A Qualified Opportunity Fund may delay tax on an eligible capital gain, but for new investors after December 31, 2026, the old basis step-up rules may mostly be off the table.

If I strip this down to the part that matters: this setup may let me reinvest an eligible gain within 180 days, defer federal tax for a set period, and possibly avoid federal tax on new fund growth after a 10-year hold. But it may also come with private-fund risk, limited liquidity, state tax issues, sponsor risk, and a tax bill that may still come due before cash comes back.

Here’s the short version:

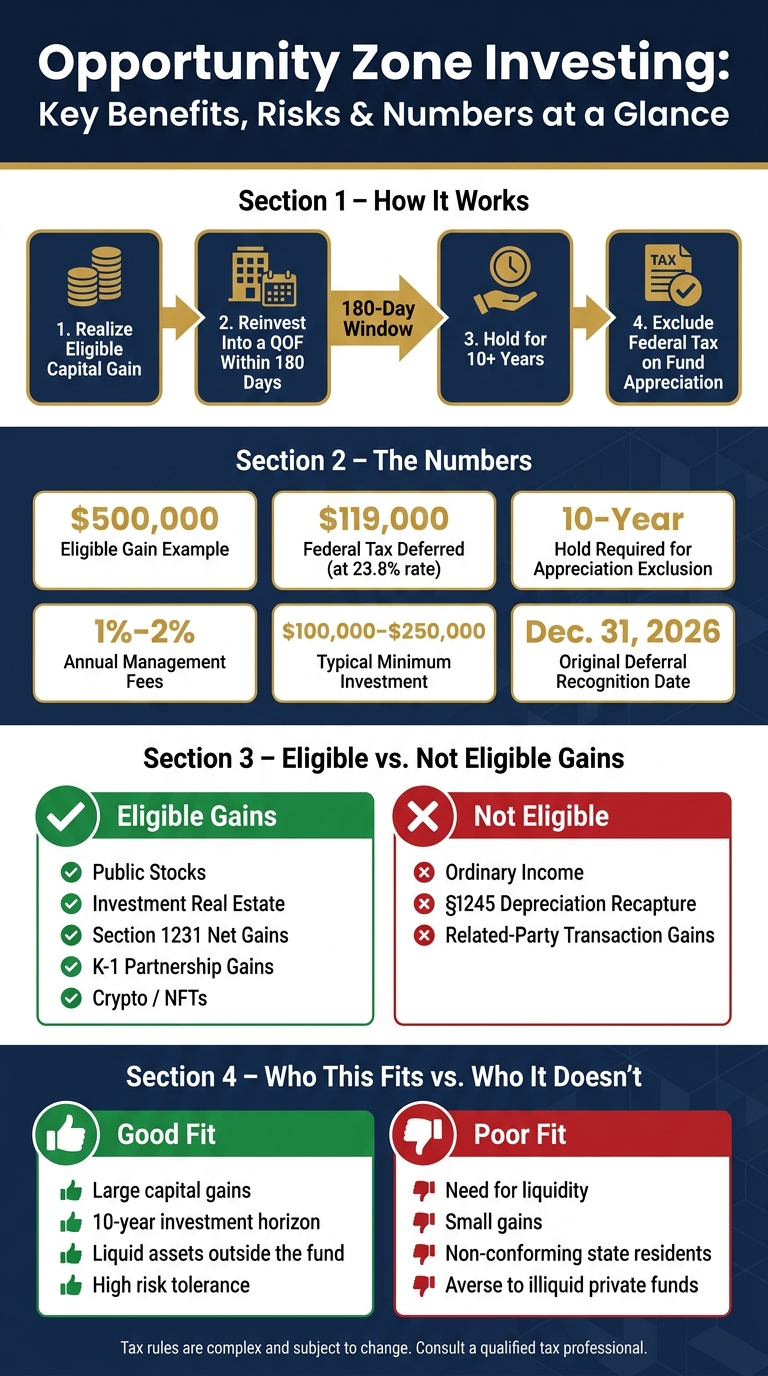

- Only capital gains may qualify - not ordinary income or most depreciation recapture.

- The 180-day deadline may control everything.

- The old 10% and 15% basis increases may no longer apply for most new deals.

- The main tax angle for many new investors may be the 10-year exclusion on fund appreciation.

- State tax treatment may differ, so federal deferral may not mean state deferral.

- QOFs may be illiquid and high risk, with fees often around 1% to 2% a year.

- Large minimums are common, often around $100,000 to $250,000.

A simple example: on a $500,000 eligible gain, federal tax at 23.8% may be about $119,000 if no QOF election is made. A QOF may delay that bill, but it may not erase tax on the original gain.

If I were summarizing the full article in one line, I’d put it this way: Opportunity Zone investing may be a tax-timing tool first and an investment second, so the deal may need to make sense even without the tax angle.

