A SLAT may let a married couple move future asset growth outside the taxable estate while keeping some indirect access through the other spouse. In 2026, the federal estate and gift tax exemption may be $15 million per person and $30 million per married couple, with a 40% federal estate tax rate above that level. For couples with stock, business interests, or real estate that may grow over time, this type of trust may be one way to use exemption now and shift later growth out of the estate.

Here’s the short version:

- One spouse puts assets into an irrevocable trust for the other spouse

- The transfer may use lifetime gift and estate tax exemption

- Future growth on those assets may stay outside the grantor’s estate

- The spouse who benefits from the trust may receive distributions, which may create indirect household access

- The setup may carry tradeoffs, including loss of control, divorce or death risk, and reciprocal trust doctrine issues if both spouses create near-match trusts

- Asset choice matters: growth assets, business interests, and income-producing property may be used more often; IRAs and 401(k)s usually do not fit

- The gift generally must be reported on IRS Form 709 by April 15 of the next year

A simple example: a $5 million transfer that grows to about $8.95 million over 10 years at 6% may move about $4 million of later growth outside the estate. At a 40% estate tax rate, that growth alone may be tied to about $1.6 million in estate tax that may no longer apply.

| Topic | What the article covers |

|---|---|

| Main tax idea | Use exemption now and move later growth outside the estate |

| Access | Indirect access through distributions to the spouse |

| Best-fit assets | Growth stock, private business interests, real estate, liquid assets |

| Poor-fit assets | Retirement accounts like IRAs and 401(k)s |

| Main risks | Irrevocability, no direct control, spouse death, divorce, mirror-trust risk |

| Filing | Form 709 and, in some cases, appraisal support |

If you’re trying to judge whether a SLAT may fit, the core question may be simple: after moving assets into an irrevocable trust, may enough liquidity stay outside the trust for taxes, spending, and surprises? That’s the lens this article uses.

SLAT Asset Suitability & Tax Benefit Overview

SLATs Explained: The Pros and Cons of Spousal Lifetime Access Trusts w/ Blake McKibbin

How a SLAT Works and What Assets Typically Fund It

Once the tax goals are clear, the next step may be choosing assets and control terms that make the SLAT work.

