If I wanted the short answer: Mezzi may fit many self-directed investors best, Empower may fit people who want a free dashboard, Kubera may fit people with crypto or private assets, and Simplifi or Monarch may fit budgeting-first households.

Here’s the simple breakdown:

- Mezzi may fit multi-account investors who want tax views, wash-sale checks, asset-location ideas, and read-only tracking

- Empower Personal Dashboard may fit investors who want a free portfolio and net worth view with fee analysis

- Kubera may fit people tracking crypto, real estate, private equity, and global accounts

- Quicken Simplifi may fit people who want budgeting + light investment tracking at a lower yearly cost

- Monarch Money may fit couples or households that want shared money tracking with basic portfolio views

A few numbers stand out:

- Mezzi: starts at $299/year

- Empower: free dashboard; paid advisory starts at 0.89% AUM

- Kubera: starts at about $249/year

- Quicken Simplifi: about $47.99 to $71.88/year

- Monarch Money: $14.99/month or about $99.99/year on annual plans, depending on current offers

What separates these tools may be pretty simple:

- Some focus on portfolio analysis

- Some focus on net worth tracking

- Some focus on budgeting

- Only a few go beyond balances and show tax-aware portfolio checks across accounts

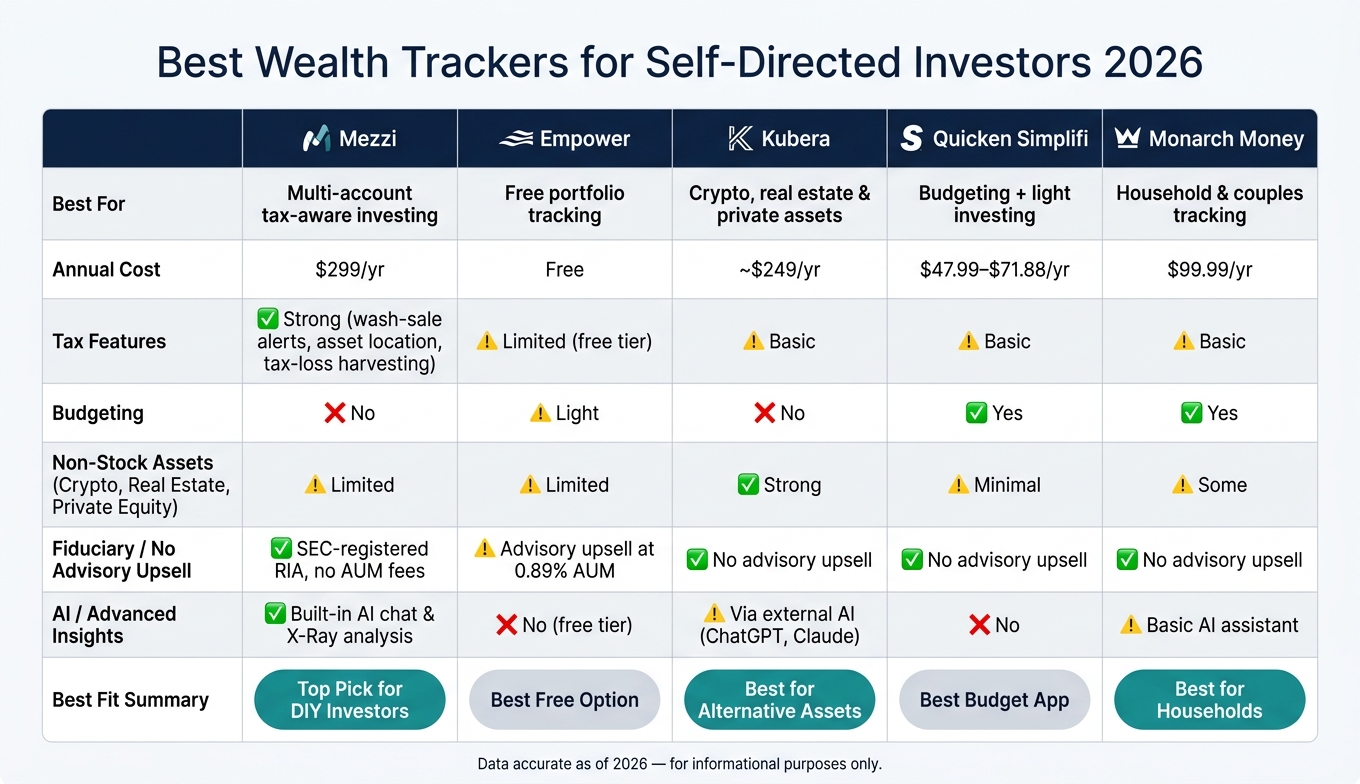

Best Wealth Trackers for Self-Directed Investors 2026: Side-by-Side Comparison

6 Best Net Worth Tracking Apps of 2026 (Tested & Reviewed)

Quick Comparison

| Tool | Best for | Cost | Tax features | Budgeting | Non-stock assets |

|---|---|---|---|---|---|

| Mezzi | Self-directed investors with multiple accounts | $299/year+ | Stronger than others in this group | No | Limited |

| Empower | Free portfolio tracking | Free | Limited in free tier | Light | Limited |

| Kubera | Net worth tracking across many asset types | ~$249/year+ | Basic | No | Strong |

| Quicken Simplifi | Budgeting with light investing tools | $47.99–$71.88/year | Basic | Yes | Limited |

| Monarch Money | Household money tracking | $99.99/year or $14.99/month | Basic | Yes | Some |

So if I were comparing these tools fast, I’d look at account type, tax optimization features, and whether I want budgeting or portfolio analysis first.

1. Mezzi

Mezzi is a read-only portfolio tracker for self-directed investors who want advisor-style analysis without handing over control. It connects to 401(k)s, Roth IRAs, Traditional IRAs, taxable brokerage accounts, HSAs, and more through Plaid and Finicity, then reviews holdings across all linked accounts. Mezzi does not place trades or move money. That setup may matter even more when tax rules apply across several accounts at once.

