Net worth is the value of what you own minus what you owe. It’s a simple formula: Total Assets – Total Liabilities. Surprisingly, many people calculate it incorrectly, which can lead to poor financial decisions. Here’s what to include, what to leave out, and common mistakes to avoid:

Key Points:

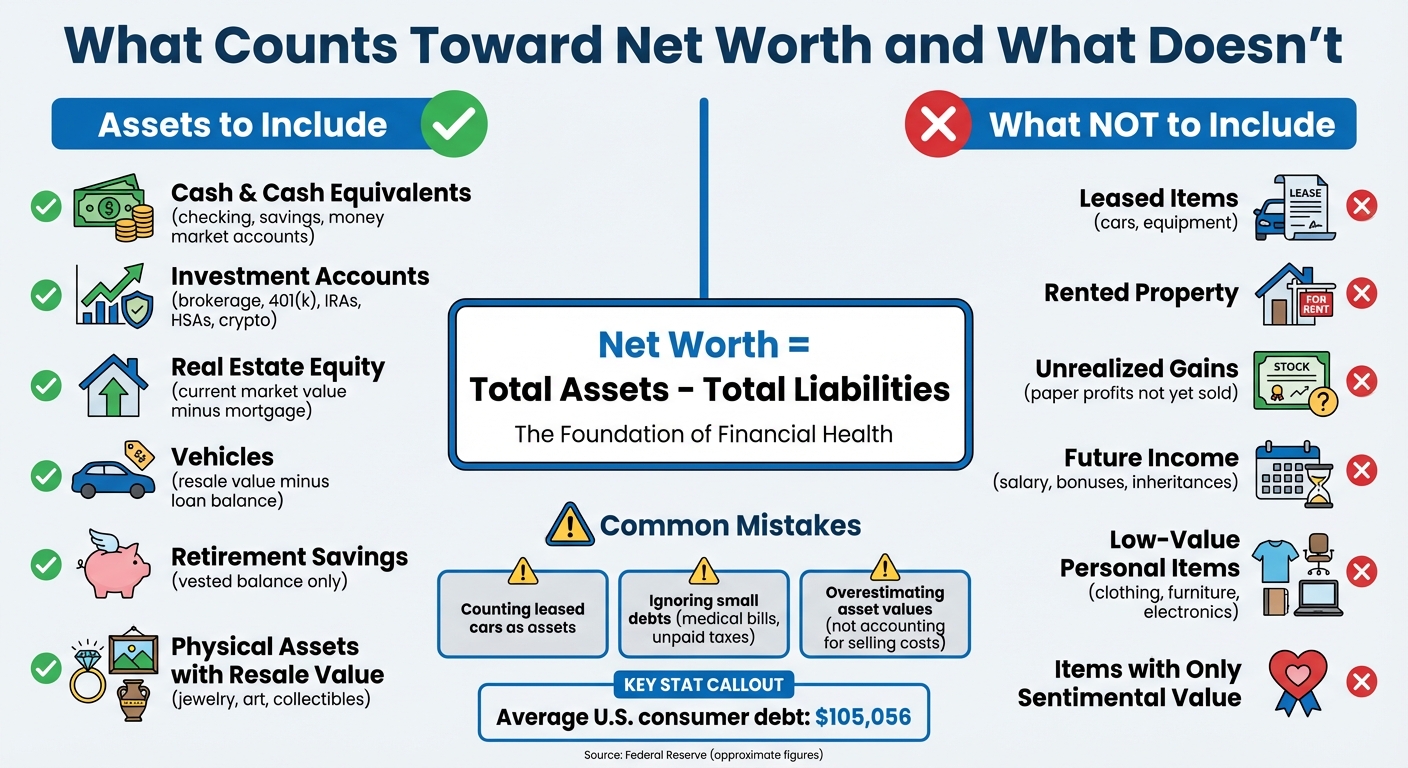

- Include in Net Worth: Cash, investments, real estate equity, retirement accounts, and physical assets like cars (minus loans).

- Exclude from Net Worth: Leased items, unrealized gains, personal items with low resale value, and future income.

-

Common Mistakes:

- Counting leased cars or rented items as assets.

- Ignoring smaller debts like unpaid taxes or medical bills.

- Overestimating asset values by not accounting for selling costs or taxes.

Tracking your net worth accurately may help you make more informed financial decisions. Avoid these errors, and focus on the current market value of what you own and owe for a clear financial picture.

