If one company makes up more than 10% to 15% of your liquid net worth, your finances may be leaning too hard on a single stock. That risk may be even higher when the same company also pays your salary.

Here’s the short version: I may look at all employer-stock exposure across all accounts, set a written cap, use preset sale rules like selling RSUs at vest, and reinvest outside the company. I may also check taxes before selling, since RSUs, ESPPs, NSOs, and ISOs may each be taxed in different ways.

At a glance, the article covers:

- What “concentrated” may mean: often above 10% to 15% of liquid net worth, and for some people even 5% to 10% of an investment portfolio

- Why employer stock may carry extra risk: job income and portfolio value may both be tied to the same company

- Where concentration may build up: RSUs, ESPPs, stock options, 401(k) company stock, deferred comp, and older grants

- Why selling may be delayed: blackout windows, trading rules, and waiting for tax treatment

- How some people deal with it: written caps, quarterly reviews, sell-at-vest rules, lot selection, and scheduled sales

- How taxes may shape decisions: RSU vesting, ESPP sale rules, NSO ordinary income, ISO AMT, capital gains, and tax-loss offsets

- Other paths some investors use: 10b5-1 plans, donor-advised funds, exchange funds, collars, and completion portfolios

A simple idea runs through the whole piece: a vested share may still be a choice to stay concentrated. Writing down rules ahead of time may make that choice less emotional and more consistent.

Managing Concentrated Stock Risk: From Concentration to Confidence

Map every way employer stock enters your finances

Employer stock may build up through a few different pay channels, often without looking dramatic at first. So the first step may be simple: break the position down by source.

How RSUs, ESPPs, and stock options each add to your position

RSUs add shares automatically on each vest date. Since they’re taxed as ordinary income when they vest, selling soon after vesting may be the simplest point to trim exposure.

ESPPs work a bit differently. Payroll deductions build up during the purchase period, then the plan buys shares, often at a discount to the market price. That may keep adding to the position over time.

Stock options - both ISOs and NSOs - may increase exposure all at once. Exercising a large grant may create a concentrated holding in a single transaction. ISOs may add another layer because holding periods may be required for tax treatment that some employees prefer, which may delay diversification.

Plan rules that can delay or limit your exit options

Next, check whether trading rules may delay an exit. Blackout periods and trading windows may block trades for large parts of the year. A Rule 10b5-1 plan may be set up during an open trading window so scheduled sales may still go through during later blackout periods.

A simple fix may be a calendar. Track grant dates, vest dates, and blackout dates in one place.

Add up your total employer stock exposure across all accounts

A common mistake may be checking only the most visible account. A full picture may require looking at every place employer stock may show up:

| Account Type | How Employer Stock Appears | Commonly missed? |

|---|---|---|

| Taxable brokerage | Vested RSUs, ESPP shares, exercised options | No |

| 401(k) | Company stock fund option within the plan | Yes |

| ESPP account | Shares held after the purchase period closes | Sometimes |

| Deferred compensation | Payouts tied to company stock value | Yes |

| Old grants, pre-IPO shares, or inherited shares | Older grants, pre-IPO shares, or inherited stock | Yes |

From there, some people divide total employer stock value by liquid net worth - cash, brokerage accounts, and retirement accounts combined. With the full tally in hand, it may be easier to set a cap and sell down in a steady way.

Set concentration limits and written rules before emotions take over

Once you know your total exposure, turn that number into a rule you may follow without having to rethink it each time.

Pick a hard cap for employer stock

After you total your exposure, set a written cap before the stock moves. A practical starting point may be 10%. Shorter time horizons may call for lower caps. If you're within five years of retirement, a home purchase, or paying for college, one bad year may throw off a specific timeline.

A useful gut check:

would you buy this much company stock with cash today?

Write a short employer-stock policy

A cap may only work if it turns into an automatic rule at vest, exercise, and sale. A written policy removes the need to make a new decision every time shares vest or the stock jumps. One simple version: sell most RSUs at vest, and set preplanned rules for ESPP shares and option exercises.

The idea is plain: a vested share isn't a free hold. It may be better viewed as a choice to stay concentrated.

Check for drift after vests, exercises, and price jumps

Even a good cap may fall apart if you don't revisit it when new shares arrive. A vest, exercise, or sharp rally may push you past your cap fast. That's why a quarterly review may make sense. A recurring calendar reminder on the first Monday of each quarter may work well.

The calendar alone may not be enough. Any RSU vest, option exercise, or major price jump may also trigger a review. If a stock drop would change your retirement, home, or career plan, the position may be too large to ignore.

Build a disciplined selling and reinvestment plan

Ways to Reduce Concentrated Employer Stock: Strategy Comparison Guide

Use repeatable sale rules instead of waiting for the right price

Once you have a cap, a preset sale rule may help you get back under it. Waiting for the "right price" may let concentration grow for years. A repeatable rule takes that call off your plate.