It scans taxable accounts for tax-loss harvesting opportunities and flags wash-sale risk across linked accounts before and after you trade. That may matter because trades often happen across separate custodians, not just inside one account. So a pending transaction at one institution may affect a planned sale at another.

Mezzi also shows where holdings overlap. The Portfolio X-Ray tool surfaces combined exposure across a 401(k), Roth IRA, and taxable account, so you may see where your portfolio is more concentrated than expected. It also highlights fund fees and expense ratios, which may make duplicate exposure easier to spot and may help simplify the portfolio.

For investors balancing taxable and retirement accounts, Mezzi also looks at asset location. It reviews what you hold and where you hold it, then suggests more tax-efficient placement. For example, it may suggest moving a high-yield bond fund from taxable into a Traditional IRA while keeping a low-turnover equity index ETF in taxable. For mixed-account investors, that approach may improve after-tax returns.

Mezzi uses a flat annual subscription model rather than charging a percentage of assets under management. The current tiers are Core at $299/year, Plus at $499/year, and White Glove at $1,499/year. For investors who want guidance without AUM fees, a flat subscription may cost less.

| Plan | Price | Best For |

|---|---|---|

| Core | $299/year | Unlimited AI chat, 24/7 monitoring, tax optimization, returns analysis, and X-Ray |

| Plus | $499/year | Advanced AI research and concierge support via video, phone, and email |

| White Glove | $1,499/year | Hands-on AI coaching and unlimited support calls for high-net-worth or complex portfolios |

2. Empower Personal Dashboard

Empower Personal Dashboard, formerly Personal Capital, is a free portfolio tracker that links investment accounts and connected cash accounts through Plaid and Yodlee. It updates investment prices during the trading day, shows asset allocation, and flags cash held inside mutual funds. For self-directed investors, that may make the tool more than a simple account view. It may also offer a clearer look at fees and portfolio mix.

The standout free feature may be the Retirement Fee Analyzer. It scans linked funds and ETFs, calculates a weighted average expense ratio across accounts, and turns those expense ratios into projected dollar costs. That kind of view may help some investors spot fund costs that are easy to miss when accounts sit in different places.

