Yes, some startup stock may end up with 0% federal tax on gain - but only if a tight set of tax rules line up. In plain English: an 83(b) election may start the clock early, and QSBS may allow a 100% federal gain exclusion after 5+ years. But that result may apply only to eligible shares, only up to the federal cap, and state tax may still apply.

Here’s the short version:

- 83(b) may let me get taxed when stock is granted or early exercised, instead of at vesting.

- If the stock value at that time is close to what I paid, the upfront tax may be $0 or close to $0.

- That earlier tax timing may also start the QSBS holding period sooner.

- QSBS may exclude 100% of federal capital gain after 5 years if the company and shares meet Section 1202 rules.

- For stock issued after July 4, 2025, the federal gain cap may be $15,000,000 or 10x basis, whichever is greater.

- For stock issued on or before July 4, 2025, the cap may be $10,000,000 or 10x basis.

- Miss the 30-day 83(b) deadline, and the result may change a lot.

- RSUs, SAFEs, convertible notes, and unexercised options usually do not start the QSBS clock right away.

- Even if federal tax on gain ends up at 0%, state tax may still apply in some states.

If I had to sum up the whole article in one line, it would be this: 83(b) may start the clock, but QSBS decides whether the gain may be excluded.

83(b) Election + QSBS: How They Work Together for 0% Federal Tax

The $10 Million Tax Secret: 83(b) Election & QSBS Explained (Founder & Startup Employee Guide) 🤯💰

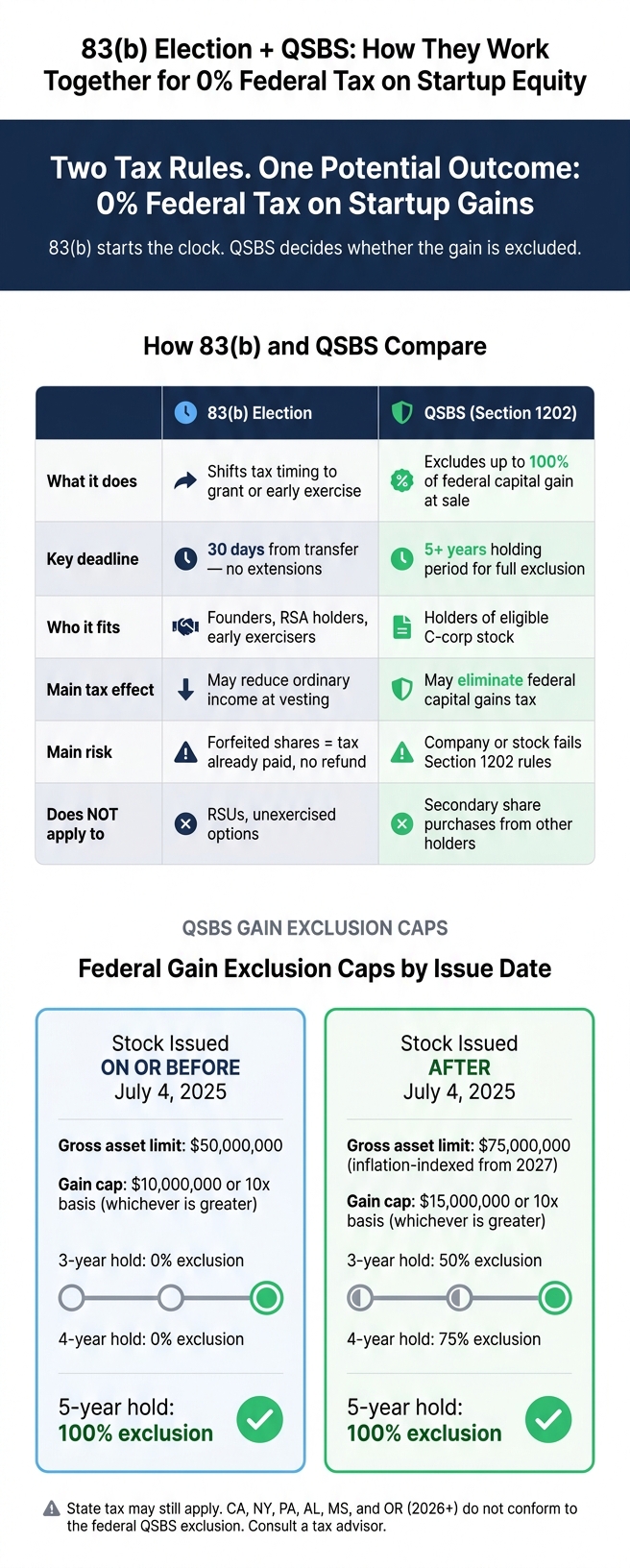

Quick Comparison

| Topic | 83(b) election | QSBS |

|---|---|---|

| What it does | May shift tax timing to grant or early exercise | May exclude federal gain at sale |

