If you're over 70½ and have Required Minimum Distributions (RMDs) from your IRA, using a Qualified Charitable Distribution (QCD) might be a smart move. A QCD lets you donate directly to a charity from your IRA, satisfying your RMD and keeping that income off your tax return. This can help reduce your taxable income, lower your Medicare premiums, and even decrease taxes on Social Security benefits.

Here’s what you need to know:

- QCD Basics: You can donate up to $111,000 annually (or $222,000 for couples) directly from your IRA to a qualified charity.

- Tax Advantage: The donated amount is excluded from your Adjusted Gross Income (AGI), avoiding taxes on RMDs.

- Eligibility: Must be 70½ or older, and donations must go directly to eligible 501(c)(3) charities (not donor-advised funds or private foundations).

- Key Rules: Ensure the QCD is processed before taking any personal RMD withdrawals to maintain its tax-free status.

With new 2026 tax rules limiting itemized deductions, QCDs are an effective way to lower your tax burden while supporting causes you care about. For those with significant IRA balances, they also help manage future RMDs by reducing the account size early. Always consult a tax professional to ensure compliance with IRS rules.

QCDs: The Tax-Smart Way to Give in Retirement (2025 Qualified Charitable Distributions Guide)

Tax Benefits of Using QCDs to Satisfy RMDs

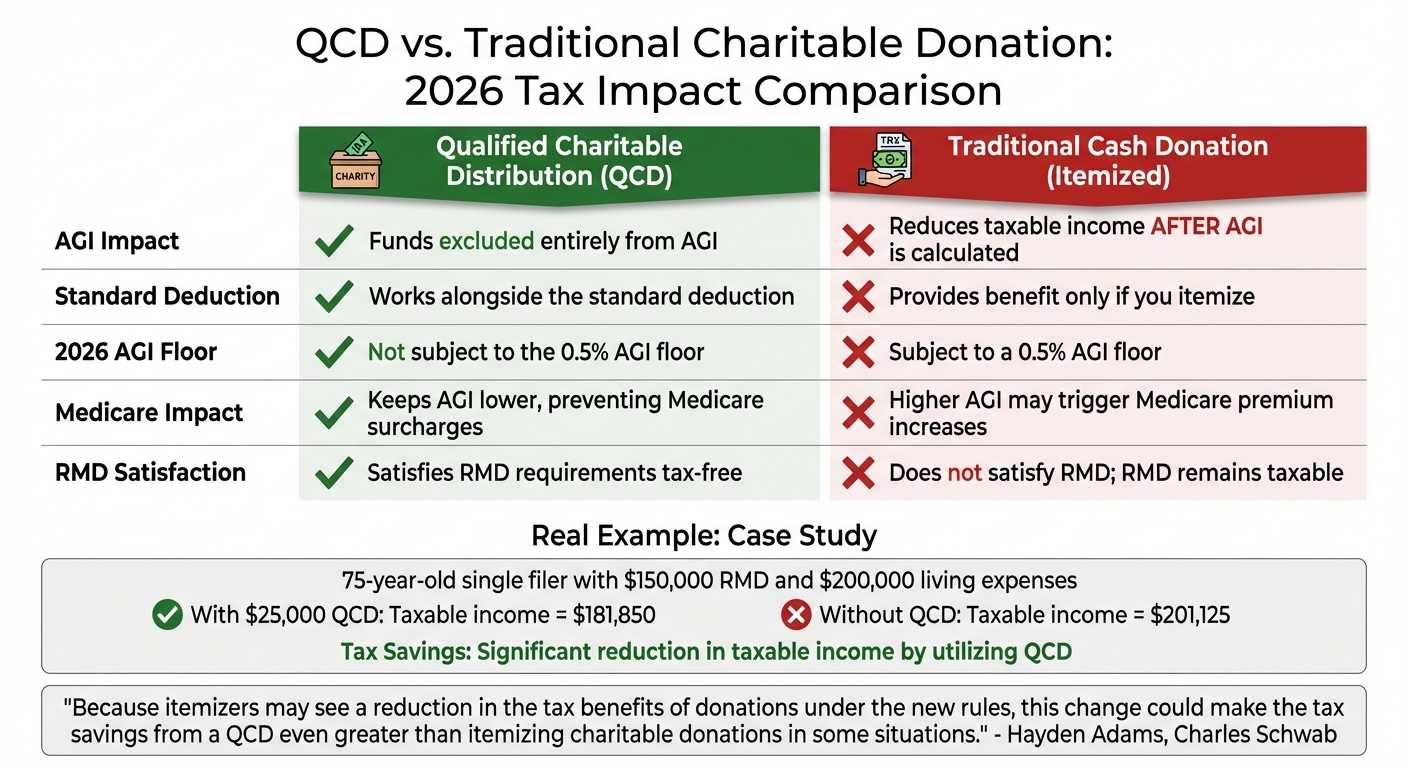

QCD vs Traditional Charitable Donation Tax Comparison 2026

Qualified Charitable Distributions (QCDs) can provide meaningful tax advantages by helping to reduce taxable income in a way that traditional methods can't match.

How QCDs Reduce Taxable Income

A QCD acts as an "above-the-line" income exclusion, meaning it never appears on your tax return. In contrast, Required Minimum Distributions (RMDs) are fully taxable as ordinary income. When you make a QCD, the funds go directly to a qualified charity, keeping them out of your Adjusted Gross Income (AGI).

Why does this matter? Your AGI doesn’t just determine your tax bracket - it also impacts how much of your Social Security benefits are taxable, your Medicare premiums, and your eligibility for certain credits and deductions. By keeping your AGI lower, you can potentially avoid higher taxes and Medicare surcharges.

"A QCD is one of the only ways to satisfy your Required Minimum Distribution (RMD) without increasing your taxable income." - Andrew Matz, Financial Planner, Oak Road Wealth Management

For individuals in higher tax brackets, the benefits can be even more pronounced. For instance, if you’re in the 35% marginal tax bracket, excluding $10,000 from your income through a QCD could save you about $3,500 in federal taxes.

