One SDIRA real estate mistake may make the full IRA taxable for that year.

If I were summarizing this topic in plain English, I’d put it like this: an SDIRA may own real estate, but the IRA has to do the buying, hold the title, pay the bills, collect the rent, and stay separate from me and my family. If I cross that line - by using the property, paying expenses myself, doing repair work, or backing the loan - I may trigger a prohibited transaction. And if debt is involved, part of the income or gain may be taxed under UBIT/UDFI, even in a Roth IRA.

Here’s the short version:

- The IRA owns the property, not me

- All income and expenses may need to flow through the IRA

- Personal use may not be allowed - even for one weekend

- Deals with disqualified people may be off-limits

- Loans generally may need to be non-recourse

- Debt-financed income may trigger Form 990-T and trust-rate tax

- RMDs may be harder with illiquid property in a pre-tax IRA

A few facts stand out:

- A prohibited transaction may disqualify the IRA as of January 1 of that year

- If I’m under 59½, a 10% early distribution penalty may also apply in some cases

- UBIT rules generally include a $1,000 specific deduction

- Independent property appraisals often run around $500 to $800

If I’m looking at SDIRA real estate, the main test may be simple: Who owns it, who pays, who benefits, and is there debt? That framework may catch most of the trouble before a deal closes.

Core IRS rules for SDIRA real estate ownership and cash flow

Title, custody, and document flow

The property must be titled in the IRA's name, not yours. A standard format looks like: "[Custodian Name] FBO [Your Name] IRA #[Account Number]." If your personal name appears on the deed, the property may be treated as yours rather than the IRA's.

That sounds like a small paperwork detail. It isn't. If the title, payment flow, or control setup is off, the deal may fail even if the property itself looks solid.

Your custodian signs the purchase contract, deed, and closing papers. You give direction through written instructions. With an IRA-owned LLC setup - where the IRA fully owns an LLC and you serve as its unpaid manager - the property may be titled in the LLC's name, and you may sign contracts and write checks directly.

It may also make sense to fund the IRA before making offers, so earnest money and closing costs may come from IRA cash.

Who pays expenses and who receives income

Once the title is set up the right way, the cash-flow rules tend to matter most. All income and all expenses must move through IRA funds.

That means property taxes, insurance premiums, HOA dues, repairs, utilities, and legal fees must be paid from IRA funds. Rent, sale proceeds, and insurance claim payments must go back to the IRA.

Do not pay expenses yourself, even for a short time, and do not do the work on the property yourself. Maintenance must be handled by unrelated third-party professionals and paid by the IRA.

Use this as a quick compliance check:

Table: Allowed vs. prohibited cash flows for IRA-owned real estate

| Transaction Type | Allowed (Must flow through IRA) | Prohibited (Personal interaction) |

|---|---|---|

| Purchase Deposit | Custodian wires 100% of funds from IRA account | Owner pays earnest money from personal checking |

| Roof Repair | IRA pays unrelated contractor via custodian or LLC check | Owner pays contractor personally and asks for reimbursement |

| Rental Income | Tenant sends rent check to Custodian FBO IRA | Owner receives rent and deposits it into a personal account |

| Property Taxes | Paid directly from IRA cash reserves | Owner pays taxes to be reimbursed later |

| Sale Proceeds | 100% of proceeds wired back to the IRA account | Any portion taken personally |

The IRA may also need enough cash on hand for vacancies, taxes, and repairs.

The next issue is who you cannot do business with at all.

Distributions and liquidity limits

Traditional SDIRAs follow the same RMD rules as other traditional IRAs, starting at age 73. Real estate may be allowed inside an IRA, but it may still create RMD pressure because it may be hard to sell on short notice.

If the IRA does not have enough cash for an RMD, an in-kind distribution of a property interest may be needed. In that case, the custodian re-titles a fractional interest - say, 5% - from the IRA to you personally, and the appraised value counts toward part of the RMD. That approach may work, but it usually takes planning and appraisal fees. Independent appraisals typically run $500 to $800 per property.

Roth SDIRAs avoid this issue during the original owner's lifetime because they do not have RMD requirements in that period.

