Miss the Form 706 filing, and the unused federal estate tax exclusion may be lost. That is the short version.

If I boil this down, portability may let a surviving spouse use a deceased spouse’s unused federal estate and gift tax exclusion. But that transfer only may happen if the estate files Form 706 and makes the election on time. In 2026, the federal exclusion is listed as $15,000,000 per person, and the federal estate tax rate may reach 40% in some cases.

Here’s the plain-English version:

- DSUE means the unused exclusion of the spouse who died first

- Portability is not automatic

- Form 706 may need to be filed even when no estate tax may be due

- The usual deadline may be 9 months after death

- A 6-month extension may be requested with Form 4768

- Some smaller estates may get a late-election path for up to 5 years

- Remarriage may change which DSUE a surviving spouse may use

- GST exemption does not transfer

- State estate tax rules may differ from federal rules

- Bad valuations, missing gift history, or late filing may cut the DSUE amount or wipe it out

What Is DSUE (Deceased Spousal Unused Exclusion)? - Wealth and Estate Planners

Quick comparison

| Topic | Basic rule |

|---|---|

| What portability does | May transfer a deceased spouse’s unused exclusion to the survivor |

| What triggers it | A timely, complete Form 706 |

| Standard deadline | 9 months from date of death |

| Extension option | Up to 15 months from death with Form 4768 |

| Late-election relief | Some estates may use Rev. Proc. 2022-32 within 5 years |

| Who may use DSUE | A surviving spouse, if legal requirements are met |

| Remarriage effect | Only the last deceased spouse’s DSUE may apply |

| GST exemption | Not portable |

| Inflation treatment | DSUE stays fixed after transfer |

| Main risk | No filing or an incomplete filing may mean permanent loss |

The article below may make sense if I want the short answer first: DSUE may be worth preserving, but the filing rules, deadlines, and valuation details may decide whether it survives at all.

Who qualifies for DSUE

Once the basic portability rule is on the table, the next issue is simpler: who may actually use the transferred exemption?

Three rules set the limits. The deceased spouse must have died on or after Jan. 1, 2011. The deceased spouse also must have been a U.S. citizen or resident at the time of death. And the surviving spouse must still be living when the DSUE is used.

A noncitizen surviving spouse generally may not use DSUE unless a treaty applies or the spouse later becomes a U.S. citizen. If assets pass through a QDOT, DSUE may be calculated, but that amount may change until the trust ends or citizenship is obtained.

There’s also the last deceased spouse rule. This is where remarriage may change the picture. If a surviving spouse remarries and that later spouse dies, the later spouse’s DSUE may replace the earlier one. DSUE does not stack across spouses, so each later death may reset the amount available to the surviving spouse.

When Form 706 is required versus filed only to elect portability

Eligibility only matters if the estate files on time and includes the needed records.

Estates above the 2026 federal filing threshold of $15,000,000 must file Form 706 and meet full valuation rules across all assets. Estates below that threshold have no legal duty to file. But if the goal is to elect portability and keep the DSUE, a timely, complete Form 706 is still the only path.

For estates filing only to elect portability, good-faith estimates may be used for some marital and charitable deduction property, unless that property is part of a formula bequest that affects other heirs. That carveout may sound minor, but it matters. A late filing, or missing valuation detail, may permanently block the DSUE election.

When portability helps and when it falls short

Portability may matter most when the surviving spouse’s estate is likely to grow over time. A concentrated stock position, appreciating real estate, or a closely held business may push an estate past the individual exclusion later on.

There’s also a timing edge here. DSUE is used before the surviving spouse’s own exemption, which may leave the surviving spouse’s inflation-indexed exclusion untouched for later use. That matters because DSUE is a fixed dollar amount and does not adjust for inflation.

Still, portability has gaps.

- The GST exemption is not portable, so if it goes unused at the first death, it is lost.

- Many states with their own estate taxes do not recognize federal portability, so a surviving spouse may still face a state estate tax bill.

