Equity pay may look simple at first. The tax date usually changes everything.

If I want the short version, here it is:

- RSUs are usually taxed when they vest

- ISOs may trigger AMT when exercised, even before a sale

- NSOs are usually taxed as ordinary income at exercise

- ESPPs let me buy through payroll deductions, often at up to a 15% discount, with tax treatment that may depend on how long I hold

That’s the whole game: when I get the shares, when tax may show up, and whether I need cash up front.

Some key points stand out fast:

- RSUs may feel simplest, but the common 22% federal withholding may be too low for higher earners

- ISOs may offer long-term capital gains treatment, but only if holding-period rules are met

- NSOs may require cash for both the strike price and the tax bill at exercise

- ESPPs may look low-friction, but basis reporting errors may lead to paying tax twice on the same income

- Option holders who leave a company may have only about 90 days to exercise vested shares before terms change or the option expires

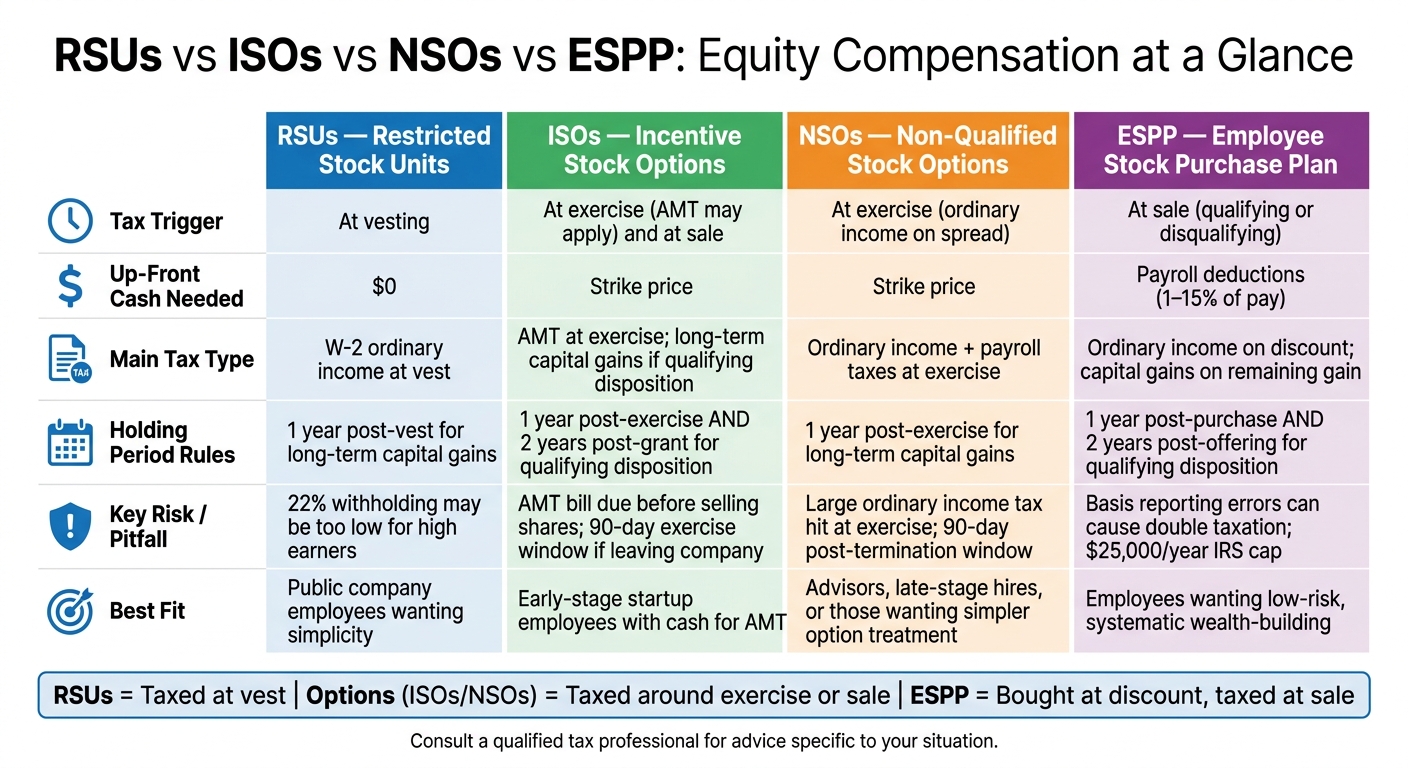

RSUs vs ISOs vs NSOs vs ESPP: Equity Compensation Comparison

Equity Compensation 101: How RSUs, ISOs, NSOs, and ESPP Plans Work

Quick Comparison

| Type | Main trigger | Up-front cash | Main tax issue | Main tradeoff |

|---|---|---|---|---|

| RSUs | Vesting | $0 | Value at vest may be taxed as W-2 income | Simplicity vs. concentration risk |

| ISOs | Exercise and sale | Strike price | AMT may apply at exercise | Tax upside vs. cash and holding risk |

| NSOs | Exercise | Strike price | Spread may be taxed as ordinary income | Flexibility vs. tax hit at exercise |

| ESPP | Purchase and sale | Payroll deductions | Discount may be taxed at sale | Discount vs. holding-period rules |

Put another way: RSUs = taxed at vest. Options = taxed around exercise or sale. ESPPs = bought at a discount, then taxed based on sale timing.

If I’m comparing them side by side, I’m usually looking at four things:

- Tax timing

- Cash needed

- Holding-period rules

- Risk from owning too much company stock

The article breaks down those tradeoffs in plain English, with examples, deadlines, and the tax forms that may come with each type.

1. RSUs

A Restricted Stock Unit (RSU) is a promise to give you company shares after you meet certain conditions, usually staying employed through the vesting date. No cash changes hands when the RSU is granted, and no tax is due at that point. RSUs are the simplest stock comp type: there’s no exercise step, just vesting and then the choice to sell or hold.

