A Roth conversion may cost more than income tax. If it pushes your Medicare income over an IRMAA line by even $1, you may face added Part B and Part D premiums two years later - from about $1,148 to $6,936 per person per year in 2026 figures.

Here’s the short version:

- I’d first estimate baseline MAGI before any conversion

- Then I’d compare that number with the next IRMAA threshold

- The gap between those two numbers, minus a $2,000 to $5,000 buffer, may show the amount that may fit

- I’d also check whether that amount may stay under my target tax bracket

- If the room looks small, some people split conversions across several lower-income years

- Timing may matter most in the years after retirement and before Social Security, RMDs, and age 63

That last point is easy to miss. Medicare usually looks back two years, so a conversion in 2026 may affect premiums in 2028. For some people, that may create a short window for larger conversions before IRMAA starts to matter.

Simple formula:

Safe conversion amount = (next IRMAA threshold − expected MAGI) − buffer

A few things that may trip people up:

- Tax-exempt municipal bond interest still counts for IRMAA

- The standard deduction does not lower IRMAA MAGI

- One big conversion may push income into a higher tax bracket and a higher IRMAA tier at the same time

- Smaller yearly conversions may give some households more control over both

If I were boiling the article down to one idea, it would be this: the “right” Roth conversion amount may be the amount that fits under both your next IRMAA line and your tax-bracket ceiling, in the lowest-income years available to you.

How Much Can You Convert to Roth Without Triggering IRMAA?

The three numbers you need before converting

2026 IRMAA Brackets: How a Roth Conversion Can Spike Your Medicare Premiums

Start with three numbers: your baseline MAGI, the next IRMAA threshold, and the conversion amount that may fit below it.

Then compare the conversion to the IRMAA threshold that may apply two years later.

How IRMAA, MAGI, and Roth conversions connect

IRMAA is a Medicare surcharge added to Part B and Part D premiums when income goes above certain thresholds. Medicare uses MAGI to measure income. MAGI equals your Adjusted Gross Income plus tax-exempt interest, such as municipal bond interest.

A Roth conversion adds the converted amount to your MAGI in the year of the conversion, which may lead to higher IRMAA two years later. If your income goes over a threshold by even $1, the full surcharge for that tier may apply.

Your safe conversion amount may be the next IRMAA threshold minus projected MAGI minus a buffer.