| Main deadline | 30 days from transfer or early exercise | Usually 5+ years for full exclusion |

| Who it fits | Founders, RSA holders, early exercisers | Holders of eligible C-corp stock |

| Main tax effect | May reduce ordinary income later | May reduce federal capital gains tax later |

| Main risk | Forfeited shares may leave tax already paid | Company or stock may fail Section 1202 rules |

| Applies to | Unvested stock actually issued | Qualified small business stock |

| Does not usually apply to | RSUs, unexercised options | Secondary purchases from other holders |

This article breaks down when this setup may work, when it may fail, and what facts may change the tax result.

83(b) Elections: Starting the Clock Early

By default, unvested stock may be taxed when it vests. Each vesting event may create ordinary income based on the spread between fair market value and what you paid, even if you may not be able to sell the shares yet. In plain English: you may owe tax before you have a way to turn those shares into cash.

An 83(b) election changes when that tax event happens. You send a notice to the IRS asking to be taxed when the stock is granted, or when you early exercise, instead of waiting for vesting. If the shares are issued when fair market value matches what you paid - which may happen for founders at formation - your immediate taxable income may be $0. Any later gain may be taxed as capital gain instead of ordinary income. That shift in timing may matter for another reason too: it may start the QSBS holding period earlier.

Which Types of Equity Can Use an 83(b) Election

The election applies to unvested stock received for services. In practice, that usually includes the following:

| Equity Type | Eligible for 83(b)? | Notes |

|---|---|---|

| Founder common stock | Yes | Often issued at formation and subject to vesting |

| Restricted stock awards (RSAs) | Yes | Shares issued directly to employees or advisors |

| Shares from early-exercised options | Yes | Only if the plan allows exercise before vesting; 83(b) applies to the shares, not the option grant |

| Unexercised options | No | 83(b) applies to unvested property |

| RSUs | No | They are a promise to issue shares later |

Tax Mechanics and the 30-Day Deadline

You have 30 calendar days from the transfer date or early exercise date to file. There are no extensions.

The taxable income at filing equals fair market value minus the amount you paid. Here’s a simple example. A founder receives 2,000,000 shares at $0.0001 per share, for a total cost of $200. If the fair market value at grant is also $0.0001 per share, the immediate taxable income may be $0. Three years later, if those shares are worth $2.00 each, the founder may owe no ordinary income tax on that appreciation, because the tax event already occurred at grant.

File electronically or send it by certified mail, and keep proof that it was filed on time.

What Can Go Wrong Whether You File or Not

Filing early may lock in a low tax basis and may start the QSBS five-year clock right away. But it’s not risk-free.

If you leave the company before the shares fully vest, you may forfeit those shares. And if that happens, you generally don’t get the tax back. You may only be able to claim a capital loss for the amount you paid for the stock.

If you don’t file an 83(b) election, each vesting tranche may start its own QSBS clock. That may push the exclusion date out further.

Once that clock starts, the next issue is whether the stock meets the QSBS rules.

QSBS Rules: When Startup Stock Qualifies for a 100% Federal Gain Exclusion

An 83(b) election may matter only if the stock also qualifies as QSBS under Section 1202. The clean way to check it: start with the company rules, then look at the shareholder rules.

Company Requirements to Verify

The issuing company must be a U.S. C corporation when it issues the stock and through most of your holding period. S corporations, LLCs, and partnerships do not qualify. If a startup began as an LLC and later converted to a C corp, the QSBS holding period may start only when the C corp shares were issued, not when the business was first founded.

Two asset tests apply at issuance. The company's gross assets - cash plus the tax basis of property - must remain below the limit immediately after issuance, and passive assets may not exceed 10% of total assets.

