Yes, your 401(k) counts as part of your net worth. Here's why:

- Net worth is the total value of everything you own (assets) minus what you owe (liabilities).

- A 401(k) is an asset because it holds investments with current or potential value.

- Retirement accounts like 401(k)s made up 32.1% of household assets in 2022, often playing a major role in financial calculations.

However, when determining high-net-worth status, not all assets are treated equally. For example:

- Liquid assets (cash, stocks, bonds) are prioritized.

- Illiquid assets like your primary residence or art collections are often excluded.

For high-net-worth classifications:

- You typically need $1 million in liquid assets.

- The SEC sets thresholds at $750,000 in investable assets or $1.5 million in total net worth.

Key takeaway: Your 401(k) is part of your net worth, but its role in defining "high net worth" depends on liquidity and specific criteria.

Net Worth and High Net Worth Basics

How Net Worth Works

Net worth is the difference between what you own (your assets) and what you owe (your liabilities). This figure helps determine whether you're building wealth or experiencing financial shortfalls. Simply put: Assets - Liabilities = Net Worth.

Assets include things like cash, investments, real estate, personal belongings, and business interests. Here's a breakdown:

| Asset Category | Examples |

|---|---|

| Cash & Equivalents | Bank accounts, CDs, money market accounts |

| Investments | Stocks, bonds, mutual funds, 401(k)s |

| Real Estate | Primary residence, investment properties |

| Personal Property | Vehicles, valuable collections |

| Business Interests | Company ownership, partnerships |

Liabilities, on the other hand, cover debts such as mortgages, car loans, student loans, and credit card balances. For example, if you own a $250,000 home, have $100,000 in investments, and $25,000 in other assets - but owe $100,000 on your mortgage and $10,000 in car loans - your net worth would be $265,000.

Understanding this calculation is essential for diving into what defines high net worth.

High Net Worth Requirements

Once you've calculated your net worth, determining high-net-worth status focuses on liquid assets - assets that can quickly be converted to cash. Generally, someone is considered a high-net-worth individual (HNWI) if they have at least $1 million in liquid assets.

The Securities and Exchange Commission (SEC) uses slightly different benchmarks. According to the SEC, a person qualifies as wealthy if they have:

- $750,000 in investable assets, or

- $1.5 million in total net worth.

In 2023, the global HNWI population reached 22.8 million people, controlling about $86.8 trillion in wealth. North America leads with the largest share, home to approximately 7.9 million HNWIs.

However, not all assets count toward high-net-worth status. The following are typically excluded:

- Primary residence value

- Fine art collections

- Antiques

- Other illiquid assets

These exclusions ensure that wealth calculations focus on resources that are readily accessible.

401(k)s in Net Worth Calculations

How 401(k)s Count as Assets

A 401(k) is a key part of net worth calculations. These accounts hold securities and investment products that carry either current or potential value. In the U.S., 401(k)s and other retirement accounts make up a large portion of household wealth, often dominating financial portfolios.

For individuals with significant wealth, 401(k)s and IRAs can account for as much as 55% of their total assets.

"Your 401(k), and any other retirement accounts, are financial assets. These are portfolios in which you hold securities and investment products with either realized or potential value."

That said, there are instances where adjustments to the value of these accounts may be necessary.

When 401(k)s Don't Count

In some cases, it’s important to adjust or even exclude 401(k) values to ensure accurate net worth calculations:

- 401(k) Loans: If you've borrowed against your 401(k), the loan amount should be treated as a liability or deducted from the account balance.

- Small Balances: Balances under $25 are often excluded from calculations since they’re considered too minor to impact overall net worth.

- Pension Plans: Unlike 401(k)s, traditional pension plans generally don’t factor into net worth calculations, even though they provide retirement income.

These adjustments are especially crucial for those nearing high-net-worth status, as precision in calculating net worth becomes increasingly important.

Net Worth Calculation Steps

Calculate Your Net Worth

| Asset and Liability Categories for Calculation | |

|---|---|

| Assets to Include | Liabilities to Include |

| Cash & Bank Accounts | Credit Card Debt |

| 401(k) & Retirement Accounts | Mortgage Balance |

| Investment Portfolios | Auto Loans |

| Real Estate | Student Loans |

| Vehicles & Personal Property | Personal Loans |

To figure out your net worth:

-

List All Assets

Write down all your assets at their current market value. This includes your 401(k) balance, which you can find on your latest statement. -

List All Liabilities

Record every debt you owe, including any loans against your 401(k). -

Calculate Net Worth

Subtract your total liabilities from your total assets. The result is your net worth.