There are limits, though. The dashboard is read-only, so it may surface insights but it doesn't place trades or rebalance a portfolio. Tax-aware rebalancing sits behind Empower's paid advisory tier, which starts at 0.89% AUM and has a $100,000 minimum. Crypto has to be entered manually, and real estate values come from Zillow instead of syncing on their own. In practice, that may keep Empower more useful for visibility than for hands-on portfolio control.

The free dashboard also acts as an entry point to Empower's advisory business.

Empower may be strongest for free tracking and fee visibility. Investors who want tax-aware monitoring or AI tools for portfolio performance tracking may need something with more depth.

3. Kubera

For investors with nontraditional assets, Kubera puts the spotlight on total net worth instead of day-to-day account activity. It's a net-worth dashboard, not a transaction tracker. Kubera connects to more than 20,000 financial institutions through nine aggregators, including Plaid, Yodlee, MX, and Akoya, and routes each institution through the connection that may be the most reliable at that moment. On top of standard brokerage and bank accounts, it also tracks crypto wallets, DeFi positions, real estate, vehicles, domain names, and private equity.

That broad asset coverage may make aggregation easier, especially for people whose finances don't fit neatly into a standard brokerage view. But Kubera may feel lighter if someone wants deep portfolio analysis or tax reporting. It reports IRR, but not time-weighted return, benchmarks, or risk metrics, and its tax features are limited to basic estimates. There is also no trade execution or automated rebalancing.

Kubera takes a different path on AI. Instead of building its own analysis layer, it relies on outside AI tools through Model Context Protocol (MCP) integration. That setup lets users send portfolio data to ChatGPT, Claude, or Perplexity for analysis.

Pricing starts at about $249 per year for Essentials, while Kubera Black costs $2,500 per year. Revenue comes entirely from subscriptions. It also includes an inactivity-triggered beneficiary feature: if a user is inactive for a set period, named beneficiaries automatically receive read-only access to the portfolio and stored documents.

4. Quicken Simplifi

After Kubera’s big-picture net worth view, Simplifi shifts back to day-to-day money management with budgeting built in. Quicken Simplifi combines investment tracking and budgeting in one dashboard. It connects to 14,000+ financial institutions, including 401(k)s, IRAs, 403(b)s, brokerage accounts, and crypto exchanges, through Plaid and Quicken’s bank-linking network. It also includes real-time market data for stocks, ETFs, mutual funds, and cryptocurrency, along with a news feed and asset allocation by class.

Simplifi calculates both TWR and IRR, which may give investors two ways to look at results: strategy performance and personal performance.

Its tax views are more limited. You get cost basis, total costs, and gains. But features like stock screening, benchmark comparisons, and wallet-based crypto tracking are not included. It also does not place trades or automate rebalancing.

Pricing starts at $3.99/month when billed annually for new subscribers. Standard pricing runs $5.99 to $6.99/month, also billed annually. There’s no monthly billing and no free trial, though there is a 30-day money-back guarantee. That may make Simplifi a lighter option for investors who want portfolio visibility inside a budget app. Monarch Money takes a more household-focused approach to that same idea.