Opportunity Zone Investing: Key Benefits, Risks & Numbers at a Glance

How the New Opportunity Zone Rules Create Long Term Tax Savings

How Opportunity Zone investing works: eligible gains, Qualified Opportunity Funds, and deadlines

Benefits may apply only when the investment goes through a Qualified Opportunity Fund (QOF) - a partnership or corporation that self-certifies on Form 8996 and meets the 90% asset test. Once that part is clear, the next step may be figuring out which gains qualify and when the 180-day clock begins.

Who can invest and which gains qualify for deferral

Individuals and pass-through entities with realized capital gains may elect deferral through a QOF. Most capital gains may qualify, including gains from stocks, real estate, business interests, and digital assets.

Unlike a 1031 exchange, only the gain may need to be reinvested, not the full sale proceeds. If someone sells a rental property for $900,000 and has a $400,000 gain, only the $400,000 may need to go into the QOF for full deferral.

Some items do not qualify. Ordinary income, depreciation recapture taxed as ordinary income under §1245 or §1250, and gains from related-party transactions as defined under IRC §267(b) or §707(b) are excluded.

| Gain Type | Eligible for QOF? | 180-Day Clock Starts |

|---|---|---|

| Public stocks | Yes | Trade/closing date |

| Investment real estate | Yes | Closing/title transfer date |

| Section 1231 net gains | Yes | December 31 of the realization year |

| K-1 partnership gains | Yes | Choice of sale date, Dec 31, or return due date |

| Crypto / NFTs | Yes | Trade/closing date |

| Ordinary income | No | N/A |

| Depreciation recapture (§1245) | No | N/A |

The 180-day reinvestment window and key timing rules

After eligibility, timing may be the part that decides whether deferral remains available.

The 180-day clock starts when the gain is realized. For a stock sale or real estate closing, that may be the transaction date. For Section 1231 gains, the 180-day clock starts on December 31 of the realization year.

K-1 investors may start the clock on the gain date, the entity's year-end, or the return due date. Using the return due date may extend the window, and in some cases it may push the deadline into the following September for gains realized early in the prior year.

Meeting the deadline may only be the first part of the picture. The holding period may affect whether the tax treatment remains available.

Some events may end deferral before the 10-year hold is complete. Gifting a QOF interest or a fund liquidation may trigger immediate gain recognition. For gains deferred under the original program rules, that deferred gain is generally recognized on December 31, 2026, with tax due on the 2027 return.

How Mezzi can help before you commit capital

The 180-day window may move fast, and the first step may be knowing which gains are in play. Mezzi's read-only account aggregation connects taxable accounts so realized gains may be viewed in one place. Instead of sorting through trade confirmations and year-end statements, users may see what appears eligible and when each 180-day clock expires.

Mezzi may flag that a QOF strategy applies to a specific gain and may help with thinking through the timing before the window closes. It does not execute trades or move money; those steps are handled through a user's own custodian. Early tracking may help with meeting the 180-day deadline.

With eligible gains and deadlines identified, the next step is measuring the tax benefit.

Tax benefits explained: deferral, basis adjustments, and the 10-year appreciation exclusion

How tax deferral works and when the deferred gain is recognized

After you meet the deadline, the next issue may be timing: when does the tax come due? If you reinvest an eligible capital gain into a Qualified Opportunity Fund (QOF), your QOF interest starts with a zero basis.

For original-program investments, the deferred gain may be recognized on the earlier of:

- a sale of the QOF interest

- Dec. 31, 2026

For investments made after Dec. 31, 2026, the deferral period may run five years from the investment date.

How basis adjustments and long holding periods affect your tax outcome

Those basis step-ups applied only to investments made before the earlier deadlines, so they may no longer matter for most new investors.

The bigger long-term tax feature may be the 10-year appreciation exclusion. If you hold a QOF interest for at least 10 years, you may elect to increase the basis of the QOF investment to its fair market value at the time of sale. That election may exclude post-investment appreciation from federal capital gains tax, and for OZ 1.0 investments it remains available through Dec. 31, 2047.

For investments made after Dec. 31, 2026, the basis may increase to fair market value at sale or on the 30th anniversary of the investment, whichever comes first. For qualified rural opportunity funds, the five-year basis increase may be 30%.

That’s why the long-term value of a QOF may depend more on the 10-year exclusion than on the original deferral.

Hypothetical example: investing a $500,000 gain into a QOF vs. paying tax now

Here’s what that may look like in dollar terms. Suppose you have a $500,000 eligible gain. If you do not use a QOF, federal tax may be about $119,000 at a 23.8% rate. If you do invest the gain into a QOF, the tax on the original gain may be deferred until the applicable recognition date: Dec. 31, 2026, for original-program investments, or after five years for investments made after Dec. 31, 2026.

A QOF may defer tax on the original gain and may eliminate federal tax on future appreciation after 10 years. The deferred tax on the original gain still may have to be paid when it comes due.