The simplest place to start is sell-at-vest. Each vest adds to the same concentration you already measured. When RSUs vest, the cost basis resets to the fair market value on that day, so an immediate sale may be tax-efficient and may leave little or no capital gain between vest and sale.

For appreciated lots, some people trim on a fixed quarterly schedule until they are back under their target cap.

If you face insider-trading restrictions or blackout windows, a prearranged Rule 10b5-1 plan may be used.

Reinvest proceeds into your target allocation

Selling only reduces risk if the cash moves away from your employer's orbit. Proceeds may be redirected into assets that diversify away from your employer's stock - a total U.S. market index fund, an international stock fund, and a bond fund are common choices.

There’s one easy trap here. If you work in tech and reinvest into a tech-heavy fund, your exposure may still lean in the same direction. In that case, the position changed, but the risk may not have changed much.

One more refined option is the completion portfolio approach. With this setup, the rest of the portfolio is built to underweight your employer’s sector, so the broader mix may offset some of the concentration instead of adding to it.

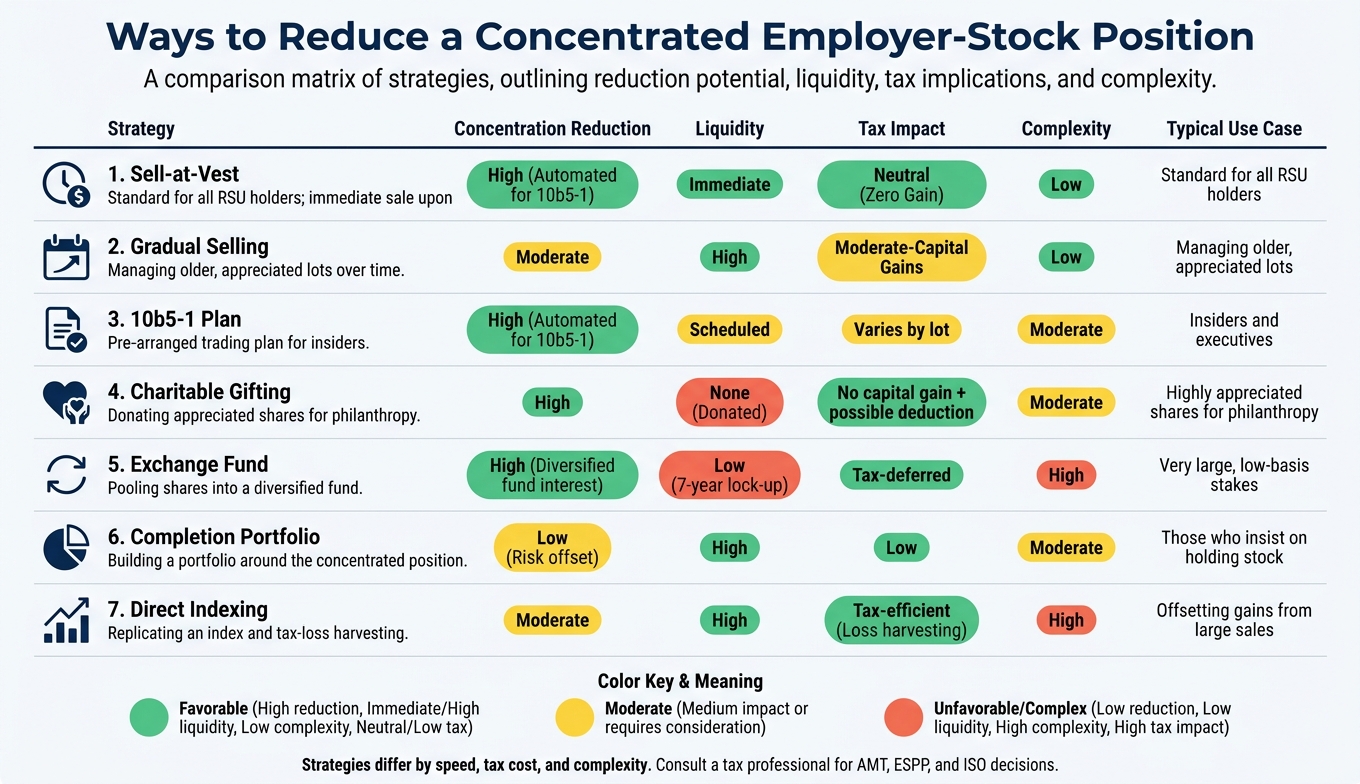

Comparison table: ways to reduce a concentrated employer-stock position

These methods differ mainly by speed, tax cost, and complexity.