Those gaps may reduce what heirs receive even when federal DSUE is preserved. Portability may help, but it does not replace a broader estate plan.

If DSUE is available and worth preserving, the next step is filing Form 706 correctly and before the deadline.

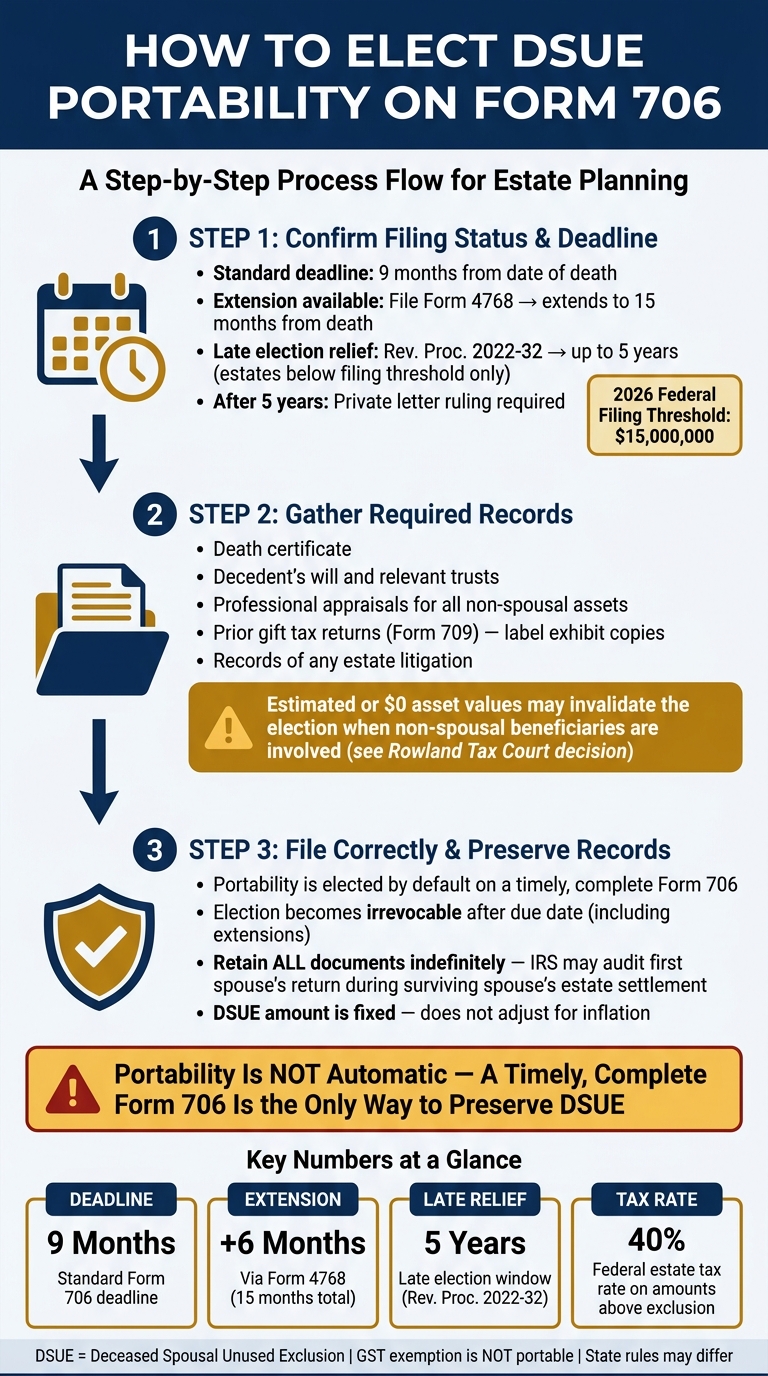

How to elect portability on Form 706 without missing the deadline

Estate Tax Portability: DSUE Election Steps & Deadlines

Making the portability election may sound simple on paper. In practice, the timing and paperwork may make all the difference. A late filing or an incomplete return may put DSUE at risk.