This tax efficiency becomes even more compelling when you compare QCDs to more traditional forms of charitable giving.

QCDs vs. Traditional Charitable Giving

The 2026 tax updates have introduced new challenges for traditional charitable contributions, making QCDs a more attractive option. Under the One Big Beautiful Bill Act (OBBBA), itemized charitable deductions now face a 0.5% AGI floor and a maximum tax benefit of 35 cents on the dollar for high-income earners. QCDs, however, avoid these limitations entirely.

Take this example from Charles Schwab’s January 2026 analysis: A 75-year-old single filer needed $200,000 for living expenses and had a $150,000 RMD. By using a $25,000 QCD instead of taking the full RMD and then making a cash donation, the filer reduced their taxable income from $201,125 to $181,850. This approach also took advantage of the 2026 standard deduction of $18,150 and avoided the 0.5% AGI floor that would have applied to an itemized donation.

Here’s a quick comparison of QCDs and traditional cash donations:

| Feature | Qualified Charitable Distribution (QCD) | Traditional Cash Donation (Itemized) |

|---|---|---|

| AGI Impact | Funds excluded entirely from AGI | Reduces taxable income after AGI is calculated |

| Standard Deduction | Works alongside the standard deduction | Provides a benefit only if you itemize |

| 2026 AGI Floor | Not subject to the 0.5% AGI floor | Subject to a 0.5% AGI floor |

| Medicare Impact | Keeps AGI lower, preventing Medicare surcharges | Higher AGI may trigger Medicare premium increases |

| RMD Satisfaction | Satisfies RMD requirements tax-free | Does not satisfy RMD; RMD remains taxable |

"Because itemizers may see a reduction in the tax benefits of donations under the new rules, this change could make the tax savings from a QCD even greater than itemizing charitable donations in some situations." - Hayden Adams, Director of Tax and Financial Planning, Charles Schwab

In short, QCDs offer a way to lower your taxable income whether you itemize or take the standard deduction. They sidestep new deduction floors and reduce your income before other calculations, making them a powerful tool for those navigating the 2026 tax rules, especially high-net-worth individuals.

Eligibility Rules and Restrictions for QCDs

Before using Qualified Charitable Distributions (QCDs) to meet your Required Minimum Distribution (RMD) and lower your taxable income, it's important to understand the IRS rules for eligibility. These rules cover who qualifies, which accounts can be used, and the types of charities that are eligible.