Vesting is the taxable event. When RSUs vest, the shares are deposited into your brokerage account. The fair market value (FMV) of those shares on the vesting date is taxed as W-2 wages. Many employers withhold 22% for federal taxes through a sell-to-cover process, where the company sells enough shares to cover withholding. For higher earners, that amount may not fully cover the total tax due.

After vesting, the shares are yours. Your cost basis is the FMV on the vesting date. If you sell later, any gain or loss above that vest-date FMV may be taxed as a short-term or long-term capital gain or loss, depending on how long you hold the shares after vesting.

| Event | When Tax Applies | Tax Type | Basis Used |

|---|---|---|---|

| Grant | Never | None | N/A |

| Vesting | Immediately | W-2 wages | FMV on vest date |

| Sale (≤1 year) | At sale | Short-term capital gain or loss | Sale price minus vest FMV |

| Sale (>1 year) | At sale | Long-term capital gain or loss | Sale price minus vest FMV |

The main choice usually comes down to this: sell at vesting, or keep the stock and stay exposed to your company’s share price. Some people treat vested RSUs like cash compensation and decide ahead of time how much to sell and how much company stock they may want to keep. Also worth noting: a loss sale within 30 days of vesting may trigger wash sale rules.

Unlike RSUs, ISOs and NSOs add an exercise step before you own the shares.

2. ISOs

Unlike RSUs, ISOs require cash up front. With an Incentive Stock Option (ISO), you get the right to buy company shares at a fixed strike price set on the grant date. That price must be at least equal to FMV at that time. Nothing shows up in your account on its own. You have to exercise the option and pay the strike price to receive shares.

ISOs often vest over four years with a one-year cliff. The first tax event usually happens when you exercise. At that point, no regular income tax may be due, but the spread may trigger AMT. For 2026, AMT rates are 26% on the first $239,100 of AMT income and 28% above that threshold. So you may owe cash taxes before selling a single share. In plain English: ISOs may create tax value on paper while still asking for cash out of pocket before any sale happens.