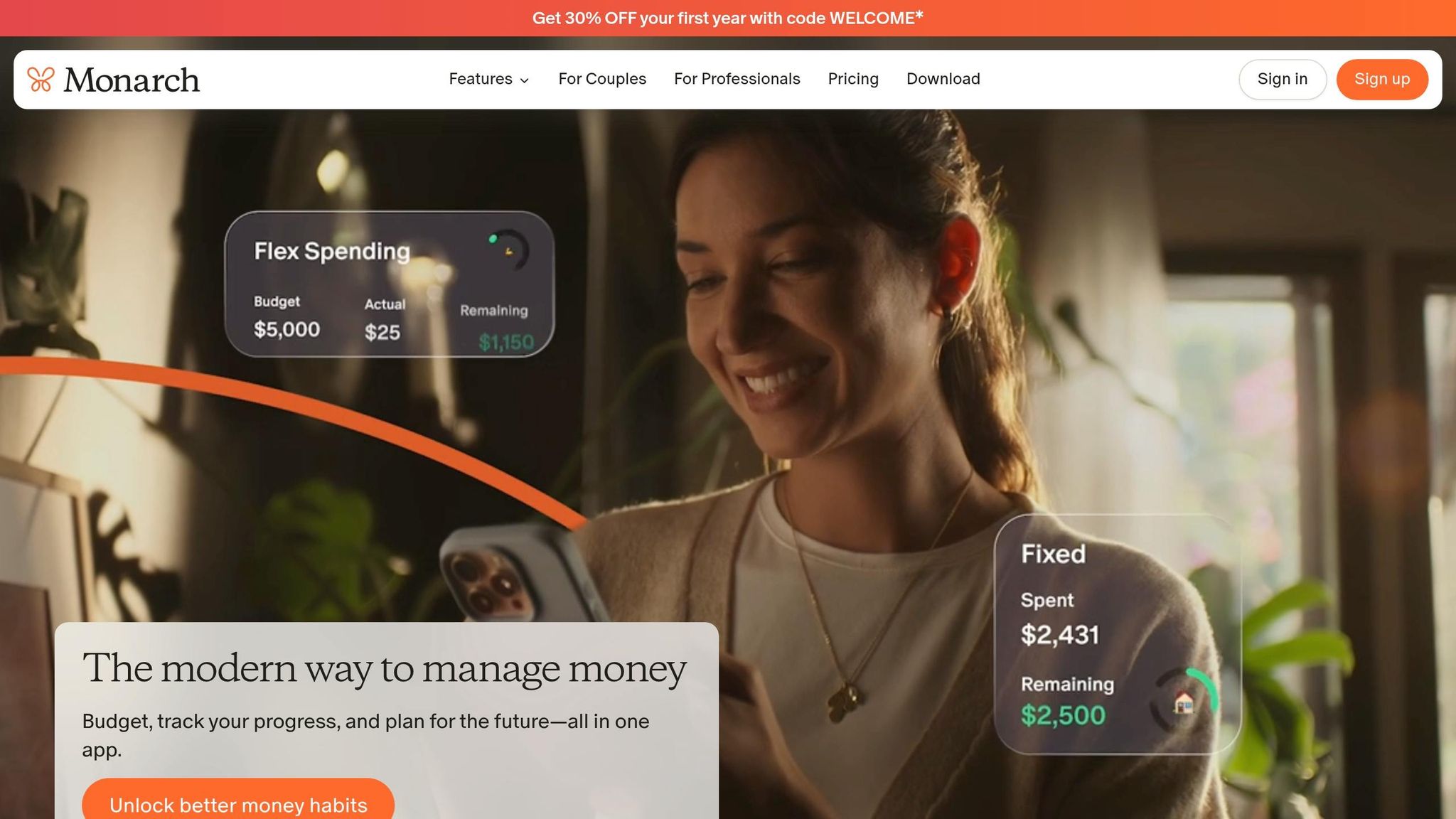

5. Monarch Money

Monarch Money connects to 13,000+ financial institutions through Plaid, Finicity, and MX, and it tracks stocks, ETFs, mutual funds, bonds, crypto, real estate, and vehicles. One detail stands out: if a brokerage connection breaks, you may switch data providers for that account without contacting support. That may help keep a household-level view in place, even when accounts sit across different institutions.

It also has "Shared Views" for couples or households that may want shared visibility without pooling every detail into one setup. You may label accounts as "Yours", "Mine", or "Ours," which may preserve some privacy while still showing a combined net worth. Monarch also includes a AI software for preparing for retirement assistant that you may ask about portfolio topics, such as how higher 401(k) contributions may affect projected net worth.

For self-directed investors, the tradeoff may be depth. Monarch offers basic allocation and performance views, but it does not include fee analysis, tax-loss harvesting, wash-sale alerts, automated rebalancing, or advanced retirement modeling.

Monarch is read-only. It uses a subscription model and does not rely on ads or data sales. Pricing is $14.99 per month, and it includes a 7-day free trial.

How the top tools compare on the features that matter most

For self-directed investors, four areas may shape the choice more than anything else: aggregation, tax insight, control, and cost. That’s where the clearest differences tend to show up.