| Strategy | Concentration Reduction | Liquidity | Tax Impact | Complexity | Typical Use Case |

|---|---|---|---|---|---|

| Sell-at-Vest | High | Immediate | Neutral (Zero Gain) | Low | Standard for all RSU holders |

| Gradual Selling | Moderate | High | Moderate (Capital gains) | Low | Managing older, appreciated lots |

| 10b5-1 Plan | High (Automated) | Scheduled | Varies by lot | Moderate | Insiders and executives |

| Charitable Gifting | High | None (Donated) | No capital gain; possible deduction | Moderate | Highly appreciated shares for philanthropy |

| Exchange Fund | High (diversified exchange fund interest) | Low (7-year lock-up) | Tax-deferred | High | Very large, low-basis stakes |

| Completion Portfolio | Low (Risk offset) | High | Low | Moderate | Those who insist on holding stock |

| Direct Indexing | Moderate | High | Tax-efficient (Loss harvesting) | High | Offsetting gains from large sales |

Gifting appreciated shares to a donor-advised fund may eliminate capital gains and may generate a charitable deduction. This route may be most useful when shares have a very low cost basis.

Exchange funds pool your shares with other concentrated investors in exchange for a diversified fund interest, but they require a seven-year lock-up and are generally used for very large, low-basis positions.

Tax lot choice comes next.

Handle taxes and set up a system that keeps concentration from rebuilding

Factor in tax lot and compensation type before you sell

Once you set a sale rule, the next step is deciding which shares to sell first. That choice may shape the tax hit just as much as the timing of the sale.

Different share types may be taxed in different ways:

- RSUs: Taxed at vest, so selling soon after vesting may create little added taxable gain.

- ESPPs: Gains are split between ordinary income and capital gains; early sales may increase the ordinary-income share.

- NSOs: May trigger ordinary income at exercise, then capital gains on later appreciation.

- ISOs: May avoid ordinary income at exercise but may trigger AMT.

Two practical moves may reduce friction. First, use specific-lot selection. In plain English, that means selling the most recently vested shares before touching older lots with large embedded gains. Second, some people spread sales across tax years to stay under the thresholds tied to the 20% long-term capital gains rate and the 3.8% NIIT.

If you have losses elsewhere in your portfolio, those losses may offset capital gains from a concentrated stock sale.

Use Mezzi to surface shares with the highest cost basis and track employer-stock exposure across accounts; consult a tax professional for AMT, ESPP, and ISO decisions.

That may leave the highest-basis shares and the exits that are most tax-sensitive.

When to consider charitable giving and advanced exit strategies

If tax on a direct sale may be too high, some investors look at more advanced exit tools. For low-basis shares that have appreciated a lot, a standard sale may create a large tax bill.

Donating appreciated shares directly to a donor-advised fund (DAF) may let you avoid capital gains tax on those shares while claiming a fair-market-value charitable deduction. This approach is often used for the oldest, most appreciated lots.

Protective puts and collars may limit downside risk, but they add cost and complexity and may cap upside.

Exchange funds may diversify a concentrated position on a tax-deferred basis by contributing low-basis shares into a pooled portfolio, though they usually require a seven-year lock-up and are generally practical only for very large positions.

Conclusion: A simple, written system beats ad hoc decisions every time

A simple system may work better than making each decision on the fly: define the rule, follow it, and review it on a set schedule.

The core issue with employer stock concentration usually isn't a lack of awareness. Many people know the risk. The problem is that the rules for handling it often never get written down. Without a written policy, inertia may take over. Every vest, every price jump, and every option expiration may turn into a new decision made under pressure.

A written policy reviewed quarterly, paired with full-picture monitoring in Mezzi to track total employer-stock exposure across all accounts, may be the simplest setup that holds up in practice.

FAQs

How much employer stock is too much?

There’s no single rule that fits everyone. But concentration risk may start to matter once one stock makes up about 5% to 20% of your investable assets.

A lot of experts point to 10% as the level where one holding may add meaningful, uncompensated risk.

For employees, the picture may be even tighter than it first appears. Your paycheck, career path, and unvested equity may already be tied to your employer. So even 10% in company stock may be more exposure than some people are comfortable with.

Should I sell my RSUs as soon as they vest?

It depends on your total exposure to your employer’s stock and your tolerance for risk.

Selling at vest is a common way some people use to reduce concentration risk. And because your cost basis may be the fair market value at vesting, selling right away may result in no added capital gains tax at that point.

If you hold the shares, you may face short- or long-term capital gains taxes later. At the same time, your concentration risk may increase.

Some experts suggest keeping employer stock at 10% to 20% of net worth.

What taxes should I check before selling employer stock?

Check the equity type first, since taxes may differ.

RSUs are taxed as ordinary income at vesting, and employer withholding may not cover your full tax rate. ISOs may trigger AMT at exercise, while NSOs are taxed as ordinary income at exercise.

For ESPPs, review the holding periods, since selling early may mean higher short-term capital gains instead of long-term rates. Also confirm whether gains are short-term or long-term, and reconcile your W-2 and cost basis.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.