on track without overfunding the account.

Municipal Bonds for Tax-Free Income

Once you’ve addressed education savings with a 529 plan, municipal bonds can be a good choice for generating stable, tax-free income. These bonds, issued by states, cities, and counties to fund infrastructure projects, are particularly appealing for high earners since the interest they pay is exempt from federal income tax. If you buy bonds issued by your home state, you may also avoid state and local taxes on the interest.

To evaluate their return, compare the bond’s tax-free yield to a taxable bond by dividing the yield by (1 minus your tax rate). For instance, a 4% municipal bond offers the same after-tax return as a 5.56% taxable bond for someone in the 28% tax bracket.

"While municipal bonds might seem intimidating to investors who have never invested in them before, their ability to provide a predictable stream of tax-exempt income offers a unique and potentially powerful capability, especially useful for high-income earners in high-tax states."

- Richard Carter, Vice President of Fixed Income Strategy, Fidelity

Keep in mind that municipal bonds often require a minimum investment of around $5,000 per bond. They are best held in taxable brokerage accounts to maintain their tax advantages. Tools like Mezzi can analyze whether municipal bonds align with your risk tolerance and portfolio goals, helping you decide if the potential tax savings make them a smart addition to your investment strategy.

Optimizing Your Full Portfolio with AI

Once you've taken advantage of the tax and growth benefits offered by individual accounts, the next step is to fine-tune your entire portfolio. By coordinating your 401(k), Roth IRA, HSA, taxable accounts, and other specialty accounts, you can ensure every dollar is working as effectively as possible. Managing these accounts in isolation often leads to missed opportunities to cut taxes, manage risk, and improve overall returns. Smart asset location - placing specific investments in the most tax-efficient accounts - paired with regular rebalancing can add an extra 0.25%–0.75% to your after-tax returns annually. Over time, this can result in significant growth. Mezzi uses AI to integrate your financial data and provide actionable insights on taxes and risk, offering a service similar to what traditional advisors charge thousands for - without the typical 1% AUM fee.

Asset Location: Placing Investments Where They Work Best

Not all accounts are taxed the same way, so where you place your investments matters just as much as what you invest in. For example, high-growth stocks are ideal for Roth IRAs or HSAs, where gains can grow tax-free. On the other hand, tax-inefficient assets, like certain bonds or REITs that generate ordinary income, are better suited for tax-deferred accounts. If structured correctly, they can also be held in taxable accounts. Mezzi's AI reviews your connected accounts to identify assets that might be better placed elsewhere. For instance, moving high-growth stocks into a Roth IRA can allow gains to grow tax-free, potentially saving you a significant amount in taxes over time. This strategic placement lays the groundwork for consistent and effective portfolio rebalancing.

Rebalancing and Risk Management with Mezzi

Market fluctuations can quickly throw off your portfolio's balance. For example, a 60/40 stock-bond allocation can shift to 70/30, exposing you to more risk than intended. Mezzi monitors your portfolio daily and notifies you when shifts exceed 5%, prompting action. These alerts recommend steps like selling overweight positions to take advantage of tax-loss harvesting and reallocating funds to underweighted areas for a smoother balance.

Mezzi also identifies concentrated positions, such as when a single holding makes up more than 10% of your portfolio, and offers strategies to diversify over time. For instance, if your 401(k) is heavily invested in your employer's stock, Mezzi can guide you through net unrealized appreciation (NUA) rules to reduce concentration risk while keeping taxes low. Research shows that investors who use automated rebalancing tools achieve annualized returns that are 1.82% higher over 10 years compared to those who rebalance manually. This data-driven, disciplined approach can make a noticeable difference in your portfolio's performance over the long haul.

Conclusion

Maxing out your 401(k) is a huge step toward securing your financial future, but it’s just the start of building long-term wealth. Once you’ve reached that milestone, it’s time to put your additional savings to work in other tax-efficient vehicles like Roth IRAs, Health Savings Accounts (HSAs), taxable brokerage accounts, 529 plans, or even municipal bonds. Each option has its strengths: Roth IRAs allow for tax-free growth, HSAs come with triple tax benefits, and taxable accounts provide unmatched flexibility with no contribution limits.

The real challenge? Deciding where your next dollar should go. The best choice depends on your income, tax situation, and long-term goals. Whether it’s using a backdoor Roth conversion, fully funding your HSA for future growth, or increasing contributions to a taxable account for added liquidity, these strategies can significantly enhance your portfolio’s performance over time.

That’s where Mezzi steps in. Mezzi brings all your accounts together and provides powerful tax-optimization insights that are typically reserved for high-cost financial advisors. Unlike traditional advisors who charge hefty fees - often 1% of your assets under management - Mezzi delivers this guidance without the extra cost.

With Mezzi, you get 24/7 access to actionable, real-time advice tailored to your financial situation. Whether you’re considering a mega backdoor Roth or fine-tuning your HSA contributions, Mezzi’s AI-driven tools make it easier to navigate these decisions. By combining these insights with the savings strategies outlined here, you’ll have the confidence to make informed choices and keep your financial goals on track.

FAQs

Should I max an HSA before a Roth IRA?

When deciding between an HSA and a Roth IRA, it’s all about your financial priorities. HSAs come with triple tax perks: contributions are tax-deductible, growth is tax-deferred, and withdrawals for medical expenses are tax-free. This combination makes HSAs a powerful option for covering healthcare costs while building savings.

On the other hand, if your main goal is growing retirement funds, a Roth IRA might be the better fit. It offers tax-free growth and withdrawals, helping you secure income for your later years.

Many financial advisors suggest focusing on maxing out your HSA first because of its unique tax advantages. Once that’s done, putting money into a Roth IRA can help you build a solid retirement nest egg.

How do I do a backdoor Roth without tax surprises?

To carry out a backdoor Roth IRA without triggering unexpected taxes, it’s important to follow the steps precisely. Start by contributing after-tax dollars to a traditional IRA. Then, convert those funds into a Roth IRA.

Pay close attention to the pro-rata rule, which determines how conversions are taxed based on the proportion of pre-tax and after-tax balances across all your traditional IRAs. To reduce potential tax liability, you might want to roll pre-tax IRA funds into a 401(k) plan. It’s always a smart move to consult a tax professional to make sure you're in line with IRS regulations.

What should I invest in within a taxable brokerage to minimize taxes?

To keep taxes low in a taxable brokerage account, consider investments that are more tax-efficient. Options like tax-managed funds, municipal bonds, and dividend stocks with favorable tax treatment can be smart choices. On the flip side, steer clear of investments that result in high taxable distributions, such as actively managed stock funds and stocks with large dividend payouts. By focusing on these strategies, you can ease your tax burden while still working toward solid investment returns.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

- Registration does not imply a certain level of skill or that the SEC has approved the company or its services.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.