After exercise, the next issue is the holding period. A qualifying disposition means holding the shares for more than one year after exercise and more than two years after the grant date. Miss either test and it becomes a disqualifying disposition. So the choice may come down to this: exercise now, hold through stock-price risk, or sell earlier and give up part of the tax upside.

The tax gap between those paths may be large. Say you have 1,000 ISOs with a $20 strike price and you exercise when the stock is at $100. In a qualifying disposition - selling above $150 more than one year after exercise and two years after grant - the full $130,000 gain is taxed as long-term capital gain. In a disqualifying disposition, the $80,000 spread at exercise is ordinary income, and only the $50,000 gain above the exercise price gets capital gains treatment.

Two rules may push the timeline faster than people expect:

- The $100,000 rule: only $100,000 worth of ISOs, measured by strike price, may first become exercisable in one calendar year and still keep ISO treatment. Anything above that is treated as NSOs.

- If you leave the company, you often have just 90 days to exercise vested ISOs before they convert to NSOs.

That may mean coming up with cash for the exercise cost and possible AMT before any sale takes place.

| Event | Regular Income Tax | AMT |

|---|---|---|

| Grant | None | None |

| Vesting | None | None |

| Exercise | None | Taxed on spread (FMV − strike) |

| Sale (qualifying) | Long-term capital gain | None |

| Sale (disqualifying) | Ordinary income on spread | None |

3. NSOs

A Non-Qualified Stock Option (NSO) gives you the right to buy company shares at a set strike price. But the tax treatment may be tougher than with an ISO. And an NSO only has value if the stock price is above the strike price.

When you exercise, the spread between the strike price and the fair market value gets taxed as ordinary income. That amount may also be subject to payroll taxes like Social Security and Medicare. For some people, that tax bill may be large. Exercise may require cash for the share purchase and cash for taxes at the same time.

Employers usually withhold federal tax on NSO income at a flat 22% supplemental rate. For higher earners, that amount may be too low, so some people check their marginal rate and plan for estimated payments if needed.

After exercise, the FMV on that date becomes your cost basis. If the stock goes up after that, the extra gain may be taxed as capital gains. If you sell within one year, it may be taxed as short-term capital gains. If you hold for more than one year, it may qualify for long-term capital gains treatment.

That two-step setup is a big reason timing and cash planning get so much attention with NSOs.

A cashless exercise sells enough shares right away to cover the strike price and taxes. Some employees who feel strongly about the stock and have the cash to cover the upfront cost choose to exercise and hold. In that case, later growth may qualify for long-term capital gains rates if the holding period is long enough.

Most plans also give you a limited post-termination window to exercise vested NSOs before they expire. In many cases, that window may be about 90 days after you leave the company.

| Event | Tax Treatment |

|---|---|

| Grant | None |

| Vesting | None |

| Exercise | Ordinary income + payroll taxes on the spread (FMV − strike) |

| Sale (held ≤1 year) | Short-term capital gains on growth above exercise FMV |

| Sale (held >1 year) | Long-term capital gains on growth above exercise FMV |

ESPPs work differently: you buy shares through payroll deductions, usually at a discount.

4. ESPPs

Unlike options, ESPPs let employees buy shares through automatic payroll deductions, often at a discount. An Employee Stock Purchase Plan (ESPP) uses after-tax payroll deductions, usually between 1% and 15% of pay. You sign up during an enrollment window, pick a contribution rate, and the money builds up over a purchase period, which is often six months. At the end of that period, the plan uses the cash on hand to buy shares for you.

The big draw is the look-back provision. In many plans, the purchase price is based on the lower of the stock price at the start of the offering period or the stock price on the purchase date, and then the plan applies a discount of up to 15%. If the stock moves up during that window, the effective discount may end up being more than 15%. There’s also an IRS limit: total purchases are capped at $25,000 of stock per calendar year, based on fair market value at the start of the offering period.

Taxes depend on when the shares are sold. A qualifying disposition means you hold the shares for more than two years from the offering date and more than one year from the purchase date. In that case, only the lesser of the original discount or the actual gain may be taxed as ordinary income, and the rest may be taxed as long-term capital gains.