Step 1: Confirm filing status and the correct deadline

Start with the deadline first. That tells you whether the estate may file in the usual way or may need to rely on a late-election path.

Estates may be required to file when the gross estate plus adjusted taxable gifts exceeds the filing threshold. Estates below that threshold may not need to file for estate tax liability, but Form 706 still may be used to elect portability.

The standard due date is nine months from the date of death. An estate may file Form 4768 by the original due date to extend the Form 706 deadline to 15 months from death.

If the estate was below the filing threshold, Revenue Procedure 2022-32 may allow a late portability election within five years of death. In that case, the return needs the required late-filing notation at the top of Form 706. After that five-year window, the estate generally may need a private letter ruling.

Once that filing window is sorted out, the next step is pulling together the records behind the return.

Step 2: Gather the records needed to prepare a complete return

The estate may need the death certificate, the decedent's will and relevant trusts, professional appraisals, records tied to any litigation involving the estate, and copies of previously filed gift tax returns, Form 709. If a prior Form 709 is attached, write "THIS PREVIOUSLY FILED FORM IS AN EXHIBIT TO FORM 706" at the top.

Those records may support the DSUE amount and may matter later if the IRS reviews the surviving spouse's future estate.

Simplified valuation applies only to assets passing entirely to a spouse or charity. It does not apply when the value affects what other beneficiaries receive. So if a trust uses percentage-based distributions for non-spousal beneficiaries, the return may still require full itemization and fair market value figures.

The Tax Court's Rowland decision shows why that matters. Estimated values may wipe out the DSUE election when full valuation is required.

Step 3: File correctly and keep the surviving spouse's records

After the return is ready, the last part is filing it the right way and keeping the paper trail.

On a timely filed Form 706, portability applies unless the executor opts out. The return still needs to be complete.

After filing, keep every document indefinitely. The election becomes irrevocable after the due date passes, including extensions. The IRS may examine the first spouse's return later to verify the DSUE amount, even after the statute of limitations has expired, when the surviving spouse's estate is eventually settled. That means the surviving spouse may need these records many years later to support the DSUE amount.

Mistakes that can reduce or permanently eliminate DSUE

Once the filing steps are clear, the next risk is losing DSUE through avoidable mistakes. Families may lose DSUE because of filing errors, and every dollar lost may face a 40% federal estate tax when the surviving spouse dies. The result may be permanent and costly.

Deadline, valuation, and gift-history errors that cause the biggest problems

The biggest mistake is assuming portability happens automatically. It does not. Portability requires a timely Form 706, even when no estate tax may be due.

Valuation mistakes are another major trouble spot. Assets such as concentrated stock positions, private business interests, and real estate need defensible fair market values when any part of the estate passes to non-spousal beneficiaries. Estimated figures or $0 values on asset schedules may make the return incomplete and may put the election at risk. A recent Tax Court case shows that estimated values may jeopardize the election when nonspousal beneficiaries are involved.

Leaving prior taxable gifts off Form 709 creates a third layer of risk. DSUE is calculated by subtracting lifetime taxable gifts and the taxable estate from the deceased spouse's exclusion amount. If prior gifts are missing, the DSUE figure may be wrong, and the IRS may correct it years later when reviewing the surviving spouse's estate, even after the statute of limitations on the first estate has expired.

Under the last deceased spouse rule, remarriage may also change what remains available. A surviving spouse may only use the DSUE from their most recently deceased spouse. If a second spouse dies with a smaller unused exclusion, the first spouse's DSUE is replaced by the second spouse's amount. In cases where remarriage may be likely, some people use the first DSUE sooner through lifetime gifts because a later spouse's DSUE replaces it.