These mechanics matter even more once personal use, related parties, or financing enter the picture - the next section covers the transactions that may break the IRA rules.

Top 10 Costly MISTAKES People Make With a Self-Directed IRA

Prohibited transactions and disqualified persons

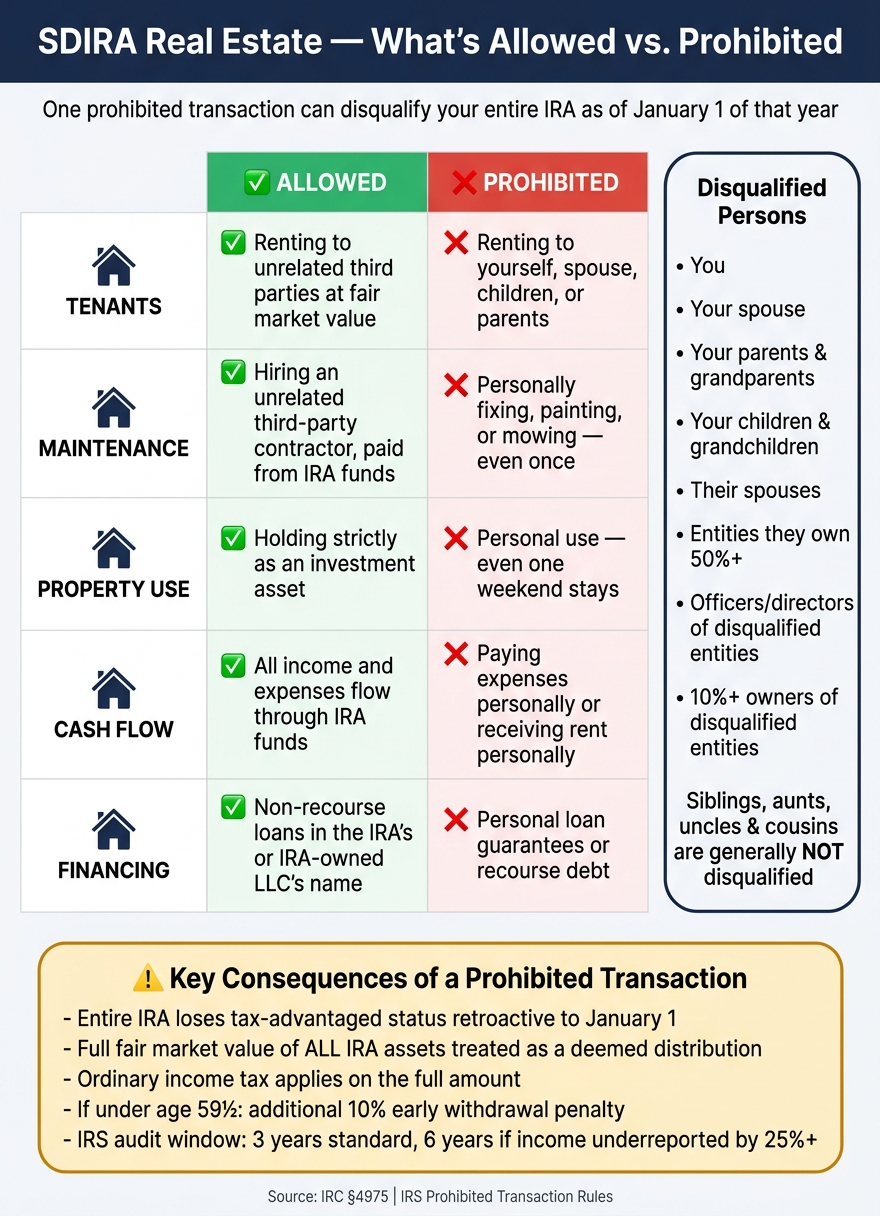

SDIRA Real Estate: Allowed vs. Prohibited Transactions at a Glance

Who counts as a disqualified person

The IRS sets a narrow group of people and entities that your IRA may not transact with. That group includes you, your spouse, your parents and grandparents, your children and grandchildren, and each of their spouses. It also includes any entity they control. If they own 50% or more of an entity, that entity is also treated as disqualified.