Sell before both holding periods are met, and it becomes a disqualifying disposition. Then, the full discount at purchase may be taxed as ordinary income. That leaves a fairly simple tradeoff: selling right after purchase may lock in the discount and may reduce the chance that the stock falls during the holding period. Holding longer may lead to better tax treatment on gains, but it also may add concentration risk, especially if you already hold company stock through RSUs or other equity.

One gut-check may help: if those shares were cash today, would you use that cash to buy the stock at the current price? If the answer is no, selling right away may make more sense for some people. Also, no tax is withheld at purchase, so you may want to keep cash available for the tax bill when you eventually sell.

Cost basis reporting is another place where people may get tripped up. Brokers often list only the discounted purchase price as your basis on Form 1099-B. If you don’t adjust that number upward to include the amount already taxed as ordinary income on your W-2, you may end up paying tax twice on the same gain. Form 3922 may help you track the right basis.

The discount may look like the headline feature. But taxes, liquidity needs, and concentration risk may matter just as much when deciding whether to sell or hold.

Taxes, Liquidity, and Planning Tradeoffs

Once you get past the mechanics, the tougher calls usually come down to taxes, cash flow, and concentration risk. That’s where the choice to sell, hold, or exercise may start to look less like a simple math problem and more like a tradeoff.

Tax Timing and Character

| Equity Type | When Ordinary Income Tax Is Due | Reporting Form | Later Gains |

|---|---|---|---|

| RSUs | At vesting | W-2; 1099-B | Short- or long-term capital gains on sale |

| ISOs | None at exercise; AMT may apply; qualifies for long-term capital gains if held one year from exercise and two years from grant | Form 3921; 1099-B; Form 6251 if AMT applies | Long-term capital gains if holding periods are met |

| NSOs | At exercise (spread taxed as W-2 income) | W-2; 1099-B | Short- or long-term capital gains on sale |

| ESPPs | At sale (discount portion is ordinary income) | Form 3922; W-2; 1099-B | Short- or long-term capital gains on sale |

These tax rules may shape the timing. In some cases, holding longer may change the tax character. In others, selling sooner may reduce complexity.

Liquidity and Cash Flow

| Equity Type | Cash Needed Up Front | Withholding Method | Main Cash Risk |

|---|---|---|---|

| RSUs | $0 | Sell-to-cover, usually 22% | Under-withholding for high earners |

| ISOs | Strike price | None at exercise | AMT bill due without selling shares |

| NSOs | Strike price | Cashless exercise or sell-to-cover | Tax owed at exercise on the spread |

| ESPPs | Payroll deductions (up to 15% of pay) | None at purchase | Lower take-home pay during the offering period |

Cash needs may shift the picture fast. RSUs and NSOs, for example, may look simple at first, but higher earners may still run into under-withholding risk.

Planning and Risk Tradeoffs

| Equity Type | Concentration Risk | Common Pitfall | Practical Strategy |

|---|---|---|---|

| RSUs | High if held after vesting | Under-withholding tax gap | Sell at vest; adjust W-4 |

| ISOs | Very high if held for long-term gains | AMT on income you have not turned into cash if the stock falls | Exercise in smaller batches to manage risk |

| NSOs | Moderate | Higher tax bracket from a large exercise | Exercise in lower-income years |

| ESPPs | Low if sold at purchase | Double taxation from incorrect basis reporting | Maximize contribution; sell right after purchase |

One theme shows up again and again: employer stock may pile up faster than people expect. If both your paycheck and a large part of your portfolio are tied to the same company, concentration risk may climb in a hurry.

That risk may matter even more with ISOs and RSUs, where the tax setup may tempt people to hold longer than they otherwise would.

Pros and Cons

Each equity type comes with its own tradeoff. The better fit may depend less on which one sounds better on paper and more on your situation - how much cash you may have available, how long you may stay at the company, and how much admin and tax complexity you may be willing to deal with.