Common portability mistakes, their impact on DSUE, and how to avoid them

These mistakes tend to fall into a few repeatable categories.

| Mistake | Impact on DSUE | Preventive Steps |

|---|---|---|

| Assuming portability is automatic | Permanent DSUE loss | File Form 706 within 9 months of death, even if no tax is owed |

| Missing the 9-month deadline | Loss of the election unless IRS relief applies | File Form 4768 for an automatic 6-month extension; use Rev. Proc. 2022-32 if within 5 years of death |

| Using estimated or $0 asset values | Return incomplete; election at risk | Obtain professional appraisals for assets passing to non-spousal beneficiaries |

| Omitting prior taxable gifts | IRS may reduce DSUE at surviving spouse's estate review | Review all prior Forms 709 before filing Form 706 |

| Misreading remarriage rules | First spouse's DSUE replaced by second spouse's DSUE | Some people use the first DSUE through lifetime gifting before a second spouse dies |

| Missing the 5-year safe harbor | Late election unavailable after five years | Track the 5-year window under Rev. Proc. 2022-32 for estates not otherwise required to file |

These errors show why portability may need to sit inside a broader estate plan.

How portability fits into a broader estate and tax plan

Portability may help, but it rarely stands in for a full estate plan. DSUE is a fixed dollar amount. It’s locked in based on the value calculated on the date of the first spouse’s death, and asset growth later on may leave the surviving spouse’s estate above the exemption threshold.

There’s also a key rule that tends to matter in gift planning. If a surviving spouse makes a taxable gift, the IRS requires the DSUE to be used first, before the survivor’s own basic exclusion amount. That setup may preserve the survivor’s own exclusion for later.

This is one reason some families pair portability with trust planning instead of relying on portability by itself. A credit shelter trust (CST) may cover gaps that portability does not. Assets placed in a CST may grow outside the surviving spouse’s taxable estate, while DSUE shields only a fixed amount no matter how much those assets later appreciate. The GST tax exemption is not portable. If it goes unused at the first death, it’s gone for good. And in many states that impose estate taxes, federal portability may not be recognized at all.

That’s why a full look at net worth may matter before deciding whether filing Form 706 is worth the cost. For some families, that filing may look like a formality. For others, it may end up being the thing that keeps later planning options open.

Conclusion: The deadlines, documents, and decisions that matter most

The main issue isn’t whether portability exists. It’s whether portability, by itself, may be enough. Form 706 is the election point, and missed deadlines may still be fatal to the election. A timely filed return, along with accurate asset valuations, is what makes the election stick.

In cases involving appreciating assets, GST planning, state estate taxes, or the chance of remarriage, portability alone may fall short. Some families use DSUE, a credit shelter trust, or a mix of both, often with help from a qualified estate attorney or tax professional.

FAQs

How much tax could portability save my family?

Portability may preserve a deceased spouse’s unused federal estate and gift tax exemption, often called DSUE. For some families, that may mean a much larger amount passes to heirs without federal estate or gift tax.

Here’s the basic idea: if the 2026 exemption is $15,000,000 per person, a surviving spouse who elects portability may be able to protect up to $30,000,000. If portability isn’t elected, that unused exemption may be lost.

That’s why portability often comes up in estate planning conversations. It may let a married couple use both spouses’ exemptions, instead of leaving part of one spouse’s exemption on the table.

Should most surviving spouses file Form 706 anyway?

Yes. For many surviving spouses, filing a timely, complete Form 706 may be the only way to preserve the deceased spouse’s unused federal estate and gift tax exemption (DSUE) for later use, even when the estate may be below the federal filing threshold.

Portability is not automatic. If the election is not made, the DSUE may be lost permanently.

When is a trust better than portability alone?

A trust may make more sense than portability alone if the goal includes using GST tax exemption, because that exemption may not transfer between spouses through portability.

A trust may also offer more control over distributions. It may keep the deceased spouse’s assets outside the surviving spouse’s taxable estate. And in more complicated family situations - or if the surviving spouse may remarry - it may add another layer of protection, since portability applies only to the last deceased spouse.

Disclosures:

• This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

• Tax laws and exemption amounts are subject to change. Readers should consult a qualified estate attorney or tax professional for advice specific to their situation.

• Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.