This method ensures that your retirement accounts are correctly included in the overall assessment of your financial standing. The example below shows how these steps come together to calculate net worth.

Sample Net Worth Calculation

| Assets | Value |

|---|---|

| 401(k) Balance | $175,000 |

| Home Market Value | $450,000 |

| Savings Account | $35,000 |

| Investment Account | $65,000 |

| Vehicle | $25,000 |

| Total Assets | $750,000 |

| Liabilities | Amount |

|---|---|

| Mortgage Balance | $325,000 |

| 401(k) Loan | $15,000 |

| Car Loan | $12,000 |

| Credit Card Debt | $5,000 |

| Total Liabilities | $357,000 |

In this case, the net worth calculation is:

- Total Assets ($750,000) - Total Liabilities ($357,000) = $393,000 Net Worth

Retirement accounts often play a major role in household net worth, though the exact contribution depends on individual circumstances.

401(k) millionaires are a growing demographic

Net Worth Management Tools

Modern financial tools now bring all your accounts - like 401(k)s - into one live dashboard, making it easier to monitor and improve your portfolio.

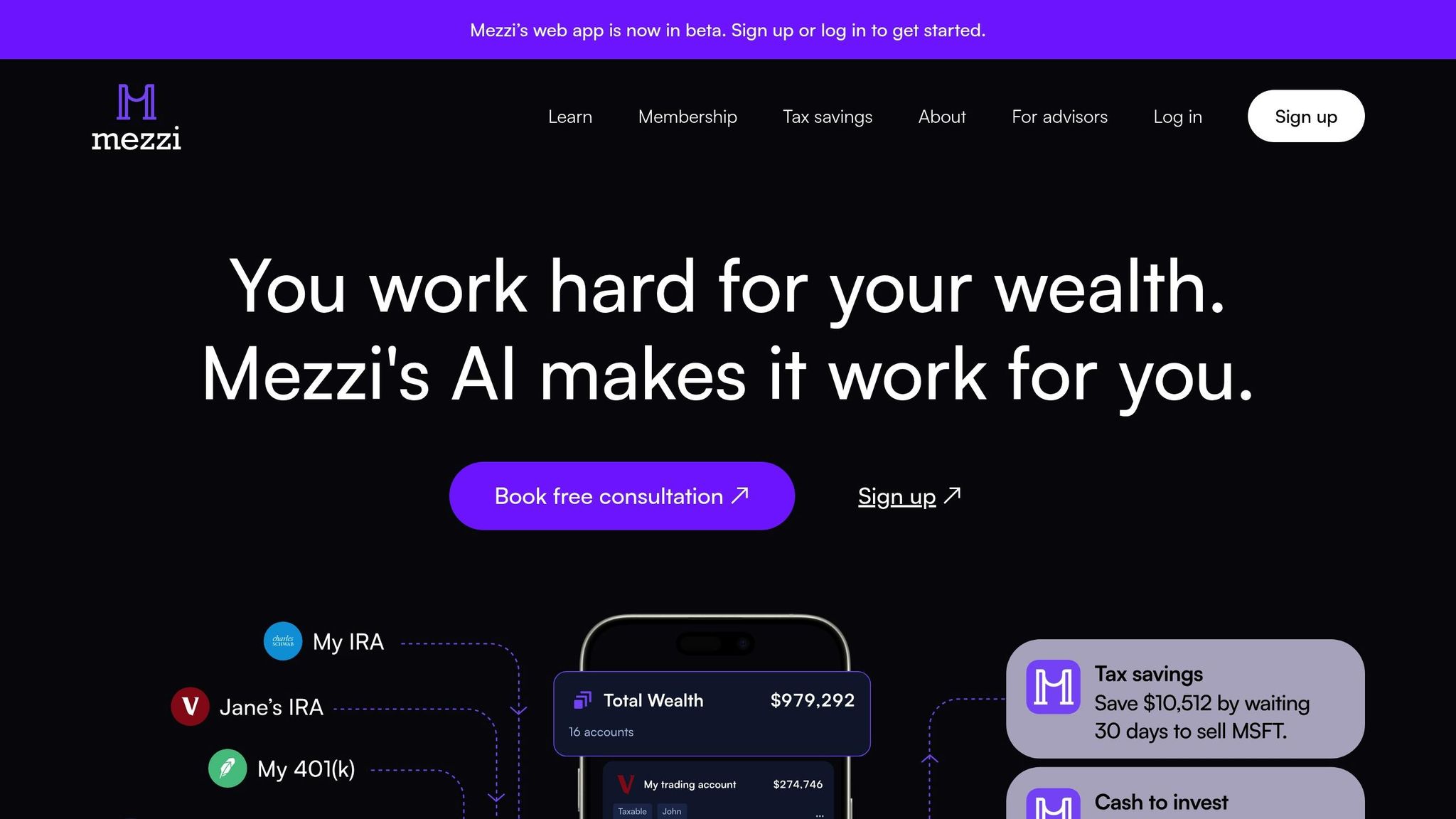

Mezzi's Net Worth Tracking Features

Mezzi brings together all your financial accounts, including 401(k)s, into one place. Its dashboard gives you a full picture of your assets and debts.