Account aggregation

Aggregation quality may depend on three things: how many accounts a tool connects, how reliable the data looks after syncing, and how much cleanup you may need to do yourself.

| Tool | Supported institutions | Holdings detail | Nontraditional assets | Manual input |

|---|---|---|---|---|

| Mezzi | Major U.S. brokerages, 401(k)s, IRAs, banks | Holdings-level across accounts | Limited | Yes |

| Empower | Major U.S. brokerages, banks, retirement accounts | Deep: sector, style, asset class | Limited | Yes |

| Kubera | Global banks, brokerages, crypto, DeFi | Mostly balance-level | Strong: real estate, private equity, collectibles | Yes, highly flexible |

| Quicken Simplifi | U.S. banks, brokerages, credit cards | Basic holdings view | Minimal | Limited |

| Monarch Money | Broad U.S. banking, credit card, loan, and investment coverage | Basic allocation view | Limited | Yes |

Mezzi uses read-only syncing across investment accounts. Kubera may stand out for households with international accounts, crypto, and private assets. Monarch Money covers a lot on the everyday banking side, though more manual categorization may be needed for complex investment setups.

Portfolio and tax insight

Aggregation only goes so far. The bigger question is whether the data may help you do anything with it.

Mezzi is the only tool in this group with cross-account tax-loss and wash-sale monitoring. Empower offers strong fee analysis and retirement modeling. Kubera, Quicken Simplifi, and Monarch Money provide basic portfolio visibility, but not lot-level detail or tax-action guidance.

| Tool | Unrealized gain/loss | Lot-level detail | Wash sale alerts | Asset-location guidance | Fee analysis |

|---|---|---|---|---|---|

| Mezzi | Yes | Yes | Yes, cross-account | Yes | Yes (X-Ray) |

| Empower | Yes | Limited | No | No | Yes (Fee Analyzer) |

| Kubera | Basic | No | No | No | No |

| Quicken Simplifi | Basic | No | No | No | No |

| Monarch Money | Basic | No | No | No | No |

Execution control vs. automation

After data quality, the next issue may be simple: does the tool just show information, or does it also support action?

Mezzi provides rebalancing guidance, flags harvesting opportunities, and notifies users when a wash-sale window clears, without placing trades. Empower’s optional advisory service may implement changes, though that may shift assets into managed accounts and away from self-directed control. Kubera, Simplifi, and Monarch surface information only.

| Tool | Read-only | Rebalancing alerts | Tax-action guidance | Managed advisory option | Trade execution |

|---|---|---|---|---|---|

| Mezzi | Yes | Yes | Yes | No | No |

| Empower | Yes | Yes | Limited | Yes | Via managed accounts only |

| Kubera | Yes | No | No | No | No |

| Quicken Simplifi | Yes | No | No | No | No |

| Monarch Money | Yes | No | No | No | No |

Pricing and incentives and business model

Once the feature set is clear, cost and incentives may decide whether the fit holds up over time.

Mezzi starts at $299/year and is an SEC-registered fiduciary with no AUM fees and no managed advisory path. Empower’s dashboard is free, but its revenue comes from a paid advisory service at 0.89% AUM. That may not make the dashboard less useful, though it may shape the sales path. Kubera and Monarch Money are subscription-only with no advisory upsell. Quicken Simplifi is the lowest-cost option for investors who mainly want budget-plus-portfolio visibility.

| Tool | Core cost (DIY use) | Paid advisory service | In-app advisory upsell | Fiduciary status |

|---|---|---|---|---|

| Mezzi | $299/year | None | None | Yes (SEC-registered RIA) |

| Empower | Free | Yes (0.89% AUM on first $1M) | Yes | Yes (for paid advisory clients) |

| Kubera | ~$249/year | None | None | No |

| Quicken Simplifi | $47.99–$71.88/year | None | None | No |

| Monarch Money | $99.99/year ($14.99/month) | None | None | No |

For self-directed investors, a tool may feel very different once the business model comes into view. Some tools are built to support oversight without a managed-advice path. Others may use a free dashboard as the front door to an advisory service. That distinction often shows up pretty fast in day-to-day use.

