If you hold startup shares, the key issue may be timing. For stock issued after July 4, 2025, some holders may exclude the greater of $15,000,000 or 10x basis from federal capital gains tax. But that tax treatment may depend on when the shares were issued, when options were exercised, whether the company was a C corporation, whether assets stayed under the limit, and whether you held the stock long enough.

Here’s the short version:

- QSBS applies to stock, not just equity grants. For options, the clock may start at exercise, not grant.

- Original issuance matters. Shares bought from another holder on a secondary sale may not qualify.

- Company status matters. The business may need to be a domestic C corporation when the stock is issued.

- Asset limits matter. The company may need to be under $50 million in gross assets for stock issued on or before 7/4/2025, or under $75 million for stock issued after that date.

- Holding time matters. For newer stock, the federal exclusion may be 50% after 3 years, 75% after 4 years, and 100% after 5 years.

- Paperwork matters. An 83(b) election, exercise records, stock agreements, and company records may all affect the result.

- State taxes may differ. Federal exclusion does not always mean state-level exclusion.

If I were scanning this before a sale, I’d focus on one thing first: the date my actual shares started. That one date may affect the QSBS clock, the asset test, and how much gain may be excluded.

How to Avoid Capital Gains Tax on Startup Stock (QSBS Explained)

Quick comparison

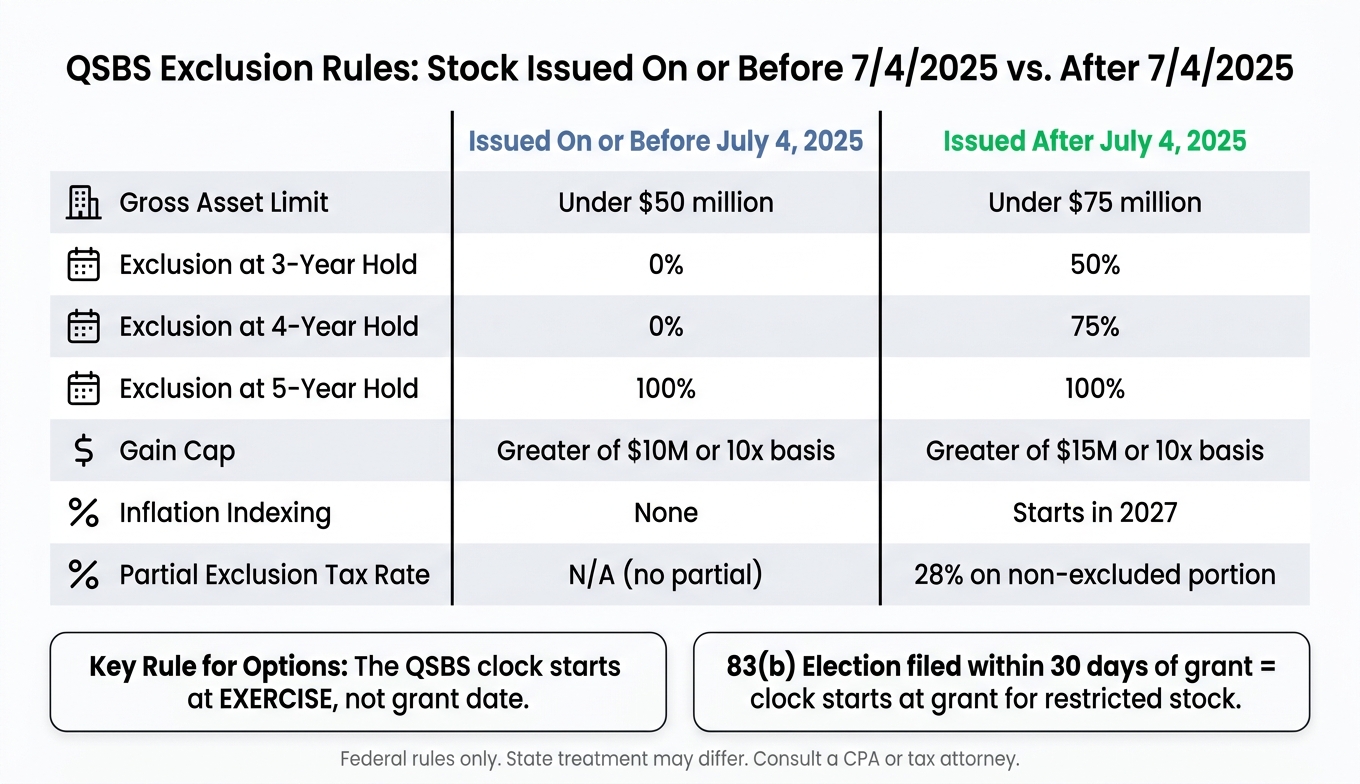

| Topic | Stock issued on or before 7/4/2025 | Stock issued after 7/4/2025 |

|---|---|---|

| Gross asset limit | Under $50 million | Under $75 million |

| Exclusion after 3 years | 0% | 50% |

| Exclusion after 4 years | 0% | 75% |

| Exclusion after 5 years | 100% | 100% |

| Gain cap | Greater of $10 million or 10x basis | Greater of $15 million or 10x basis |

This article may help you sort the rules, spot common mistakes, and gather the records a CPA or tax attorney may ask for before a liquidity event.