Here’s what Mezzi offers for managing your net worth:

| Feature | What It Does |

|---|---|

| Account Aggregation | Combines all accounts, including 401(k)s, into one clear view. |

| Portfolio X-Ray | Identifies hidden stock exposures across your retirement accounts. |

| Fee Analysis | Shows where you could save on investment fees (users save an average of $186,877 for retirement). |

| Tax Optimization | Reveals tax-saving opportunities that could total up to $76,123 over 30 years. |

"Mezzi's X-Ray feature allowed me to uncover exposure to stocks I didn't realize I had."

– Shuping, Founder of Summer AI

In addition to tracking, Mezzi uses AI to fine-tune your financial approach.

AI Tools for Financial Planning

Mezzi’s AI features help users get the most out of their retirement portfolios. It offers personalized insights for reducing fees, managing risks, and improving portfolio performance.

Some standout AI features include:

- Real-time Investment Analysis: Reviews your portfolio and suggests rebalancing without selling when needed.

- Tax Strategy Recommendations: Pinpoints potential tax savings across different account types.

- Fee Optimization: Compares expense ratios to highlight ways to lower investment costs.

- Risk Assessment: Examines your portfolio for concentration risks or hidden exposures.

On average, users uncover over $1,000 in yearly tax and fee savings with Mezzi. With a 4.8/5 rating on the App Store, it’s praised for managing multiple accounts - like 401(k)s, brokerage accounts, and 529 plans - all in one place.

Summary

401(k) plans are a major part of household wealth. In 2022, retirement accounts like 401(k)s made up 32.1% of the typical household's net worth, slightly edging out home equity at 31.4%.

For wealthier individuals, these accounts can represent as much as 55% of their total assets. This highlights why it's essential to include 401(k)s when calculating net worth.

Certified financial planner Michelle Brownstein explains:

"The strategies needed to get rich are different from the ones required to stay rich and eventually earn on your money." - Michelle Brownstein, vice president of Empower Private Client Group

To get the most out of your 401(k) and grow your net worth, consider these steps:

- Track your net worth quarterly, making sure to include all retirement accounts

- Max out employer matching contributions to take full advantage of free money

- Seek professional advice for fine-tuning your financial strategy

Age-specific benchmarks reveal notable differences in net worth, emphasizing the importance of accurate tracking. By combining precise calculations with modern tools, you can make the most of your 401(k) and other investments.

FAQs

Does a 401(k)'s liquidity affect whether it counts toward high-net-worth status?

A 401(k)'s liquidity can influence how it factors into your high-net-worth status. Liquidity refers to how easily an asset can be converted to cash without a significant loss in value. Since 401(k) funds are typically subject to penalties and taxes if withdrawn before retirement age, they are considered less liquid compared to other assets like savings or investments in brokerage accounts.

While 401(k) balances contribute to your overall net worth, their limited liquidity may affect how they are viewed in financial assessments, especially for determining liquid net worth. Understanding this distinction can help you better evaluate your financial standing and plan effectively for the future.

Does a 401(k) count toward my net worth?

Yes, your 401(k) is included when calculating your net worth. Net worth is determined by subtracting your total liabilities (debts) from your total assets, and your 401(k) balance is considered one of those assets.

To get an accurate picture of your net worth, include the current value of your 401(k) along with other assets like savings, investments, and property. Keep in mind that while your 401(k) is part of your net worth, it’s a retirement account, so accessing those funds early may come with penalties or tax implications.

Why aren't certain assets, like your home or art collection, included in high-net-worth calculations?

Certain assets, such as your primary residence, are typically excluded when calculating high net worth. This is because organizations like the SEC require the value of your primary home to be left out when determining if you meet the $1 million net worth threshold to qualify as an accredited investor.

The reasoning behind this exclusion is that a primary residence is considered a personal-use asset rather than an investment. Similarly, other personal assets, like art collections, may also be excluded unless they are explicitly treated as investments or sold for financial gain.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.