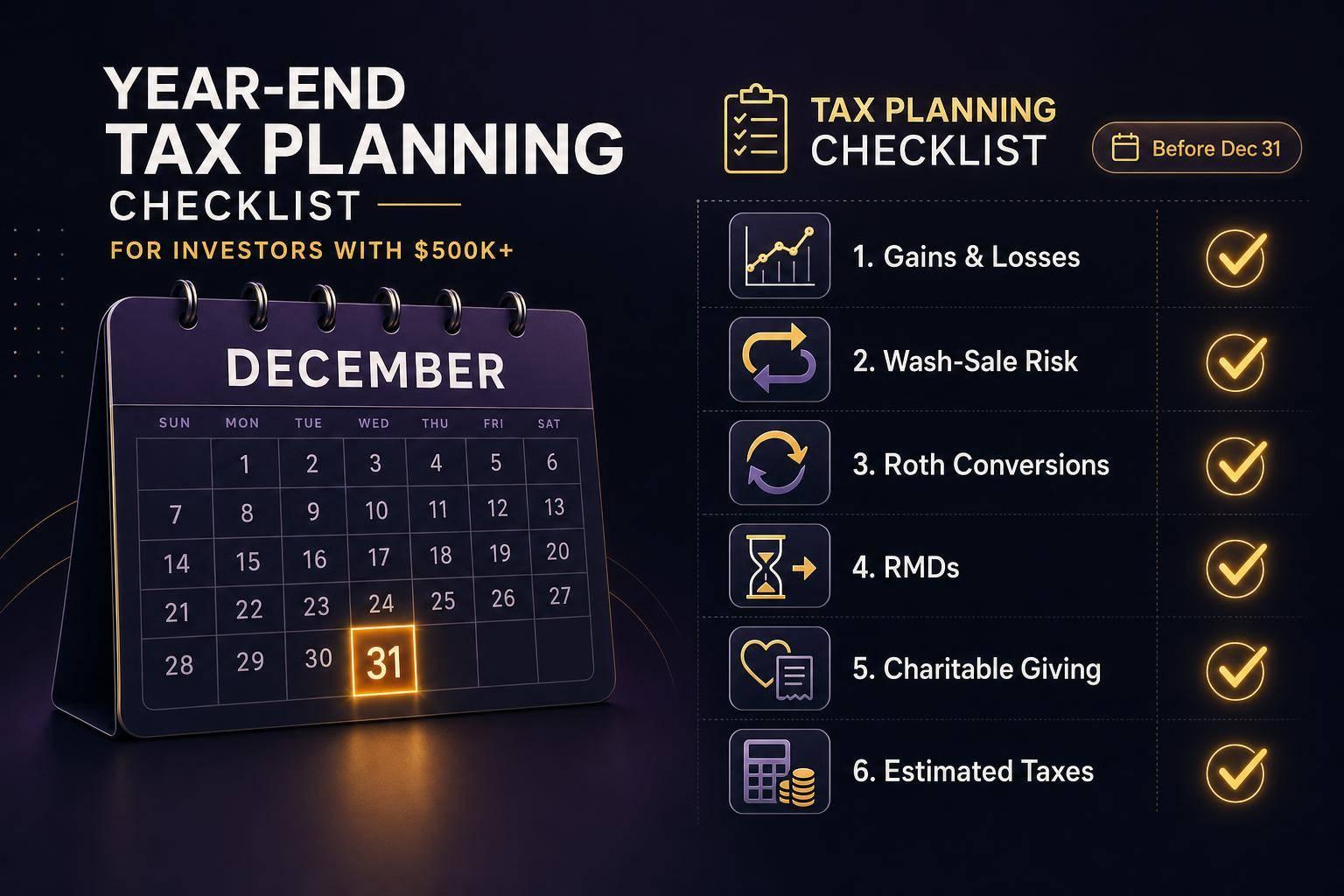

If I wait until late December, I may miss tax moves that need to happen by 12/31/2026. For investors with $500,000+ across brokerage accounts, IRAs, Roth accounts, HSAs, and stock comp, the main year-end risks may come from timing and account overlap.