Who Qualifies for QCDs?

To qualify for a QCD, you must be at least 70½ years old on the day your IRA custodian processes the distribution. If the request is made even one day before you reach this age, the distribution will be considered taxable.

The following accounts are eligible for QCDs:

- Traditional IRAs

- Inherited IRAs

- SEP or SIMPLE IRAs, but only if no employer contributions are made during the calendar year

However, QCDs cannot be made directly from 401(k)s, 403(b)s, or Thrift Savings Plans. If you want to use funds from these accounts for a QCD, you'll need to roll them into an IRA first.

"The 'direct transfer' detail is what separates a QCD from taking a withdrawal and then writing a personal check, and it's the reason the tax treatment is completely different." – Taylor R. Schulte, CFP, Define Financial

For a distribution to qualify as a QCD, it must be sent directly from your IRA custodian to the charity. If the check is made payable to you and you later forward it to the charity, the amount will count as taxable income. To avoid this, ensure the custodian makes the check payable directly to the charitable organization.

Finally, make sure to review the annual limits and confirm that the charity meets IRS requirements before proceeding.

Annual Limits and Eligible Charities

As of 2026, you can exclude up to $111,000 per person annually through QCDs. If you're married, and both you and your spouse are 70½ or older with separate IRAs, each of you can make QCDs up to this limit, allowing for a combined total of $222,000. This limit will adjust annually to account for inflation.

To qualify for a QCD, the charity must be a 501(c)(3) organization that is eligible to receive tax-deductible contributions. Examples include churches, food banks, educational institutions, and many community nonprofits. To confirm eligibility, use the IRS tool to verify the organization's 501(c)(3) status before initiating your distribution.

Keep in mind that QCDs cannot be made to donor-advised funds, private foundations, or supporting organizations. Contributions to these entities will not qualify as tax-free distributions. Additionally, if you have made any tax-deductible contributions to your traditional IRA after the age of 70½, those contributions will reduce the amount of QCDs you can exclude from taxable income until they are fully accounted for.

"Any post-2019 deductible contributions made to your IRAs when you were 70½ or older will reduce your allowable tax-free QCD amount until they are used up." – Joy Taylor, Editor, The Kiplinger Tax Letter

How to Execute QCDs

If you're eligible, following the right steps can help you execute a Qualified Charitable Distribution (QCD) that satisfies your Required Minimum Distribution (RMD) while also lowering your taxable income.

Step-by-Step QCD Process

To carry out a QCD, you’ll need to coordinate with both your IRA custodian and the charity. First, confirm that you are at least 70½ years old on the date the QCD is processed. If processed earlier, the distribution will be taxable.

Next, verify that the charity qualifies as a 501(c)(3) organization using the IRS’s verification tool. Keep in mind that donor-advised funds, private foundations, and supporting organizations do not meet the requirements for QCDs. After confirming eligibility, contact your IRA custodian to arrange for a direct transfer to the charity. The check must be made payable directly to the charitable organization. Depending on your custodian, the check may either be mailed directly to the charity or sent to you for delivery - but the payee must remain the charity.

"To have the RMD excluded from income via a QCD, the QCD must happen before you take any RMD money into your own hands." – Daniel Leonard, CFP and Owner, Powering Your Retirement

Timing matters. The IRS considers the first funds withdrawn from your IRA as part of your RMD, so it’s critical to complete your QCD before taking any personal distributions. Many financial advisors suggest making QCDs early in the year - "January is the new December" - to avoid complications with automatic RMD withdrawals. Remember, all QCDs must be finalized by December 31 to count for that tax year. Following these steps ensures your QCD meets IRS requirements while aligning with your tax planning goals.

Timing and Documentation Requirements

Processing times for QCDs vary by custodian, so it’s a good idea to allow several weeks for the request to be completed, especially as the year-end deadline approaches. If your QCD requires liquidating investments, factor in about three business days for settlement.

Once the transfer is complete, request a written acknowledgment from the charity. For donations of $250 or more, this receipt should include the amount, date, and a statement confirming that no goods or services were received in return. Your IRA custodian will report the distribution on Form 1099-R, using distribution code "Y" in Box 7. When filing taxes, report the total distribution on line 4a and the taxable amount (usually $0) on line 4b of Form 1040. Be sure to keep your IRA statement showing the distribution, along with the charity's acknowledgment letter, as part of your tax records.