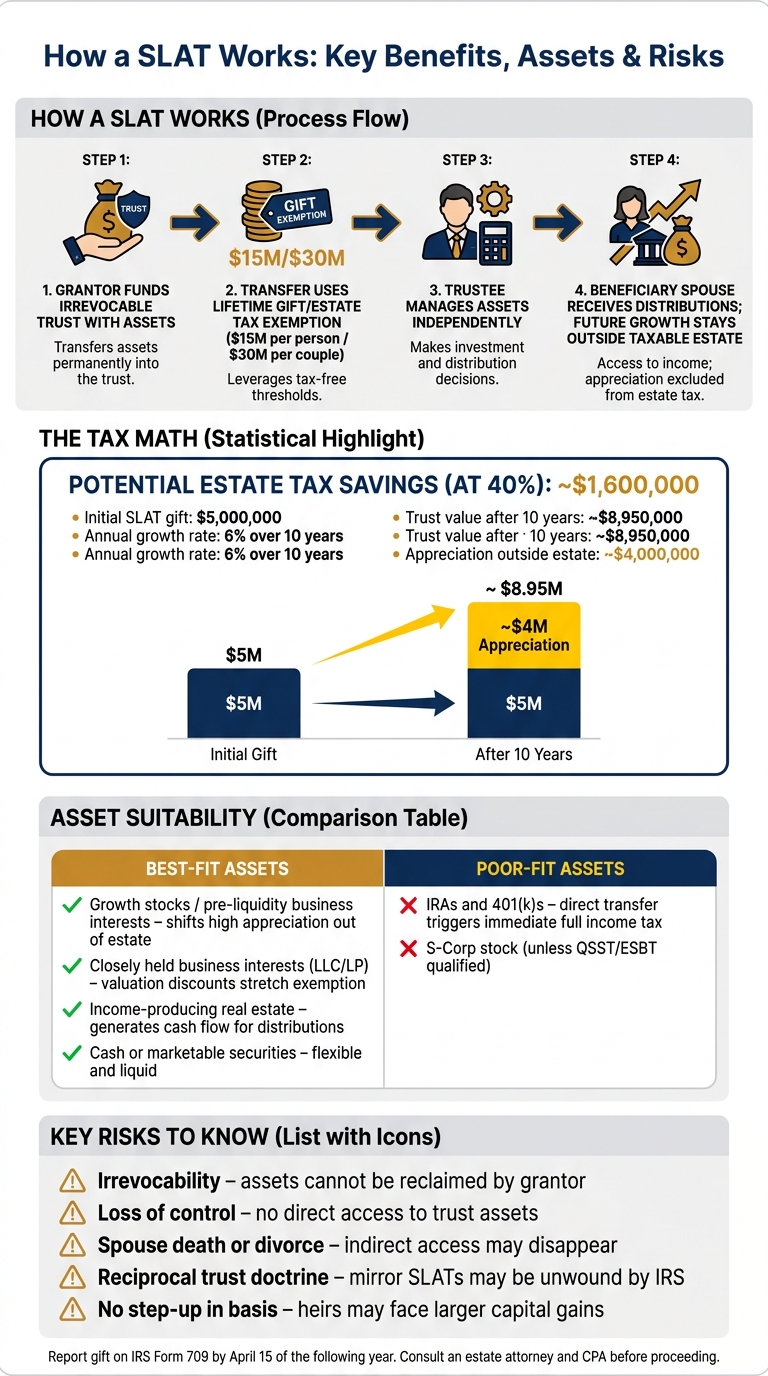

A SLAT is an irrevocable trust. That irrevocability is the whole point. It may make the transfer a completed gift, use lifetime exemption, and keep future appreciation outside the grantor's estate. If the grantor retains access, IRC Sections 2036 and 2038 may pull the assets back into the estate.

The Key Parties: Grantor, Beneficiary Spouse, Trustee, and Descendants

Four parties make a SLAT function. The grantor funds the trust with separate property and gives up direct control. The beneficiary spouse may receive distributions under the trust terms. The trustee manages the assets and decides when and how much to distribute. The descendants - usually children - are named as remainder beneficiaries, meaning they receive what’s left after the beneficiary spouse passes.

An independent or corporate trustee - someone who is neither the grantor nor the beneficiary spouse - may reduce control risk and may allow broader discretionary powers, while also helping avoid IRS challenges tied to retained control.

That trustee setup is what may let the beneficiary spouse create indirect access without giving the grantor direct control.

How Indirect Access Works Without Direct Ownership

The grantor may not receive distributions directly, but the beneficiary spouse may support shared household spending. When the beneficiary spouse receives distributions for shared household expenses or lifestyle needs, the grantor may benefit from those same dollars. That’s the core appeal of a SLAT.

Choosing Assets That Create the Most Tax Leverage

The best assets to fund a SLAT are usually the ones that may grow a lot after the transfer date. Because the gift is valued at the time of transfer, any appreciation after that point may escape estate tax. That may make growth stocks, pre-liquidity business interests, and other closely held business interests strong candidates.

Closely held interests in LLCs or limited partnerships may be especially powerful because they may qualify for valuation discounts due to lack of control and lack of marketability. That may stretch how far the lifetime exemption goes.

Income-producing assets - such as rental real estate or dividend-paying securities - may also work well because they generate cash flow the trustee may use to make distributions to the beneficiary spouse. Cash or marketable securities offer flexibility and liquidity, which may make them straightforward funding choices when other assets carry more complexity.

Avoid retirement accounts. Transferring an IRA or 401(k) directly into a SLAT triggers immediate income tax on the entire balance. These accounts are usually better handled through beneficiary designations.

| Asset Type | Suitability | Why It Works |

|---|---|---|

| Growth stocks / pre-liquidity business interests | Excellent | Shifts high appreciation out of the estate at today's value |

| Closely held business interests (LLC/LP) | Strong | Valuation discounts stretch the lifetime exemption |

| Income-producing real estate | Strong | Generates cash flow for spousal distributions |

| Cash or marketable securities | Strong | Flexible, liquid, and straightforward to transfer |

| Retirement accounts (IRA/401(k)) | Poor | Direct transfer triggers immediate full taxation |

Note on S-Corp stock: Transferring S-Corp shares into a SLAT may terminate the S-election unless the trust qualifies as a Qualified Subchapter S Trust (QSST) or Electing Small Business Trust (ESBT).

Those asset choices directly affect how much gift and estate tax benefit the SLAT may produce - the subject of the next section.

The Gift and Estate Tax Benefits a SLAT Can Provide

Once a SLAT is funded, the tax angle may come down to two ideas: freezing today's value and moving later growth outside the taxable estate. In plain English, the assets transferred into the trust are generally measured at the time of the gift. If those assets grow later, that added value may remain in the trust instead of flowing back into the grantor's estate.

Locking In Lifetime Exemption Before the Law Changes

Funding a SLAT uses some or all of the donor spouse's federal lifetime gift and estate tax exemption. In 2026, that exemption is $15,000,000 per individual or $30,000,000 for a married couple, after the One Big Beautiful Bill Act kept the higher exemption amounts in place and indexed them for inflation.

The transfer is generally reported on Form 709 by April 15 of the following year. If the gift includes closely held business interests or real estate that needs an appraisal, a qualified appraisal is typically attached to support the reported value and start the IRS statute of limitations.

Keeping Future Appreciation Out of the Taxable Estate

This is where the math may get interesting. The gift is valued when it is transferred. Growth after that point may stay outside the donor's estate on a permanent basis.