What is qualified small business stock?

QSBS defined under Section 1202

Qualified Small Business Stock (QSBS) refers to the Section 1202 federal capital-gains exclusion for stock in a qualifying domestic C corporation. In plain English: eligible shareholders may exclude some or all federal capital gains when they sell qualifying shares. This is a federal tax rule, and state treatment may differ. California does not conform, and New Jersey follows the federal framework for tax years beginning Jan. 1, 2026.

There’s one rule that trips people up fast: the shares must come directly from the company at original issuance. That means the stock must be acquired in exchange for money, property, or services. If shares are purchased from another shareholder on a secondary market, they do not qualify, no matter how long they’re held.

From there, eligibility may turn on a set of company, stock, and holding-period rules.

Why startup employees and founders should pay attention

For stock issued after July 4, 2025, eligible holders may exclude the greater of $15 million or 10 times their adjusted basis per issuer in federal capital gains. With a 23.8% federal long-term capital gains rate, the potential tax difference may be large.

This may matter for startup employees and founders because common stock, founder shares, and shares acquired by exercising ISOs or NSOs may qualify. In an IPO or acquisition, that may translate into a big gap between taxable gains and excluded gains.

But there’s a catch: the outcome may depend on how the shares were issued, when the options were exercised, and when the shares were sold.

How QSBS fits with option and sale timing

QSBS doesn’t sit off to the side. It ties into ISO and NSO exercise timing, 83(b) elections, and long-term capital gains holding periods. If someone early exercises and files an 83(b) election within 30 days, the QSBS holding period may start right away.

It’s also not automatic. Qualification may depend on choices made by the company, such as entity type, gross assets at issuance, and active business use. It may also depend on shareholder decisions, including when to exercise and when to sell.

Those timing decisions set up the eligibility rules that come next.

The rules that determine QSBS eligibility

QSBS Tax Exclusion: Before vs. After July 4, 2025 Stock Issuance

Company and stock requirements

The issuing company must be a domestic C corporation at the time of issuance. S corporations, LLCs, and partnerships don't qualify, although they may convert and start the QSBS clock from that point forward.

Buying shares from another shareholder does not count. For startup employees, the exercise date may matter more than the grant date.

The company also has to meet a gross asset test at issuance. Cash plus the adjusted tax basis of property must stay under $50 million for stock issued on or before July 4, 2025, or $75 million for stock issued after that date.

For startup employees, that often comes down to one thing: were the shares acquired before the company crossed the asset threshold? If an employee exercises after the company crosses that limit, the shares may lose QSBS status.

There’s another filter too. At least 80% of the company's assets must be actively used in a qualified trade or business. Some industries are excluded, including:

- Healthcare services

- Law

- Accounting

- Consulting

- Financial services

- Banking

- Insurance

- Hospitality, including hotels and restaurants

- Farming

- Natural resource extraction, such as mining or oil and gas

Businesses in those sectors generally do not qualify.

Holding period, exclusion percentages, and sale timing

Once the company and stock qualify, timing becomes the next test.

The QSBS clock starts when you acquire the shares, not when you get the grant. For options, the clock starts at exercise.

For stock issued on or before July 4, 2025, you need to hold the shares for more than 5 years to get any exclusion. Stock acquired before September 27, 2010 may also create an AMT preference item.

Stock issued after July 4, 2025 works differently. The OBBBA added a tiered exclusion schedule: 50% after 3 years, 75% after 4 years, and 100% after 5 years.

There’s a catch with partial exclusions. The non-excluded portion of gains at the 3- or 4-year mark is taxed at a flat 28% rate, which is higher than the standard long-term capital gains rate. So an earlier sale may still come with a meaningful tax cost.

Gain limits, rollovers, and red flags

After timing comes the cap: how much gain QSBS may actually shield.

The exclusion cap depends on when the stock was issued. The per-issuer cap is the greater of $10 million or 10 times your adjusted basis for stock issued on or before July 4, 2025, and the greater of $15 million or 10 times your adjusted basis for stock issued after that date.

| Feature | Issued on or before 7/4/2025 | Issued after 7/4/2025 |

|---|---|---|

| Exclusion cap | Greater of $10M or 10x basis | Greater of $15M or 10x basis |

| Gross asset limit | $50 million | $75 million |

| 3-year hold | 0% exclusion | 50% exclusion |

| 4-year hold | 0% exclusion | 75% exclusion |

| 5-year hold | 100% exclusion | 100% exclusion |

| Inflation indexing | None | Starts in 2027 |

If liquidity comes up before 5 years, a Section 1045 rollover may defer gain after a 6-month hold.

A few red flags may disqualify shares. Significant corporate redemptions are a common one. If the company redeems more than 5% of its outstanding stock within the two-year window before or after issuance, or if there are certain redemptions from you or a related person during that same period, the stock may be tainted.