Tradeoffs, limitations, and who this strategy fits

Key risks: illiquidity, concentration, execution, and law changes

Once the tax math looks appealing, the next step may be simpler: does the deal still make sense if your money may stay tied up for 10 years?

The tax upside may be meaningful. But the lockup, project risk, and compliance work may outweigh it.

Illiquidity may be the biggest issue. Secondary liquidity in QOF interests may be limited, so early exits may be hard. If an investor exits early, they may lose the most valuable tax break and may owe tax on the deferred gain sooner than expected.

Concentration and project risk may matter just as much. These markets may be distressed, so lease-up may lag and recoveries may fall short. Many QOFs may be tied to one project or one geography, which may leave investors with investment losses that outweigh any tax upside.

Fees and compliance add friction. Management fees typically run 1–2% annually, and QOFs must meet the 90% asset test or face penalties; repeated failures can jeopardize the tax benefit.

State treatment may reduce or erase part of the federal tax break. And rules may change over time, so any current tax edge may make sense to view as conditional.

That tends to narrow the field. In practice, this setup may fit a small group of patient investors.

Who Opportunity Zone investing fits - and who it does not

This strategy may fit investors with large gains, a 10-year horizon, and enough money outside the fund to cover deferred tax when it comes due. Most institutional-grade QOFs require minimum investments between $100,000 and $250,000.

For original-program investments, deferred tax may still come due before the fund distributes cash. If an investor does not have liquid assets outside the fund to cover that bill, the strategy may create a cash-flow problem.

It may be a poor fit for investors who need liquidity, have a small gain, live in a nonconforming state, or do not want high-risk, illiquid private-fund exposure.

Pros and cons at a glance

At a glance, the tradeoff may look pretty simple:

| Potential Benefit | What It Can Improve | Main Cost or Risk | Investor Implications |

|---|---|---|---|

| Tax Deferral | Near-term liquidity and compounding | Deferral may help liquidity now, but tax may still come due later | An investor may need cash ready for the tax payment when the gain is recognized |

| 10-Year Exclusion | Total after-tax return on new growth | 10-year lockup and little to no secondary market | May fit patient capital with a long horizon |

| Compliance Risk | N/A | 90% asset test failures can trigger penalties and jeopardize tax benefits | Due diligence on the sponsor may matter a lot |

| Hands-Off Access | Easier entry than a 1031 exchange | Fees of 1–2% annually plus manager reliance | Sponsor quality and track record may be critical |

Conclusion: How to evaluate an Opportunity Zone investment within a broader tax plan

The decision may come down to three checks: eligibility, timing, and deal quality.

Before investing, confirm the gain may actually be eligible. Confirm the 180-day window may still be open, since special start dates may apply to K-1 and Section 1231 gains. Then ask a simple question: does the deal work on its own, before taxes? Those two headline benefits - deferral and the 10-year basis step-up - may matter less if the underlying investment does not hold up without them.

If those checks pass, the next step may be to test the investment against your full tax picture. That may mean modeling the after-tax result across your portfolio, accounting for the deferred tax due on the applicable recognition date, making sure you may have enough liquidity outside the fund to cover that bill, and checking state conformity.

That’s where a clear, account-level view may help. Mezzi connects taxable accounts so you may compare the after-tax result, track deadlines, and review eligible gains before you invest.

Mezzi does not provide individualized tax or legal advice. Opportunity Zone rules are complex and subject to legislative change, including post-2026 rolling five-year deferral rules. Review current IRS guidance and consult a qualified tax professional before acting.

FAQs

How do I know if my gain qualifies?

Your gain may qualify if it’s a capital gain that would otherwise be reported on Schedule D or Form 4797.

That may include gains from:

- Stocks and bonds

- Investment or business real estate

- Business assets

- Partnership or S corporation interests

- Collectibles, cryptocurrency, or NFTs treated as capital assets

There’s one key limit here: only the capital gain portion may be invested.

So if part of the amount is ordinary income, that part does not qualify. The same generally applies to ordinary-income depreciation recapture under §1245 or §1250, and to gains from related-party sales.

What happens if I miss the 180-day deadline?

If you miss the 180-day deadline, you may lose the chance to defer that capital gain for Opportunity Zone tax treatment. There may be no extensions, relief provisions, or exceptions for good-faith errors.

To qualify, the funds must be wired into a Qualified Opportunity Fund by day 180. Signing subscription documents alone may not be enough.

How do state taxes affect QOF benefits?

State taxes may materially affect the after-tax result of Opportunity Zone investments because not all states follow federal QOF rules. Federal tax benefits may not apply the same way at the state level.

For example, California and New York do not conform to federal deferral rules, so deferred gains may still be taxable by the state in the year the gain was originally realized. That means the federal upside may not fully carry over once state taxes enter the picture.

State-specific modeling may help estimate the impact.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.