Siblings, aunts, uncles, and cousins generally do not fall into that group.

The IRS list also covers fiduciaries, plus any officer, director, or 10%-plus owner of a disqualified entity.

Real estate mistakes that trigger prohibited transactions

With SDIRA real estate, the line may be stricter than many people expect.

If your IRA owns a rental property and you fix a broken faucet yourself, the IRS may treat that as a prohibited transaction. Why? Your labor may be viewed as a service provided to the IRA.

Personal use may create the same issue. Even one weekend in the property may count as a prohibited transaction. The same may apply if the property is rented to your adult child or if your IRA buys the property from your parents. Disqualified persons may not buy from, sell to, or lease property to the IRA, even at fair market value.

Table: Allowed vs. prohibited uses of SDIRA real estate

| Category | Allowed | Prohibited |

|---|---|---|

| Tenants | Renting to unrelated third parties at fair market value | Renting to yourself, your children, parents, or spouse |

| Maintenance | Hiring an unrelated third-party plumber or contractor | Personally fixing a leaky faucet, painting, or mowing the lawn |

| Property Use | Holding the property strictly as an investment | Staying in the property for a weekend or using it as a personal office |

| Management | Hiring a property manager or making high-level decisions without compensation | Paying yourself for management |

The Peek v. Commissioner case shows how far these rules may reach. In that case, the U.S. Tax Court found that personal loan guarantees may trigger a prohibited transaction and may disqualify the IRA.

These rules may do more than create paperwork trouble. They may cause the account to lose its tax treatment.

What happens when the IRS finds a rule violation

One mistake may turn an ordinary rental property inside an IRA into a full-account tax issue. A single prohibited transaction may cause the entire IRA to lose its tax-advantaged status, effective January 1 of that year. If the IRS determines that a prohibited transaction occurred, it may treat the full fair market value of every asset in the IRA as a deemed distribution.

That amount may be subject to ordinary income tax. If you're under 59½, an added 10% early withdrawal penalty may apply on top of that.

The IRS generally may have three years to assert a violation, or six years if unreported income exceeds 25%. In cases involving fraud, there may be no time limit.

Debt-financed real estate may also bring UBIT and UDFI risk.

Financing, non-recourse loans, and when UBIT or UDFI applies

What non-recourse financing means inside an IRA

An IRA may buy real estate with borrowed money, but the loan must be non-recourse. The borrower needs to be the IRA or an IRA-owned LLC, not you personally. If the deal goes south, the lender’s remedy may be limited to taking the property. They may not pursue you or the IRA for a deficiency judgment.

You also may not personally guarantee the debt. Under IRC §4975, a personal guarantee is treated as an extension of credit between a disqualified person and the IRA, which may trigger a prohibited transaction. That includes any side agreement that makes you personally liable.

Loan documents also need to match the IRA or IRA-owned LLC name used on title.

That structure may keep you out of personal liability. But once debt enters the picture, a different tax rule set may apply to the financed share of the property.

How debt creates UDFI under UBIT

Once debt is involved, the tax issue shifts from ownership to leverage.

When an IRA uses debt, the debt-financed share of rent or gain may be treated as UDFI and taxed under UBIT rules. This may apply to both traditional and Roth IRAs. A Roth IRA’s tax-free status may not shield debt-financed income.

The taxable share is figured with a debt percentage:

- Divide the average outstanding loan balance by the property’s average adjusted basis for the year.

- Apply that percentage to net income after deductions.

The IRS allows a $1,000 specific deduction against unrelated business taxable income before tax may apply. If gross unrelated business income exceeds $1,000 for the year, the IRA custodian generally must file Form 990-T and pay the tax from IRA funds, usually by April 15 of the following year.

UBIT is taxed at trust rates, which may reach 37%.

Comparing all-cash, leveraged, and partnered deals

The main choice may not be just whether to borrow. It may be whether the after-tax return still makes sense once UDFI, filing work, and deal structure are part of the picture.

Co-owning with unrelated investors requires strict pro-rata treatment of income and expenses. Disqualified persons still remain off-limits.