What to Include and Exclude When Calculating Net Worth

Net Worth Statements: Over 50% of People Get This Wrong

Common Mistakes That Skew Net Worth Calculations

Even those who are financially savvy can make errors when calculating their net worth. These missteps might inflate your assets - or worse, obscure financial trouble. To track net worth accurately, it is important to properly identify and categorize both assets and liabilities. Here are some common pitfalls, starting with how leased items are often mistakenly classified as assets.

Counting Leased Items as Assets

If you don’t own it, it’s not an asset. A common mistake is listing leased cars, rented equipment, or other leased items as assets. The reality? The leasing company owns these items, not you. Since you cannot sell a leased car or equipment to pay off debt or convert it to cash, they don’t count as part of your net worth.

Unlike a financed car, which builds equity as you pay it off, a leased car holds no resale value for you. When the lease ends, the item is returned, leaving you with no equity.

R.J. Weiss, a Certified Financial Planner, puts it simply:

"The mistake I often see is adding assets that aren't things you're actually going to sell."

Treating Unrealized Gains as Liquid Assets

An increase in the value of your home or stock portfolio might feel like a financial boost, but until you sell, those gains are only "on paper." Unrealized gains represent potential value - not cash in hand. Treating them as liquid assets can lead to a false sense of wealth, potentially encouraging overspending or risky financial decisions.

It’s also important to remember that selling assets often comes with costs. Real estate commissions, transfer taxes, and other expenses can significantly reduce the actual cash you receive.

To avoid overestimating, you may wish to calculate a separate liquid net worth. This measure includes only cash and assets that can be quickly converted to cash, minus estimated selling costs and taxes.

Forgetting to Include Certain Liabilities

Big debts like mortgages and car loans are hard to forget, but smaller liabilities often go unnoticed. Unpaid medical bills, outstanding tax debts, or informal loans from friends and family can add up, reducing your actual net worth. Overlooking these liabilities can distort your financial picture and impact your financial planning.

Hector Castaneda, a CPA, highlights this point:

"Your anticipated income in the future is not a current asset unless it is already earned."

The same logic applies to liabilities: if you owe it now, it should be included in your calculations. Ignoring these obligations not only skews your net worth but can also lead to poor financial decisions.

| What People Forget | Why It Matters |

|---|---|

| Unpaid taxes | These can accrue penalties and interest, increasing your debt. |

| Medical bills | If sent to collections, they can harm your credit and financial standing. |

| Private loans from family/friends | These are liabilities, even without formal agreements. |

| Remaining lease payments | Future obligations reduce cash flow and should be factored in. |

To maintain an accurate picture of your finances, update all liabilities regularly - no matter how small they seem. This ensures your net worth reflects your true financial situation.

Assets That Should Be Included in Net Worth

When calculating your net worth, focus on assets you actually own and value them based on today's market prices. As Robert R. Johnson, Professor of Finance at Creighton University, explains:

A person's net worth statement is that both assets and liabilities are priced at market value.

Cash and Cash Equivalents

Start with cash and liquid assets - things that can be quickly converted to cash. This category includes physical cash, checking and savings accounts (including high-yield savings), money market accounts and funds, certificates of deposit (CDs), and the cash surrender value of whole life insurance policies.

Value these items based on the balance on a specific day each month, such as payday, to account for regular income and expenses. Experts suggest keeping an emergency fund of 3–6 months' worth of expenses in liquid, interest-earning accounts.

Always use current market values when assessing these assets.

Investment Accounts and Retirement Savings

Include all investment and retirement accounts, such as brokerage accounts, 401(k)s, IRAs, HSAs, and even cryptocurrencies. Make sure to value them at their current market price. For employer-sponsored retirement plans, only count the vested balance - this is the portion of the account that you have full ownership of, including your contributions and any employer matches you've earned.

To ensure accuracy, check your investment portals for the most recent balances or closing prices. For pensions or Social Security, you can estimate their lump-sum value by multiplying the expected monthly payment by 240 (assuming 20 years of retirement). This approach offers a clearer picture of your financial standing.

Next, consider physical property to round out your net worth calculation.

Real Estate Equity and Other Physical Assets

Physical assets should also be valued using current market prices. For real estate, calculate your equity by subtracting the outstanding mortgage balance from the property's current market value. Websites like Zillow can provide a rough estimate of your home's value. Similarly, for vehicles, use tools like Kelley Blue Book to determine resale value, then subtract any remaining loan balance.

For items like jewelry, art, and collectibles, estimate their current resale value - not the original purchase price. Johnson provides a clear example with cars:

When you purchase an automobile for $70,000, that automobile depreciates in value. When calculating net worth, the current market value of the automobile would be included, less the amount one owes on the loan for that automobile.