Here’s the short version:

- I may want to review realized gains, losses, and fund distributions across all taxable accounts

- I may need to check for wash sale risk across my accounts, my IRA, and a spouse’s accounts

- I may look at asset location, Roth conversion room, and RMD status before year-end

- I may compare charitable gifting methods, tax payments, and RSU / ISO / ESPP timing

- I may also watch income thresholds tied to items like the 3.8% NIIT, capital gains rates, and future IRMAA surcharges

A few numbers may shape the review:

- Up to $3,000 in net capital losses may offset ordinary income

- The NIIT may apply above $250,000 of MAGI for joint filers

- The 20% long-term capital gains rate may start at $613,700 of taxable income for married filing jointly

- Roth conversions may need to be done by December 31, 2026

- Missing an RMD may trigger a 25% penalty on the amount not distributed

- QCDs may go up to $111,000 in 2026

| Area | What I may review before 12/31/2026 | Why it may matter |

|---|---|---|

| Gains and losses | Realized gains, carryforwards, lot selection, fund payouts | Tax cost may change based on timing and share lots |

| Wash sales | Taxable accounts, IRAs, 401(k)s, DRIPs, spouse accounts | A loss may be disallowed if the same holding gets repurchased |

| Retirement moves | Asset location, Roth conversions, RMDs, QCDs | Income this year and later years may be affected |

| Year-end cash flow | Charity, withholding, estimated taxes, equity comp | Late-year income may change bracket space and tax due |

The core idea is simple: this may be less about finding extra tactics and more about seeing every account in one place before the year closes.

Year-End Tax Planning Key Numbers for Investors with $500K+

1. Review gains, losses, and year-end distributions

1.1 Pull realized gains and losses across every taxable account

Before making trades in November or December, pull together a full year-to-date tax picture. Start with realized gain and loss reports from every taxable brokerage account. Then split them into short-term positions, held one year or less, and long-term positions, held more than one year. That split matters because the two categories may be taxed at very different rates.

Then add in other year-to-date income, including W-2 wages, bonuses, RSU vests, and any business K-1s. For 2026, the 3.8% Net Investment Income Tax (NIIT) may apply when MAGI exceeds $250,000 for joint filers, and the 20% long-term capital gains rate may begin at $613,700 of taxable income for married couples filing jointly.

Apply any prior-year capital loss carryforwards before harvesting new losses. Look at the combined year-to-date total across all accounts, not each account on its own.

"Selling a winning position one day before the one-year mark turns the gain from long-term to short-term, potentially doubling the federal tax rate." - Avior Wealth Management

1.2 Harvest losses where they actually improve your tax picture

Not every paper loss makes sense to harvest. The more useful cases may be positions that are down, where you'd be fine moving into a similar replacement, and where the realized loss may offset gains you've already locked in this year.

In general, short-term losses are used first, then long-term losses. If losses go beyond gains, up to $3,000 may offset ordinary income, and the rest may carry forward. For higher earners, tax-loss harvesting may also reduce NIIT exposure. And this applies only to taxable brokerage accounts. Losses inside IRAs or 401(k)s do not create deductible capital losses.

When selling, use specific lot identification so you can choose your highest-cost shares. If you leave the default setting at "first-in, first-out" or FIFO, the sale may pull your lowest-basis shares first. That may shrink the loss and leave you with a larger tax bill.

1.3 Check fund capital gain distributions before buying in late year

Before adding to a taxable fund position late in Q4, check the fund's distribution schedule. Mutual funds must distribute realized capital gains to shareholders each year, and many do so in November or December.

Here's the catch: if you buy before that taxable distribution, you may owe tax on gains the fund built up before you owned any shares. The share price often drops by the amount of the distribution, so you may end up with a tax bill without any economic gain to match it.

A quick check of the fund provider's website may help. Look for year-end distribution estimates and ex-dividend dates. If a fund shows a large expected distribution, some investors wait until after the ex-dividend date before making new taxable purchases.

"An investor who buys a fund in October may receive a substantial taxable distribution shortly after, even though their personal holding period was only a few weeks." - Avior Wealth Management

Active mutual funds may be more likely to make late-year gain distributions. Broad-market ETFs usually are not. This tends to matter most in taxable accounts, since fund distributions inside an IRA or 401(k) are not taxed right away.

Before you sell anything, check wash sale risk across every account.

2. Check wash sale risk and other multi-account blind spots

2.1 Audit wash sale exposure across all account types and spouse accounts

Wash sale rules cover the 30 days before and after a sale, and they may apply across taxable accounts, IRAs, 401(k)s, and spouse accounts.

The biggest trap may show up in an IRA. If you sell a position at a loss in a taxable brokerage account and a dividend reinvestment buys that same security inside your IRA during the wash sale window, the loss may be permanently disallowed. That’s because the IRA basis may not be adjusted to reflect the loss.