Other Benefits of Using QCDs

Impact on Medicare Premiums and Social Security Taxation

QCDs don't just lower your taxable income - they also help you avoid additional tax-related expenses. Unlike charitable deductions that only affect taxable income after your AGI is calculated, QCDs directly reduce your AGI. This can have a significant impact on costs tied to Medicare premiums and Social Security taxation.

For Medicare, Part B and Part D premiums include IRMAA (Income-Related Monthly Adjustment Amount) surcharges, which kick in when your MAGI crosses certain thresholds. Even a small income increase can trigger these surcharges. For example, in 2026, a retired couple with a MAGI of $226,000 would have faced a $974.40 IRMAA surcharge. By making a $10,000 QCD from their IRA, they reduced their MAGI to $216,000, avoiding the surcharge. This also saved them $2,200 in federal income tax (at the 22% bracket) and about $500 in state taxes.

QCDs also play a role in reducing the taxable portion of Social Security benefits. Up to 85% of these benefits can be taxed, depending on your combined income (AGI, tax-exempt interest, and half of your Social Security benefits). For instance, in January 2026, a Maryland couple used a $6,000 QCD to bring their AGI down to $149,000. This move helped them fall below the $150,000 threshold, restoring a $12,000 federal enhanced senior deduction and a $1,750 Maryland senior tax credit. Altogether, this provided $3,897 in total tax relief, effectively making their $6,000 donation cost just $2,103.

"This one simple shift in giving strategy, from the checkbook to the IRA, save my clients more money than any complex investment maneuver."

– Michael Ryan, Retired Financial Planner, Michael Ryan Money

These examples highlight how QCDs can be a powerful tool for reducing tax burdens while supporting charitable causes.

Combining Charitable Giving with Financial Planning

QCDs not only reduce AGI but also serve as a strategic component of long-term financial planning. They allow you to align your charitable contributions with tax-efficient strategies. Starting at age 70½ - before RMDs are required - you can use QCDs to proactively lower your IRA balance, helping to avoid "RMD creep", where increasing IRA balances push you into higher tax brackets over time.

For 2026, individuals can exclude up to $111,000 through QCDs, and married couples where both spouses are at least 70½ can combine for a $222,000 exclusion. By gradually reducing the balance of tax-deferred IRAs, you can also lower the size of your taxable estate. Additionally, SECURE 2.0 allows a one-time QCD of up to $55,000 to fund life-income vehicles, such as Charitable Remainder Trusts (CRTs) or Charitable Gift Annuities (CGAs). These tools provide a lifetime income stream while ensuring that the remainder benefits your chosen charity.

"At Oak Road Wealth Management, we view the QCD not just as a 'gift,' but as a strategic income-management tool."

– Andrew Matz, Financial Planner, Oak Road Wealth Management

Limitations and Considerations

Limits on Excess Contributions

QCD exclusions come with annual caps, and any amount exceeding your RMD for the year won't qualify for tax-free treatment. These excess amounts also can't be carried forward to future years.

The IRS uses the "first dollars out" rule, meaning the first IRA withdrawals in a calendar year are automatically counted as RMDs. To ensure your QCDs are non-taxable, you need to complete them before taking any personal distributions.

"To have the RMD excluded from income via a QCD, the QCD must happen before you take any RMD money into your own hands. If you take your RMD first and then do a QCD later, you can't retroactively fix it."

– Daniel Leonard, CFP, Owner, Powering Your Retirement

Because of this, early-year planning is key. Processing your QCD in January or early February ensures it counts toward your RMD before any other withdrawals. If you exceed the QCD limit, the excess is treated as a standard charitable contribution, subject to itemization rules under the 2026 tax laws.

Now, let's look at which accounts and types of charities qualify for a QCD.

Eligible Accounts and Organizations

Certain accounts and charities meet the criteria for QCDs. These distributions can only come from IRAs, such as Traditional, Rollover, Inherited, or inactive SEP and SIMPLE IRAs. They cannot originate from employer-sponsored plans like 401(k)s, 403(b)s, 457(b)s, or Thrift Savings Plans (TSPs). If you're looking to use funds from those plans for a QCD, you'll need to roll them over into an IRA first.