Using conservative estimates may help you avoid inflating your net worth. Items without any resale value should be excluded.

| Asset Category | How to Value It | What to Subtract |

|---|---|---|

| Real Estate | Current market value | Mortgage balance, home equity loans |

| Vehicles | Current resale value | Auto loan balance |

| Jewelry & Art | Estimated resale value | None (typically) |

| Investment Accounts | Current market price | None |

| Retirement Plans | Total vested balance | None |

Liabilities That Reduce Your Net Worth

Liabilities are the total of all debts and financial obligations you currently owe. When calculating your net worth, it's crucial to include the full outstanding debt balance - not just the monthly payment amounts. Overlooking this can give you an overly optimistic view of your financial situation.

Current Debts and Loans

Start by listing all your debts, both secured and unsecured. Secured debts, like mortgages, home equity lines of credit (HELOCs), and auto loans, are tied to collateral. On the other hand, unsecured debts include credit card balances, personal loans, student loans (federal and private), and retail store cards. To put things into perspective, the average U.S. consumer carries a total debt of $105,056, spread across these categories.

"Net worth is a reflection of the financial decisions that you have made. You can see if you are investing if your assets are growing, or if your net worth is declining because you're spending too much."

- Alissa Todd, Wealth Advisor, The Wealth Consulting Group

Debt not only reduces your net worth but also limits your ability to grow wealth by diverting money you could otherwise invest. High-interest debts, like credit card balances, can have a significant impact, so reducing these may help support your financial health.

But debts aren’t the only liabilities that can weigh on your net worth. Other financial obligations can also have a significant impact.

Pending Obligations and Contingent Liabilities

Don’t forget to account for unpaid taxes, medical bills, legal liens, and even informal loans from friends or family. Contingent liabilities - like pending legal settlements - should also be factored in, using conservative estimates to avoid inflating your net worth. Reviewing paystubs and bills regularly can help ensure you’re not missing overlooked liabilities, such as forgotten subscriptions or unused memberships.

Here’s a quick breakdown of the types of liabilities to consider:

| Category | Examples of Liabilities |

|---|---|

| Real Estate Debt | Primary mortgage, home equity lines of credit (HELOCs), second mortgages |

| Consumer Debt | Credit card balances, retail store cards, personal loans |

| Education & Auto | Student loans (federal and private), car loans, vehicle leases |

| Pending/Other | Unpaid taxes, medical bills, legal judgments, utility bills |

What Doesn't Belong in Net Worth Calculations

Understanding what to leave out of your net worth calculation is just as important as knowing what to include. Adding items that don't truly count as assets can give you a distorted view of your financial situation, potentially leading to poor financial decisions.

Leased or Borrowed Property

The key to net worth is ownership. A leased car, rented home, or borrowed equipment might be in your possession, but you don’t own them, and they hold no equity you can cash out. In fact, leases are liabilities - they represent ongoing financial obligations, not assets.

"A person's net worth statement is a rough estimate of what a person's collection of assets is worth after paying all its liabilities. Basically, it shows the net of what you own minus what you owe."

- Robert R. Johnson, Professor of Finance, Creighton University

Including leased items in your net worth can skew the numbers, making your financial health look better than it actually is. For example, driving a leased car doesn’t build wealth - it’s simply a recurring expense. The same goes for other low-value possessions that don’t contribute to your overall liquidity.

Unrealized Gains and Low-Value Personal Items

Unrealized gains - like the increased value of your home or stocks - are not actual wealth until you sell the asset and convert it to cash. Even then, selling often comes with costs that reduce the amount you walk away with.

Similarly, personal items such as clothing, furniture, and electronics don’t hold much resale value. While these items may have been expensive to buy, they depreciate quickly and add little to your financial security when it comes to liquidating assets.

"Items to leave out would be assets that have sentimental value only rather than monetary."

- Lauren Lippert, CFP, MAI Capital Management

It’s also important to avoid counting future income like salary raises, bonuses, or potential inheritances. Your net worth should reflect what you currently own and can access - not what you hope to earn down the road.

Personal Net Worth vs. National Economic Metrics

Focusing on liquid assets ensures your net worth remains a useful and realistic measure of your financial position. Personal net worth is simply the total of what you own minus what you owe. On the other hand, national economic metrics, like the Federal Reserve’s Survey of Consumer Finances, provide a broader view of wealth trends. For instance, in 2022, the median household net worth in the U.S. was $192,900, while households led by individuals aged 65–74 had a median net worth of $409,900. These numbers offer context but don’t directly impact your personal calculations.