Pros and cons of each tool

The right pick may depend on what you care about most: tax-aware portfolio management, net worth tracking, or budgeting. This table keeps it simple by lining up each tool’s main strengths, limits, and the type of investor it may fit best.

| Tool | Pros | Cons | Best-fit investor |

|---|---|---|---|

| Mezzi | Read-only aggregation across brokerage, retirement, and taxable accounts; AI portfolio insights; tax-loss and wash-sale monitoring; X-Ray overlap analysis; flat $299/year fee | Users place all trades themselves; not designed for budgeting or bill tracking | Self-directed investors with multi-account portfolios who want tax-aware oversight without handing over control |

| Empower Personal Dashboard | Free dashboard; net worth and retirement readiness views; fee analysis tool | Paid advisory upsell; limited tax-lot or overlap diagnostics | Investors who want a free overview of net worth and retirement progress |

| Kubera | Broad coverage for global, crypto, and private assets; flexible manual entry; long-term net worth tracking | Minimal tax-aware analytics; no AI-driven guidance; not a budgeting tool | Self-directed investors with diverse or international holdings who prioritize asset tracking over portfolio optimization |

| Quicken Simplifi | Strong budgeting and cash flow management; strong mobile app; light investment tracking | Shallow investment features; limited tax-lot views; no overlap analysis | Budget-first households needing basic investment visibility |

| Monarch Money | Flexible household budgeting; flat subscription with household privacy controls; multi-aggregator sync | Limited investment analytics; no tax optimization or rebalancing guidance | Households wanting shared budgeting with basic portfolio visibility |

The tradeoff may come down to three things: portfolio depth, household budgeting, or broad asset coverage.

Conclusion

Choosing a wealth tracker usually comes down to two things: how complex your portfolio may be and how much control you may want to keep over portfolio decisions.

After comparing aggregation, tax insight, and control, the choice often comes back to portfolio complexity and how hands-on you may want to remain.

| Investor situation | Portfolio complexity | Best-fit tool |

|---|---|---|

| Simple portfolio, budgeting first, basic investment visibility | Low | Quicken Simplifi |

| Household dashboard, collaborative budgeting, clear multi-account tracking | Low–medium | Monarch Money |

| Growing portfolio with retirement and taxable accounts, fee and performance visibility | Medium | Empower Personal Dashboard |

| Multi-account DIY investor with a 401(k), Roth IRA, taxable account, and HSA who wants tax-aware analytics and AI guidance | Medium–high | Mezzi |

| Diverse holdings including crypto, international securities, or private assets | High | Kubera |

| You want managed investing instead of self-directed tracking | Any | Robo-advisor |

That may make the choice less about feature lists in the abstract and more about how you actually manage your accounts.

For self-directed investors with several account types, Mezzi may be the strongest fit in this group. For many people managing a 401(k), a Roth IRA, and one or more taxable accounts, the gap between seeing the data and knowing what to do next may be where Mezzi stands out. If you self-direct across multiple accounts, Mezzi may give you tax and allocation insight without taking control of your portfolio.

Choose the tracker that matches your account mix and the depth of analysis you want.

FAQs

How many accounts should I have before a wealth tracker is worth paying for?

A wealth tracker may be worth paying for once you have 2 or more accounts.

At that point, tools like Mezzi may offer more value through account aggregation, tax optimization, and overlap detection.

Can a read-only tracker help me avoid tax mistakes across multiple accounts?

Yes. A read-only tracker like Mezzi may help you avoid tax mistakes across multiple accounts by monitoring for wash sale risk, sending alerts, and helping you stay aligned with IRS rules.

It does this without requiring you to transfer funds.

What should I prioritize first: tax insights, budgeting, or net worth tracking?

For most self-directed investors in 2026, it may make sense to start with net worth tracking. That may give you a clearer baseline for your overall financial picture by showing assets, liabilities, and how things may change over time.

Then, some investors add tax insights as a way to look for ways to optimize long-term growth. Budgeting still matters, but it may be less urgent at the start if the main goal is understanding the full financial picture.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.