How to apply QSBS rules to your own startup equity

A quick screen for common startup equity situations

Start with four checks: direct company issuance, domestic C-corp status, a qualified trade or business, and gross assets below the limit that applied at issuance - $50 million or $75 million, depending on the date. If all four line up, the shares may be potentially QSBS-eligible.

RSUs usually start the QSBS clock at settlement. In many cases, that may leave less time before an exit. RSAs work differently. With a timely 83(b) election, the clock starts at grant.

If the shares pass that screen, the next step may be figuring out when the holding period starts.

Options, early exercise, and founder stock

For ISOs and NSOs, the QSBS clock starts at exercise, not grant. Time spent holding the option does not count.

Early exercise may start the clock while the company is still under the asset limit. For founders, the clock starts when the corporation issues the shares. For restricted stock, a timely 83(b) election starts the clock at grant. Missing that 30-day window may cost years of holding-period credit.

How QSBS changes the math at a liquidity event

Once eligibility looks clear, the next issue may be whether to sell, wait, or roll the gain. The cap stays fixed. Timing may affect how much of it gets used.

- Sell before 5 years: no exclusion for stock issued on or before July 4, 2025; partial exclusion may apply for later stock.

- Sell after 5 years: full exclusion up to the applicable cap.

- Section 1045 rollover: defer gain by reinvesting in new QSBS within 60 days.

That makes issuance dates, exercise dates, and 83(b) filings the next facts to verify.

Records, common mistakes, and how Mezzi can help

What records to collect and how to track them

QSBS often comes down to two things: dates and company facts. That’s why paperwork may matter just as much as eligibility.

Keep the documents that support QSBS treatment, including stock purchase agreements, grant papers, board approvals, financial statements showing the company stayed under the asset cap, the 409A valuation, and any 83(b) filing proof.

If you filed an 83(b) election, hold on to the original form and your IRS filing confirmation, such as a stamped copy or certified mail receipt. That documentation may establish that your holding period started at grant rather than vesting. The key point here isn’t just the rule. It’s the proof that you followed it.

Annual company attestation letters may also add a useful layer of support, if they’re available. It may also help to keep records showing the company met the active-business test during your holding period, along with any record of company stock redemptions within two years of your issuance.

Track each grant or exercise as its own lot. Different exercise dates may lead to different acquisition dates, different asset-test snapshots, and different eligibility results, even for shares from the same company.

Mistakes that commonly cost employees the benefit

In many cases, the biggest problems come from missing paperwork or waiting too long to exercise.

Waiting may be the costliest mistake. If you exercise after the company crosses the asset limit, those shares may no longer qualify at the time of exercise.

Selling just before the five-year mark may also wipe out the exclusion. For stock issued on or before July 4, 2025, selling even one day early means no exclusion.

State taxes are another place people may get caught off guard. California, New York, New Jersey, and Pennsylvania do not conform to the federal Section 1202 exclusion, so gains that are excluded at the federal level may still be taxed by the state.

Using Mezzi to track timing, concentration, and tax decisions

Once the facts are documented, the next step may be keeping each lot and exercise date in one place. Mezzi connects to taxable and brokerage accounts, along with option exercise history, through read-only account connections. You keep your assets where they are, and no account transfers are required.

For QSBS, that may mean seeing the full picture in one dashboard: which lots were exercised when, which ones are getting close to the five-year mark first, and how a possible sale may fit with concentration risk, retirement timing, and state tax exposure.

Mezzi may also help you compare the tax difference between selling in year four and waiting for the full exclusion, and it may flag issues worth reviewing with a CPA or tax attorney before a deal closes.

Good records and lot-level tracking may preserve a tax break that’s easy to miss. Getting that paper trail in place before a sale may make a big difference.

FAQs

How do I know if my shares are QSBS-eligible?

Check that both the company and your shares meet Section 1202 rules. Your stock must be issued directly by a domestic C corporation, not bought from another shareholder.

The company may need to meet the gross-asset limit at the time of issuance and use at least 80% of its assets in a qualified active business. You also generally may need to hold the shares for more than five years. For options, the holding period starts when you exercise.

When does the QSBS holding period start for my equity?

The QSBS holding period usually begins when the C corporation issues the stock to you in exchange for cash, property, or services.

There are a few common timing twists:

- Founders with restricted stock: the holding period may begin on the purchase date if an 83(b) election is filed.

- Employee stock options: the holding period usually begins on the exercise date, not the grant date.

- Companies that started as an LLC: the clock usually begins only after the business converts to a C corporation.

That timing detail may sound small, but it may affect whether shares meet the required holding period for QSBS treatment.

What documents should I gather before a sale?

To support a potential tax exclusion, it may make sense to keep clean records during the full holding period. The IRS may question a claim years after a sale, so paperwork from the start may matter later.

Before a liquidity event, some people gather:

- Stock purchase or grant documents that show original issuance

- Board resolutions approving the issuance

- Your 83(b) election, if applicable

- Proof that the company was a domestic C corporation at the time

- Financial statements and records showing it met the asset and active business requirements

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.