A good rule of thumb? Apply the "liquidation rule": only count assets you could realistically convert to cash today. This approach may give you a clearer picture of your true financial standing and help you track your assets more accurately.

How Mezzi Helps Track Net Worth Accurately

Tracking your net worth accurately requires tools that can consolidate data, identify risks, and streamline tax calculations. Mezzi simplifies this process and may help reduce the chance of errors by automating much of the work. By focusing on a clear view of both assets and liabilities, Mezzi uses advanced technology to make managing your finances easier.

All Accounts in One Place

Mezzi brings all your financial accounts together - checking, savings, brokerage, and retirement plans - into one easy-to-use dashboard. Instead of juggling spreadsheets or doing manual calculations, you get a real-time view of your financial health. Asset values and liabilities are updated automatically, and the platform securely connects to major U.S. brokerages for seamless integration.

For items like real estate, vehicles, loans, or collectibles, you can manually add these to ensure a complete picture of your finances. Mezzi also categorizes your wealth into two key areas: "Portfolio" (liquid assets) and "Total Wealth" (everything you own). This distinction may clarify what part of your wealth is readily accessible versus your overall net worth.

This consolidated view lays the groundwork for deeper insights powered by Mezzi's AI tools.

Analysis and X-Ray Feature

Mezzi Advisor, an SEC-registered AI fiduciary, takes a comprehensive look at your financial situation. Using over 20 personal factors - like your retirement goals, tax profile, and risk tolerance - it provides tailored recommendations. The X-Ray feature goes a step further by identifying overlapping investments and potential risks from asset concentration.

Other tools include the AI Research Assistant, which provides information on wealth management concepts and portfolio performance, and Mezzi AI Chat, which can answer questions about tax-related topics or future value projections.

Tax Optimization Tools and Financial Calculator

Taxes can reduce your net worth, but Mezzi may help reduce this impact. It automates processes like automated tax-loss harvesting and wash-sale compliance while suggesting lower-cost ETF alternatives, which may improve outcomes.

The platform also calculates your "Liquid Net Worth", which factors in taxes, penalties, and commissions, giving you a realistic sense of what’s accessible. For long-term planning, the Financial Calculator projects your retirement savings based on your current portfolio, contributions, expected returns, and fees.

On top of these features, Mezzi may provide cost savings. Members have reported average annual savings of $10,000 in traditional advisory fees, while Core access plans start at $299 per year, covering AI fiduciary advice, 24/7 monitoring, and tax optimization.

Conclusion: Getting Your Net Worth Calculation Right

Net worth is a simple formula: total assets minus total liabilities. To get an accurate picture, always use current market values. Make sure to account for all debts - like mortgages, credit card balances, student loans, and medical bills. On the flip side, exclude leased items, unrealized gains, and any income you haven’t yet received.

"Focus on the trend of your net worth. Are you noticing over time that your assets are increasing and your debts decreasing? That means you're headed in the right direction." - Alissa Todd, Wealth Advisor, The Wealth Consulting Group

This advice highlights the importance of tracking your financial progress regularly. Monitoring trends - whether monthly or annually - can reveal if your financial habits are moving you closer to your goals or if lifestyle inflation is slowing you down. Avoiding errors in your calculations ensures your financial decisions are based on a clear, accurate understanding of your situation.

For self-directed investors juggling multiple accounts, combining traditional tracking methods with AI-powered tools may help identify common pitfalls, like missing hidden debts or overestimating asset values. Tools like Mezzi bring everything together - checking accounts, brokerage portfolios, retirement plans, and real estate - into a single dashboard with real-time updates. It also identifies risks, calculates your liquid net worth (after accounting for taxes and penalties), and provides projections of your financial future based on actual data.

FAQs

Should I include my home’s value or just my home equity?

When figuring out your net worth, make sure to include only your home equity - that’s the value of your home after subtracting the remaining mortgage balance. Avoid using the full market value of your property, as doing so would inflate your asset total.

Do my 401(k) and IRA balances count even if I can’t withdraw yet?

Yes, your 401(k) and IRA balances are part of your net worth, even if you can’t access the funds yet. These accounts are considered financial assets and should be factored into your net worth calculations.

How do I estimate my liquid net worth after taxes and selling costs?

To figure out your liquid net worth after taxes and selling costs, start by looking at assets that can quickly turn into cash, like savings accounts or investments. Then, subtract any estimated taxes - such as capital gains taxes - and selling fees tied to those assets. What’s left is your liquid wealth that’s readily available, giving you a clear and practical snapshot of your financial situation.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.