The gross asset limit depends on the issue date:

| Feature | Shares Issued ≤ July 4, 2025 | Shares Issued > July 4, 2025 |

|---|---|---|

| Gross asset limit | $50,000,000 | $75,000,000 (inflation-indexed from 2027) |

| Per-issuer gain cap | $10,000,000 or 10x basis | $15,000,000 or 10x basis |

| 3-year hold | 0% exclusion | 50% exclusion |

| 4-year hold | 0% exclusion | 75% exclusion |

| 5-year hold | 100% exclusion | 100% exclusion |

For shares issued on or before July 4, 2025, the limit is $50,000,000. For shares issued after that date, it rises to $75,000,000, with inflation adjustments starting in 2027.

Some lines of business do not qualify. That includes certain service businesses and some asset-heavy businesses.

Redemptions around the issuance date may also create problems. If the company redeems stock from you or related persons within two years before or after issuance, or redeems more than 5% of its total stock within one year before or after issuance, the stock may lose QSBS treatment.

Shareholder Requirements and Exclusion Limits

On the shareholder side, the stock must be acquired directly from the corporation in exchange for money, property, or services. Shares bought from another shareholder in a secondary sale do not qualify, even if they are held for many years afterward.

The exclusion cap and holding-period setup depend on when the shares were issued. Older shares follow the prior rule set. Shares issued after July 4, 2025, may qualify for partial exclusion after three or four years, and full exclusion after five years.

Only non-corporate taxpayers may qualify. That group includes individuals, certain trusts, and pass-through entities.

Federal vs. State Tax Treatment

Even if the federal rules line up, the state result may look different. The 100% exclusion applies only at the federal level. In nonconforming states, you may still owe state tax even when the federal gain exclusion applies.

California, New York, Pennsylvania, Alabama, and Mississippi do not conform. Oregon decoupled from federal treatment starting in 2026, while New Jersey began conforming as of January 1, 2026.

Next, see how 83(b) and QSBS stack in founder shares, restricted stock, and early exercise.

How 83(b) and QSBS Work Together

Why Combining Both Can Produce 0% Federal Tax on Eligible Gain

The main idea comes down to timing. An 83(b) election may move the QSBS holding period start date earlier, which may make 0% federal tax on eligible gain possible later on. But that only lines up if the stock also meets the QSBS rules.

A common setup looks like this: someone receives stock, or early-exercises stock, when the fair market value is still low, files the 83(b) election on time, holds the shares for more than five years, and the company continues to meet QSBS requirements before a sale. In that fact pattern, the tax result may be much better than it would have been otherwise.

3 Scenarios: Founder Shares, Restricted Stock, and Early Exercise

The three examples below show when this setup may work and when it may not.

Scenario 1 - Founder shares (qualifies): A founder receives 2,000,000 shares at $0.0001 per share in a qualifying C-corp and pays $200 total. She files the 83(b) election within 10 days. Because the FMV matches the purchase price, the filing creates no immediate income, and the five-year QSBS clock starts right away for all shares.

Scenario 2 - Early exercise (qualifies): An early employee early-exercises 100,000 unvested options at $0.10 per share and pays $10,000 total. He files the 83(b) election right away. The QSBS clock starts on the exercise date for all 100,000 shares.

Scenario 3 - Missed deadline (does not qualify): A late-stage hire receives restricted stock from a company that is not QSBS-eligible and misses the 30-day filing window. Without the 83(b) election, she may face ordinary income tax on the spread as each tranche vests, and the stock may not qualify as QSBS.

Comparison Table: When This Strategy Works and When It Does Not

Here’s the side-by-side view.

| Feature | 83(b) filed + QSBS eligible | 83(b) only | No 83(b) filed |

|---|---|---|---|

| QSBS clock start | Grant/issuance date for restricted stock; exercise date for early-exercised options | Same as left column, but no QSBS exclusion | Restricted stock: each vesting tranche; options: exercise date |

| Tax at vesting | $0 | $0 | Ordinary income tax on FMV spread |

| At sale, if held more than five years | Potential 0% federal tax on eligible gain | Capital gains treatment on later appreciation | Potential 0% only for shares or tranches that separately satisfy QSBS rules |

| Main risks | Forfeiture of prepaid tax; company failure | Forfeiture of prepaid tax; company failure | Ordinary income with no sale proceeds |

State tax may still apply even if federal tax is fully excluded.

Next: use the filing and QSBS checklists to confirm the deadlines and company tests.

Checklists, Common Mistakes, and Key Takeaways

Use these checklists to double-check the facts before you file or sell.

83(b) Filing Checklist and Documentation

The 30-day 83(b) deadline is absolute.