For SEP and SIMPLE IRAs, the account must be inactive. This means no employer contributions can be made during the same tax year. If any employer contributions are added, the account becomes ineligible for QCDs.

QCDs also have restrictions on eligible organizations. They cannot go to donor-advised funds (DAFs), private foundations, or supporting organizations. The donation must be sent directly to a qualified 501(c)(3) organization that is eligible to receive tax-deductible contributions. To confirm a charity's eligibility, use the IRS Tax Exempt Organization Search tool before making your QCD. Additionally, if you receive any personal benefit, such as tickets to an event or meals, the distribution will not qualify as a QCD.

Conclusion: Are QCDs Right for You?

Qualified Charitable Distributions (QCDs) can be a smart choice when your financial goals align with your charitable giving plans. If you're 70½ or older, have Required Minimum Distributions (RMDs), and regularly support charities, a QCD allows you to meet your RMD while keeping that income off your tax return. This approach is especially helpful if you claim the standard deduction, where traditional cash donations don’t offer tax benefits, or if you’re looking to avoid Medicare IRMAA surcharges or reduce taxes on your Social Security benefits.

Looking ahead to 2026, QCDs may become even more appealing. The One Big Beautiful Bill Act introduces new limits on itemized charitable deductions, including a 0.5% AGI floor and a 35% deduction cap. QCDs sidestep these restrictions entirely. Consider this example: A married couple in Maryland used a $6,000 QCD in early 2025, lowering their AGI from $155,000 to $149,000. This move saved them $3,897 in taxes, effectively reducing the net cost of their donation to $2,103. Examples like these highlight how QCDs can fit seamlessly into a well-rounded financial plan.

To maximize the benefits of QCDs, ensure your IRA custodian directly transfers the funds to a qualified 501(c)(3) charity. This step is crucial to meet IRS requirements. Also, confirm that the charity isn’t a donor-advised fund or private foundation. With the IRS's annual limit on QCDs, this strategy offers flexibility for those committed to charitable giving.

For a more tailored approach, Mezzi can help you integrate QCDs into your financial strategy. By connecting your accounts - IRAs, 401(k)s, and taxable accounts - Mezzi provides insights into how a QCD can lower your AGI, reduce taxes, and even impact Medicare premiums. You’ll also get guidance on timing, eligible charities, and coordinating QCDs with other tax strategies, all without the traditional advisor fees.

Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Always consult a qualified tax professional or financial advisor before making decisions about QCDs and RMDs.

FAQs

Can I do a QCD from my 401(k)?

No, you can’t make Qualified Charitable Distributions (QCDs) directly from a 401(k). They are only permitted from traditional IRAs or similar tax-deferred IRA accounts. If you’re interested in using a QCD, you’d first need to roll over funds from your 401(k) into a traditional IRA. Keep in mind, this process is subject to eligibility requirements and potential tax implications.

Will a QCD lower my Medicare IRMAA premiums?

Yes, a Qualified Charitable Distribution (QCD) can help reduce your Medicare IRMAA (Income-Related Monthly Adjustment Amount) premiums by lowering your taxable income. Here's how it works: By using a QCD to satisfy your Required Minimum Distribution (RMD), you can reduce the amount of income reported on your tax return. This, in turn, may help you stay below certain income thresholds that determine Medicare premiums.

By keeping your taxable income in check, you could avoid moving into a higher income bracket, which would otherwise result in increased Medicare costs. Essentially, a QCD serves a dual purpose - it allows you to fulfill your RMD obligations while potentially saving on Medicare expenses tied to income levels.

What if I already took part of my RMD this year?

If you've already taken part of your Required Minimum Distribution (RMD) this year, there's no way to reverse or reclassify that distribution. However, you still have the option to use a Qualified Charitable Distribution (QCD) to satisfy the rest of your RMD requirement. This approach could also lower your taxable income while allowing you to contribute to a charitable organization.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- Tax laws and IRS rules are subject to change. Readers should consult a qualified tax professional or financial advisor before making decisions about QCDs and RMDs.

- Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.