At a high level:

- RSUs may be the simplest to manage

- ISOs may be the most tax-sensitive

- NSOs may be the most straightforward option type

- ESPPs may work well for steady, payroll-based buying

This table lines up each type against cash needs, tax complexity, and holding period.

| Equity Type | Key Pros | Key Cons | Best-Fit Situation |

|---|---|---|---|

| RSUs | Simple; no strike price; value tracks the stock price directly | Ordinary income tax at vesting; no control over timing; concentration risk if held | Public company employees who want simplicity and predictable value |

| ISOs | Potential for long-term capital gains treatment; no ordinary income tax at exercise | AMT exposure; rigid holding periods; shares can expire worthless; $100,000 annual vesting cap | Early-stage startup employees with high upside and enough cash and patience to manage AMT |

| NSOs | No AMT risk; flexible timing; available to consultants and advisors; no $100,000 cap | Spread taxed as ordinary income at exercise; requires cash unless cashless exercise is used | Late-stage hires, advisors, or employees who want simpler option treatment |

| ESPPs | Built-in 15% discount plus lookback; limited downside if sold quickly; systematic wealth-building | Reduces monthly take-home pay during offering period; capped at $25,000 per year; disposition rules add complexity | Employees who want a low-risk way to build wealth and can handle the payroll reduction |

The details below explain the day-to-day tradeoff behind each row.

RSUs are simple and often liquid, but taxes may hit at vesting. The IRS flat withholding rate of 22% may leave a gap for people in the 32%–37% bracket.

ISOs may lead to the best tax result in some cases, but that result may depend on holding through AMT, timing risk, and concentration risk.

NSOs are simpler than ISOs, but exercising may trigger ordinary income tax on the spread.

ESPPs are less complex than options and come with a built-in discount through payroll deductions. Selling right after purchase may lock in the discount and may limit concentration risk.

Conclusion

Start by identifying your equity type. RSUs vest on their own, options need to be exercised, and ESPPs purchase stock through payroll deductions. Once that part is clear, timing becomes the next thing to sort out.

Review your grant agreement and plan document. Confirm the vesting schedule, strike price, and option expiration dates. Most options expire 10 years after the grant date. If you leave the company, you may have about 90 days to exercise vested options before that window closes.

After that, look at the tax dates. For ISOs and ESPPs, confirm the holding periods before selling, since those dates may affect the tax rate that applies. For RSUs and NSOs, check whether 22% withholding may cover your tax bracket, because higher earners may owe more at tax time.

Then step back and look at your full exposure. Add up your employer stock across all accounts. At many tech companies, equity may make up a large share of total compensation. That may leave you with a lot tied to one stock, especially when your income may already depend on the same employer.

Before exercising, selling, or continuing to hold, some people confirm their tax treatment with a qualified tax professional. Mezzi is designed to let you connect all your accounts in one place so you may track exposure, concentration risk, and planning opportunities.

FAQs

How do I know which equity type I have?

Check your official grant documents, such as your stock option agreement or equity award letter. Those documents should list the equity type - RSUs, ISOs, NSOs, or ESPP - along with details like vesting, strike price, and expiration date.

You may also find the same info in your company’s equity portal. If anything still feels unclear, your company’s HR or stock administration team may be able to share a summary of your grants.

Should I sell my shares right away or hold them?

It may depend on your risk tolerance and tax approach.

For RSUs, some people treat them like a cash bonus. The idea is pretty simple: if you may not choose to put that same amount into your company’s stock today, selling right away may be one way to diversify.

For ISOs, holding shares may open the door to long-term capital gains treatment. But that same move may also increase AMT exposure and leave you more concentrated in one stock. If someone decides to hold, they may do it in a steady, rules-based way and plan ahead for the tax impact.

What happens to my options if I leave my job?

When you leave your job, unvested RSUs are usually forfeited right away.

With ISOs and NSOs, you may get a post-termination exercise window based on your company’s plan. That window often ranges from 90 days to 10 years.

For ISOs, the special tax treatment may be lost if the options aren’t exercised within 90 days after you leave. That’s one reason many companies use the shorter window.

If your options are underwater, they may expire worthless.

Disclosures:

This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Before making decisions regarding equity compensation, consult a qualified tax or financial professional to understand your specific situation.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.