Don't wait on HR. The 30-day clock usually starts on the grant date or board approval date, often before the full paperwork shows up.

If you file online, use IRS Form 15620 through the IRS portal for immediate confirmation. If you file on paper, mail the election by certified mail with return receipt requested to the IRS Service Center where you file your annual return. For mailed filings, USPS now treats the processing date as the postmark date.

After filing, keep your certified mail receipt or electronic confirmation. Share a copy with your company's HR or payroll team, and send one to your tax preparer. Your filing must include:

- Name and address

- Social Security number

- Description of the property

- Date of transfer

- Nature of the restrictions

- Fair market value at transfer

- Amount paid

83(b) may help only if the stock also qualifies as QSBS.

QSBS Qualification Checklist and Ongoing Monitoring

QSBS status depends on rules that may need to hold through the full holding period.

| Category | What to Verify | Documentation to Keep |

|---|---|---|

| Entity type | Domestic C-corp at issuance and throughout the holding period | Articles of Incorporation; tax returns |

| Original issuance | Shares acquired directly from the company | Stock Purchase Agreement; stock certificate |

| Gross assets | ≤ $50 million for stock issued on or before July 4, 2025, or ≤ $75 million for stock issued after July 4, 2025, at issuance | 409A valuations; balance sheets |

| Active business | At least 80% of assets used in a qualified trade or business | QSBS attestation letters |

| Excluded industries | Not a professional services, financial, hospitality, farming, or mining business | Company business description or charter |

| Holding period | 5+ years for 100% exclusion; 3 years for 50%, 4 years for 75%, and 5 years for 100% on post-July 4, 2025 stock | 83(b) election; exercise/issuance records |

| Redemptions | No disqualifying buybacks by the company within two years before or after issuance, or by other shareholders within one year before or after | Cap table history; redemption agreements |

Ask the company for a QSBS attestation letter at issuance, then update it at each financing round. Also track asset growth after issuance. Shares issued after the company goes over the threshold may not qualify.

Conclusion: The Conditions That Matter Most

A 0% federal tax result may be possible only when 83(b) and QSBS line up. An 83(b) election is a strict timing move with no extensions or exceptions. QSBS follows a strict eligibility framework that may call for periodic tracking. When both line up - the election is filed on time, the company qualifies, and the holding period is met - gains may qualify for a full federal exclusion up to $10 million for pre-July 4, 2025 stock, or the greater of $15 million or 10x adjusted basis for post-July 4, 2025 stock.

State tax may still apply in nonconforming states.

The controlling rule is simple: 83(b) starts the clock, and QSBS decides whether the gain may be excluded.

FAQs

How do I know if my stock is actually QSBS-eligible?

Check whether the stock may have met the QSBS rules at original issuance.

That usually means looking at a few core points:

- The stock was issued by a domestic C corporation

- You acquired it directly from the company for cash, property, or services

- The company’s gross assets may have been under $75 million after July 4, 2025, or $50 million on or before that date

- The company may have been engaged in a qualified active business for substantially all of your holding period

If you received restricted stock, an 83(b) election filed within 30 days may help start the holding period at that point. It also may make sense to keep records like your stock purchase agreement and financial statements.

What happens if I file an 83(b) election and leave the company?

You may have paid more in taxes than you end up needing to. With an 83(b) election, you pay income tax upfront based on the stock’s fair market value at the time of grant, and those taxes are not refundable.

That creates a clear tradeoff. If you leave the company and forfeit unvested shares, you may have already paid tax on equity you never fully earned. That’s the main risk people often weigh against the possible tax upside.

Can I still get QSBS treatment if I missed the 83(b) deadline?

No. The 83(b) election deadline may be 30 days from the grant or purchase date, and there are generally no extensions. If that window is missed, the election may be treated as invalid.

Without a timely 83(b) election, your QSBS holding period may usually start when the shares vest, not when they were granted. That timing shift may delay the five-year clock and may reduce or eliminate possible QSBS tax treatment.

Disclosures:

- This content is for informational purposes only and does not constitute investment, tax, or legal advice. Please consult a qualified professional regarding your specific situation.

- Tax laws and regulations are subject to change and may vary by jurisdiction. The examples provided are illustrative only and may not apply to your circumstances.

- Past performance is not indicative of future results. No guarantee of future outcomes is implied.

- State tax treatment may differ from federal tax treatment. Consult your state tax authority or a tax professional for details.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.