DRIPs and recurring purchases may also trigger wash sales without any deliberate move on your part. Before a loss sale, some investors pause DRIPs and recurring buys. It may also make sense to check whether a spouse already holds, or may be scheduled to buy, the same security in another account.

| Account Type | Wash Sale Risk | Key Risk Factor |

|---|---|---|

| Taxable Brokerage | High | Main harvesting account; easiest to see |

| Traditional / Roth IRA | Critical | A repurchase here may permanently disallow the loss |

| Spouse's Accounts | High | Purchases here may create wash sale risk across the household |

2.2 Pre-select substitute funds before you harvest losses

The goal may be to keep similar market exposure while moving into a different fund. For example, an investor may sell SPY and buy VOO to keep S&P 500 exposure without repurchasing the same fund.

It also may help to document substitute funds ahead of time. That way, year-end harvesting may be more of a planned move and less of a last-minute scramble. Once those substitutes are set, review every account that may repurchase the original holding.

2.3 Use a whole-portfolio view to catch overlap and duplicate holdings

A full portfolio view may make it easier to spot duplicate holdings, hidden concentration, and wash sale exposure across all accounts before a trade goes through.

"Modern brokerage reporting makes it easier for the IRS to detect disallowed losses." - Agemy Financial Strategies

With wash-sale risk reviewed, the next step may be retirement accounts and Roth planning.

3. Review retirement accounts, asset location, and Roth moves

3.1 Check whether tax-inefficient assets are in the wrong accounts

After trade timing, look at high-net-worth investing strategies for where each asset sits across your accounts. In many cases, location may matter almost as much as the investment itself.

A common setup some investors use is to hold bonds, REITs, and high-turnover funds inside tax-deferred accounts like a traditional IRA or 401(k), while keeping tax-efficient index ETFs and low-turnover stock funds in taxable accounts. Roth accounts are often used for assets with more growth potential and a longer time horizon, since qualified withdrawals are tax-free and future gains may avoid tax as well.

Once that piece is in place, the next step may be checking whether a Roth conversion still makes sense before Dec. 31.

3.2 Evaluate Roth conversion room before Dec. 31

Roth conversions must be completed by Dec. 31. One approach some people consider is estimating 2026 taxable income, then converting only enough to stay within the current bracket rather than spilling into the next one. When taxes are due, some people pay them with cash outside the IRA.

For 2026, the 24% federal bracket tops at $206,700 for single filers and $394,600 for joint filers. It may also make sense to check the 2028 IRMAA effect before converting.

"Roth conversions can lock in today's low tax rates and reduce future RMDs, IRMAA, and taxation of Social Security." - Chris Wilbratte, Founder, Echelon Financial

If you're age 50 or older and had more than $150,000 in W-2 wages in the prior year, it may be worth confirming that 401(k) catch-up contributions are coded as Roth starting in 2026.

Next, review any required distributions that still need to happen before year-end.

3.3 Confirm remaining RMDs and decide which account will fund them

The RMD deadline is December 31, 2026, and the penalty for missing it may be 25% of the amount not distributed. If 2026 is your first RMD year, the first withdrawal may be delayed until April 1, 2027, though that may lead to two distributions landing in 2027 and may push taxable income into a higher bracket.

Before year-end, confirm required distributions across each IRA that applies. Inherited IRA RMDs cannot be aggregated with your own traditional IRA distributions, so they need to be tracked and completed separately.

For donors age 70½ and older, a Qualified Charitable Distribution (QCD) may satisfy an RMD while keeping that amount out of AGI, up to $111,000 in 2026. That lower AGI may reduce IRMAA surcharges and the share of Social Security subject to tax. In some cases, it may also work better than an itemized deduction because it lowers AGI directly.

| RMD Key Figures (2026) | Value |

|---|---|

| RMD starting age | 73 |

| Deadline | December 31, 2026 |

| Penalty for missing RMD | 25% of undistributed amount |

| QCD maximum limit | $111,000 |

| Minimum age for QCDs | 70½ |

4. Handle charitable gifts, estimated taxes, and equity comp before year-end

4.1 Choose the most tax-efficient way to give to charity

With RMDs and Roth moves reviewed, shift to the year-end items that may still directly affect 2026 taxable income.

If you plan to give this year, the asset you donate may matter just as much as the amount. Donating long-term appreciated stock directly to a charity - or to a donor-advised fund (DAF) - may let you avoid capital gains tax on the appreciation while still deducting the full fair market value.