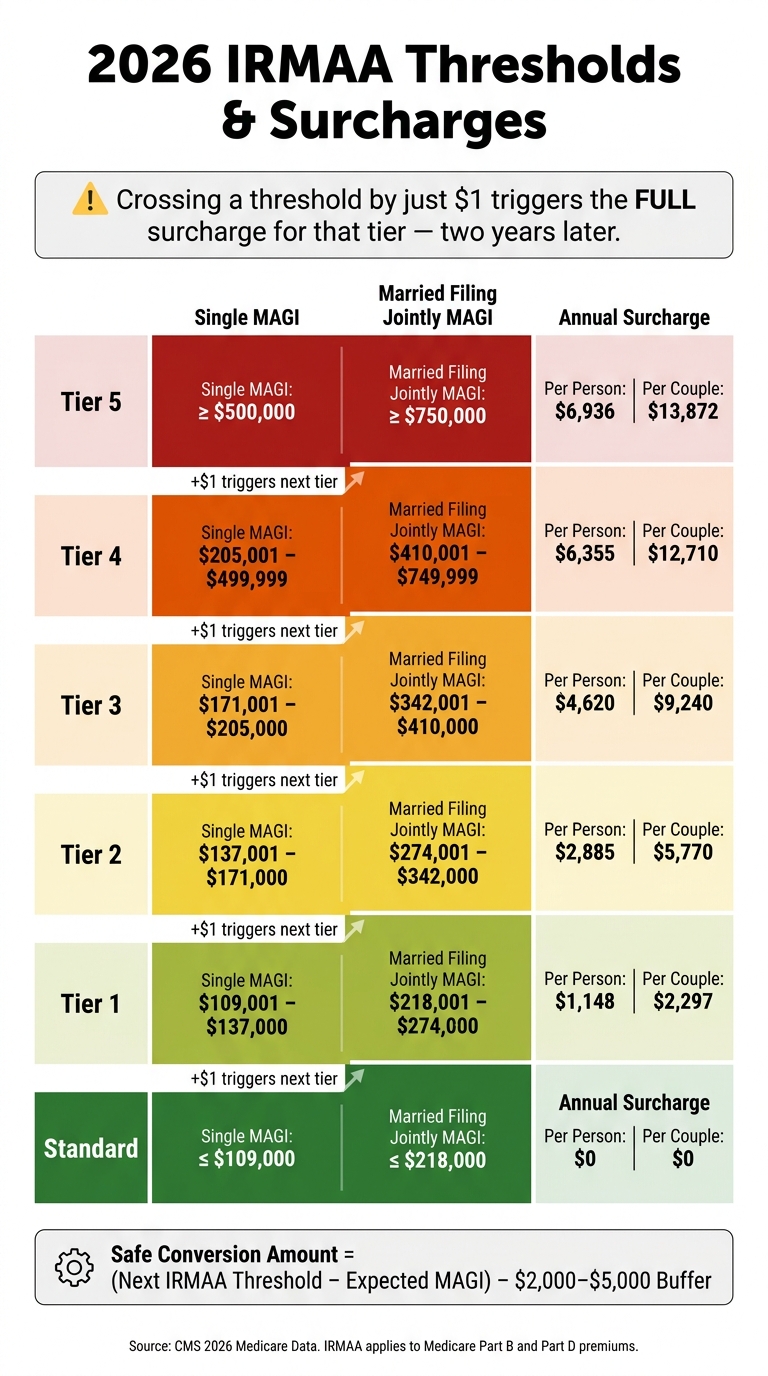

2026 IRMAA brackets for single and married filing jointly filers

| Tier | Single MAGI | Married Filing Jointly MAGI | Annual Surcharge (Per Person) | Annual Surcharge (Per Couple) |

|---|---|---|---|---|

| Standard | ≤ $109,000 | ≤ $218,000 | $0 | $0 |

| Tier 1 | $109,001 – $137,000 | $218,001 – $274,000 | $1,148 | $2,297 |

| Tier 2 | $137,001 – $171,000 | $274,001 – $342,000 | $2,885 | $5,770 |

| Tier 3 | $171,001 – $205,000 | $342,001 – $410,000 | $4,620 | $9,240 |

| Tier 4 | $205,001 – $499,999 | $410,001 – $749,999 | $6,355 | $12,710 |

| Tier 5 | ≥ $500,000 | ≥ $750,000 | $6,936 | $13,872 |

(Source: CMS 2026 Medicare Data via Income Lab and Madison Partners)

For example, if a married couple goes above $218,000 by $1, they may move into Tier 1 and may owe an added $2,297. That’s why many people use these brackets to size a conversion before picking the timing.

To estimate MAGI, add up items such as:

- wages

- self-employment income

- pensions

- annuities

- taxable Social Security

- interest

- dividends

- capital gains

- rental income

- traditional IRA or 401(k) distributions

- tax-exempt municipal bond interest, since IRMAA counts it

Next, place that amount in the lowest-income years you may have left.

How to calculate your safe Roth conversion amount

A simple formula and why you need a buffer

Use this formula:

Safe Conversion Amount = (Target IRMAA Threshold − Expected MAGI) − Safety Buffer

Start with your projected MAGI before the conversion. Subtract that number from the IRMAA threshold you want to stay under. What’s left may be your conversion room.

The point here may not be to convert the biggest amount possible. It may be to stay under the next IRMAA tier.

A buffer matters. A $2,000 to $5,000 buffer may give you some room for income that shows up late in the year. That extra income may come from:

- year-end mutual fund capital gains distributions

- dividend increases

- a pension COLA

- occasional consulting income

There’s another detail that trips people up: the standard deduction does not reduce MAGI for IRMAA purposes. You need to work from gross income before the deduction applies.

Your conversion limit may be the lower of your IRMAA room and your tax-bracket room. In practice, some people size the conversion so it stays below both the next IRMAA tier and their tax-bracket ceiling.

Once you know the safe amount, the next question may be when to use it.

Worked examples using current IRMAA brackets

Here’s what the math may look like in practice.

Example 1 - Married couple filing jointly: Margaret and Tom, both age 67, have a baseline MAGI of $102,000. The Tier 1 IRMAA threshold for married filers is $218,000. That leaves $116,000 of remaining conversion room. After a $6,000 buffer, they convert $110,000, which keeps them below the cliff and may avoid a potential $2,297 more per person in surcharges.

Example 2 - Single filer: A single filer with $95,000 of baseline MAGI has $14,000 of room before the $109,000 Tier 1 cliff. With a $2,000 buffer, the safe conversion amount is $12,000. Crossing that tier may add $1,148 per person.

If the safe amount feels too small for your goal, some people spread the conversion across low-income years.

When to convert: timing and spreading conversions across multiple years

If your safe conversion amount may be too small to handle in one year, it may make sense to shift the conversion into your lowest-income years. Avoiding IRMAA isn't always about converting less. In many cases, it's about converting at the right time. The same conversion may lead to very different Medicare premium results depending on the year you do it.