Table: All-cash vs. non-recourse financing vs. partnering in an SDIRA

| Feature | All-Cash Purchase | Non-Recourse Financing | Partnering (with unrelated co-investors) |

|---|---|---|---|

| Risk | Low (no debt) | Moderate (leverage risk) | Moderate (partnership disputes) |

| Liquidity | Low (capital tied up) | Moderate (less initial cash) | High (pooled resources) |

| UBIT/UDFI Exposure | None | High (on debt-financed portion) | Variable (depends on whether debt is used) |

| Admin Complexity | Low | High (990-T filings, reserves) | Moderate (LLC/partnership docs) |

An all-cash purchase may avoid UDFI entirely, but it may also leave more IRA capital tied up in one illiquid asset. Leverage may expand purchasing power, though the after-tax math may still need to pencil out.

Compliance checklist and how Mezzi helps you pressure-test the decision

Expense handling, third-party services, and recordkeeping

With SDIRA real estate, all property cash flow must move through the IRA. You also may not do the work yourself or take compensation from the IRA. Personal services may count as a prohibited benefit to a disqualified person.

That usually means:

- All expenses - property taxes, insurance, repairs, and management fees - must be paid from IRA funds

- Every service provider must be an unrelated third party; keep their invoices on file

- No personal use of the property, ever

It may also make sense to keep an annual independent valuation for Form 5498 and pay that fee from IRA funds. Many investors also keep a cash cushion for taxes, insurance, repairs, and vacancies.

Once those rules are clear, the next step may be testing whether the deal fits your portfolio and liquidity needs.

Using Mezzi to evaluate SDIRA real estate across your full portfolio

Portfolio-level context may help you test whether the IRA may support the property without adding too much concentration or cash-flow strain. Mezzi aggregates connected accounts on a read-only basis, so you may see liquidity, concentration, and account mix before committing IRA cash.

Mezzi's X-Ray feature may surface hidden real estate concentration across REITs, private holdings, and direct property exposure in each connected account. Mezzi may also model liquidity, concentration, and tax drag before you buy.

Table: How Mezzi features apply to SDIRA real estate

| Feature | What it analyzes | How it helps the investor decide |

|---|---|---|

| Read-only aggregation | IRAs, 401(k)s, taxable accounts, and cash | Assesses total liquidity and ability to fund IRA property expenses |

| X-Ray overlap analysis | REITs, private holdings, and direct property | Identifies hidden real estate concentration across the full portfolio |

| Concentration risk | Asset allocation across all account types | Determines if adding a direct property creates excessive real estate exposure |

| Tax modeling | Account type and leverage structure | Evaluates tax drag on leveraged real estate income |

Conclusion: The rules that matter most before you buy

SDIRA real estate may be a legitimate strategy for building tax-advantaged wealth through property. But the compliance requirements are strict, and the consequences of errors may be severe.

If the property passes the checklist, the final question may be whether the after-tax return still works. Some investors treat compliance, liquidity, and leverage as part of the buy decision from day one.

FAQs

Can my SDIRA buy a property I already own?

No. Your self-directed IRA may not buy a property you already own.

Under Internal Revenue Code Section 4975, that would be self-dealing and a prohibited transaction.

The IRS bars direct or indirect sales, exchanges, or leases between an IRA and a disqualified person. That group includes you, your spouse, your ancestors, and your lineal descendants. If this happens, your entire IRA may be disqualified and may trigger major tax penalties.

What counts as personal use of IRA-owned real estate?

Personal use may occur when the account holder or a disqualified person - such as a spouse, parent, child, grandparent, or grandchild - gets any direct or indirect benefit from IRA-owned real estate.

That may include living there, using it as a vacation home, storing personal belongings there, doing repairs or maintenance yourself, or getting side benefits like discounts or special access.

How is UBIT calculated on a leveraged SDIRA property?

Calculate UDFI by finding the debt-financed percentage: average acquisition indebtedness divided by average adjusted basis for the tax year. Then apply that ratio to the property’s net income after deductible expenses like mortgage interest, property taxes, insurance, management fees, and depreciation.

If taxable income exceeds $1,000, the IRA may need to file Form 990-T and may owe tax at compressed trust tax rates. The same approach may also apply to capital gains on sale.Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.