Starting in 2026, itemizers may only deduct the portion of charitable contributions that exceeds 0.5% of AGI. On a $400,000 AGI, the first $2,000 of giving may produce no deduction. One way some people deal with that is bunching: combining two or three years of giving into one DAF contribution to get past the deduction floor in a high-income year.

| Giving Method | Tax Treatment | Best Use Case |

|---|---|---|

| Appreciated Securities | Full FMV deduction plus no capital gains tax | High-value gifts from taxable brokerage accounts |

| Donor-Advised Fund (DAF) | Immediate deduction; grants to charities may happen over future years | High-income years or multi-year giving plans |

| Qualified Charitable Distribution (QCD) | Direct transfer from IRA custodian to charity; excluded from gross income | Investors age 70½+ managing IRMAA or Social Security taxation |

Appreciated stock transfers typically take 5–10 business days to process, so starting by early to mid-December may make sense.

4.2 Reconcile withholding and estimated tax payments

Next, match tax payments to the income you may have already locked in.

Compare year-to-date withholding and estimated payments with projected tax liability, then address any shortfall before Dec. 31. Increasing W-2 withholding through a revised Form W-4 may be more effective than making an estimated payment because the IRS treats withholding as paid evenly throughout the year, which may retroactively cover earlier quarters. Q4 estimated tax is credited when paid and is due Jan. 15, 2027.

If you itemize, paying your final state estimated tax installment by December 31 instead of waiting until January may let you claim that amount under the SALT deduction in the current tax year. The SALT cap under the One Big Beautiful Bill Act is $40,400 for 2026.

4.3 Review RSUs, options, and ESPP activity, then build a Dec. 31 action list

Then check compensation events that may undo the bracket space you planned to use.

RSU vests add ordinary income and may push income into higher tax brackets, NIIT, and future IRMAA. A large vest late in the year may also make a Roth conversion less appealing, since the bracket space you planned to use may already be filled.

Before Dec. 31, check whether an ISO exercise may trigger AMT; a same-year disqualifying disposition may reduce that risk. For ESPP shares, confirm whether you've met the qualifying disposition holding periods: two years from the offering date and one year from the purchase date.

A short Dec. 31 action list may help keep timing-sensitive items from slipping:

- Roth conversions

- QCDs

- Final state estimated tax payments

- Charitable stock transfers

IRA and HSA contributions may move to the April 15, 2027 deadline.

Tax Planning Strategies to Consider for 2026

Conclusion: Year-end tax moves $500K+ investors should not leave to chance

The biggest avoidable mistakes at this portfolio level may share one cause: accounts may be managed in isolation.

A loss harvested in one account may trigger a wash sale in a spouse's account or IRA. RMDs from inherited IRAs may not be aggregated with traditional IRAs, which may be a common source of filing errors. A large Roth conversion or capital gain may push MAGI higher than expected and may be associated with higher Medicare premiums two years later.

These issues may be predictable when several accounts are handled separately. Those moves may only work as intended when you may see their cross-account effects before Dec. 31.

"A year-end tax review is not about finding every possible trick. It is about seeing the year before it closes." - OnWealth Editorial Team

Dec. 31 is fixed. Your visibility into the remaining moves may not be.

Wash sale exposure, asset location gaps, unconfirmed RMDs, charitable timing, and estimated tax shortfalls may all call for a complete, current view of every account, not a spreadsheet pulled together from last month's statements.

That is why a whole-portfolio view may matter at year-end. Mezzi's read-only platform connects taxable accounts, IRAs, Roth accounts, and 401(k)s without moving assets. It flags wash sale risk, asset location inefficiencies, and Roth conversion and tax-loss harvesting opportunities based on your actual holdings.

Before Dec. 31, the main question may be simple: do you have a clear enough view of every account to act?

FAQs

How do I avoid wash sales across all my accounts?

To avoid wash sales, some investors try not to buy substantially identical securities during the 61-day window around the sale: 30 days before and 30 days after. That may apply across all accounts, including retirement accounts and automatic equity compensation such as RSU vesting or ESPP purchases.

If someone wants to keep market exposure while harvesting a loss, one approach may be to replace the sold holding with a similar security that is not substantially identical.

Should I harvest losses or use carryforwards first?

You don’t have to choose. The tax code may apply capital losses in a set order automatically.

Losses first offset gains of the same type: short-term against short-term and long-term against long-term. Any net losses left over may then offset the other type of gain. If losses still exceed gains, up to $3,000 may offset ordinary income, and the rest may carry forward indefinitely.

When does a Roth conversion make sense before year-end?

A Roth conversion may make sense before December 31 if your taxable income is unusually low this year and may be higher in retirement. That situation may come up after a business slowdown, a sabbatical, or a major loss.

A common way to think about it: project your full-year taxable income, then look at how much room may be left in your current tax bracket. It may also make sense to factor in Medicare IRMAA.

Some people avoid converting if they’re already in the 37% bracket or if they don’t have non-IRA cash available to pay the tax.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.