The best years to convert: before 63, after retirement, before Social Security and RMDs

The best window may be the gap between retirement and the start of Social Security and RMDs, when taxable income may be lower and conversion room may be at its widest.

Age 63 is the key cutoff. Income at 63 affects premiums at 65. Conversions done at 62 or earlier usually fall outside that lookback window. So the years right after retirement, but before 63, may offer the best opening for larger conversions.

Once RMDs begin, conversion room may shrink because mandatory distributions are added directly to MAGI. Converting earlier may reduce the IRA balance tied to future RMDs, which is the whole point.

Why smaller conversions over several years usually beat one large conversion

One large conversion may be tax-inefficient. It often pushes income into the 32%–37% tax brackets and may trigger the highest IRMAA tier in a single year. A 3- to 5-year plan may let you fill the 22% or 24% brackets each year and stay under a chosen IRMAA cliff. If one spouse may later file single, some households convert more while they still use joint IRMAA brackets, since single thresholds are much lower.

That tradeoff may help frame the choice between converting more now or spreading the amount across several lower-income years.

| Feature | One Large Conversion (e.g., $500,000) | Multi-Year Plan (e.g., $100,000/year for 5 years) |

|---|---|---|

| Current taxes | Higher; may reach 32%–37% brackets | Lower; often fits 22% or 24% brackets |

| IRMAA risk | Higher; may trigger top-tier IRMAA for one year | Lower; may be sized to stay below Tier 1 or 2 thresholds |

| Future RMD reduction | Immediate and maximum | Gradual but still highly effective |

| Social Security taxation | May make 85% of benefits taxable in conversion year | Spreads impact; may keep Social Security taxation lower over time |

With the timing window set, the next step is sizing the conversion against your own income and accounts.

Put the framework to work with your own accounts

A five-step process for sizing your conversion

Before you convert, map out your income for the year. Then use the threshold gap from the prior section to estimate how much room you may have for a conversion.

- Gather your year-to-date income from all sources: wages, pension payments, Social Security benefits, dividends, interest, realized capital gains, and any RMDs already taken.

- Project full-year MAGI based on that year-to-date income. Then add tax-exempt interest, such as municipal bond interest, since it counts toward IRMAA.

- Identify your next IRMAA threshold. Take the next IRMAA threshold from the prior section and subtract your projected MAGI. That difference may show your conversion room.

- Subtract a $2,000 to $5,000 buffer.

- Your estimated safe conversion amount may be whatever remains after the buffer.

Many people wait until October or November to lock in the amount, when year-end income may be easier to estimate.

Use Mezzi to check your conversion amount across all accounts

Once you know the range, pull data from every account before making a move. For a lot of people, that's the messy part. A 401(k) from a former employer, a brokerage account, a traditional IRA, and a Roth IRA may all sit at different firms.

Mezzi connects those accounts through read-only access via Plaid and Finicity. It pulls wages, dividends, IRA balances, and other income sources into one view. From there, it may help you estimate a conversion amount and timing, flag IRMAA risk based on projected MAGI, and review the full picture across connected accounts.

It only helps with estimates and review. You stay in control of the transaction.

Conclusion: The right conversion amount fits your tax bracket and IRMAA tier

At that point, the decision may come down to your tax bracket, IRMAA tier, and timing. Roth conversions may work best when they're sized to stay under both a tax-bracket target and the next IRMAA tier.

A common approach is to estimate baseline MAGI, find the gap to the next threshold, apply a buffer, and spread conversions across multiple lower-income years when that fits the situation. The idea is simple: move money toward tax-free growth without triggering a higher Medicare premium two years later.

FAQs

How do I estimate my IRMAA MAGI accurately?

Start with your baseline MAGI. That may include expected income from Social Security benefits, pension distributions, interest, dividends, capital gains, and rental income. Add tax-exempt interest too, because it counts toward IRMAA even though it isn’t taxed for regular income tax purposes.

Next, subtract your baseline MAGI from your target IRMAA threshold. What’s left is your available conversion room. In plain English, that’s the amount you may be able to convert without moving into the next Medicare premium surcharge tier.

What if my conversion pushes me over by $1?

Even $1 over an IRMAA threshold may trigger the full surcharge for that tier. IRMAA works more like a cliff than a gradual phase-in, so the added cost may be the same whether you go over by $1 or by a much larger amount.

Because the surcharge may apply for the full year of your Medicare Part B and Part D premiums, many experts suggest staying $2,000 to $5,000 below the threshold as a safety margin.

Should I convert before age 63 if I plan to retire early?

Yes. For many early retirees, converting before age 63 may be the best window.

Medicare uses a two-year lookback for IRMAA. That means income at age 62 or earlier may fall outside the window used for premiums that start at age 65. If someone waits until age 63, those conversions may affect Medicare premiums.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.