A $5 million SLAT gift growing at 6% annually for 10 years becomes about $8.95 million. That leaves roughly $4 million of appreciation outside the estate. At a 40% federal estate tax rate, that may translate to about $1,600,000 in tax savings from appreciation alone.

The longer the time horizon, and the faster the assets grow, the more this structure may matter. Pre-IPO stock, early-stage equity, and growth-oriented real estate are often seen as strong candidates because earlier funding may lock in a lower value for estate tax purposes.

Grantor Trust Status, Valuation Discounts, and Two-Spouse Planning

Most SLATs are set up as grantor trusts. In that arrangement, the donor spouse pays the income tax on the trust's earnings from their own assets. That setup may let the trust grow with less income-tax drag, and it may also reduce the amount that is later subject to estate tax in the donor spouse's estate.

That same idea may become more useful when the gifted asset qualifies for a discount. If a SLAT is funded with interests in a family LLC, limited partnership, or closely held business, valuation discounts for lack of control and lack of marketability may apply. That may let the donor transfer more underlying economic value while using less of their lifetime exemption.

Some couples with large estates create two separate SLATs - one funded by each spouse - to use both spouses' exemptions. Two SLATs may increase the tax upside, but the next issue is whether the setup holds up under reciprocal-trust scrutiny.

The Tradeoffs, Risks, and Situations Where a SLAT Can Backfire

A SLAT may produce strong tax savings, but those benefits may only hold up if the trust also works for the couple's day-to-day life. That's the hard part. The tax upside may come with a plain tradeoff: giving up control.

Loss of Control and the Real Cost of Irrevocability

A SLAT is irrevocable. That means the donor gives up ownership, control, and flexibility. In practical terms, the donor may not keep meaningful authority over the trust without creating estate-inclusion risk. The trust also needs its own EIN, separate accounts, and separate tax filings.

Assets in a SLAT usually do not receive a step-up in basis at the donor's death, which may leave heirs with larger capital gains later.

That loss of control may hit hardest when the beneficiary spouse's situation changes.

What Happens If the Beneficiary Spouse Dies, Divorces, or Gets Smaller or Discretionary Distributions

Access may disappear if the beneficiary spouse dies or if distributions become narrower. If the couple divorces, a former spouse may keep benefiting from the trust unless the document includes a divorce-trigger clause. Even in a stable marriage, the trustee may limit distributions, which may make access far tighter than expected.

Because of that, some families only fund a SLAT with assets they may be prepared to live without. Detailed cash-flow modeling over 20 to 30 years of retirement spending, taxes, and surprise expenses may take place before any transfer is made.

The Reciprocal Trust Doctrine and How to Structure Two SLATs Safely

For couples using two SLATs, one of the bigger risks may come from making the trusts too similar. Mirror-image SLATs may be vulnerable. The two trusts need differences in timing, trustees, distributions, assets, and beneficiaries. If the IRS finds the trusts too similar to treat them as separate, the tax benefits may unwind.

| Structuring Difference | How to Apply It |

|---|---|

| Staggered Timing | Fund in different tax years or months apart |

| Different Distribution Standards | HEMS for one; broad discretion for the other |

| Different Trustees | Individual trustee for one; corporate for the other |

| Different Assets | Real estate in one; securities or business interests in the other |

| Different Beneficiary Classes | Include different descendants or add other family members to only one trust |

The next step may be to test these risks against the couple's full balance sheet and cash flow before any transfer.

How to Evaluate a SLAT Using Complete Financial Data and Where Mezzi Fits

Why You Need a Full Financial Picture Before Gifting Millions

After looking at control and reciprocity risk, the last big check is simpler: may the couple fund a SLAT without putting pressure on day-to-day liquidity?

Before any transfer, it may make sense to map the full household balance sheet, projected spending, debt, and liquidity needs. That usually means looking across taxable accounts, retirement accounts, business equity, real estate, insurance, and compensation tied to future growth. For people who hold concentrated or high-growth assets, this step may matter even more.

A SLAT may look good on paper, but the household still needs enough assets outside the trust to cover spending, taxes, debt, and surprises. If that part is fuzzy, an irrevocable transfer may add risk instead of reducing it.

How Mezzi Can Help You Frame the Asset and Tax Decisions

Once the balance sheet is clear, the next step may be getting the data into a format your estate team may actually use.

Mezzi provides fiduciary-grade portfolio visibility across taxable accounts, retirement plans, employer stock, and private investments. For SLAT planning, Mezzi's X-Ray analysis may surface concentrated positions and overlapping exposures, identify which assets may carry the most appreciation potential, and flag low-basis holdings that may involve a lost step-up at death.

It may also model the liquidity tradeoff by showing what the balance sheet may look like after a hypothetical transfer. That may give the household and its advisors a way to test whether enough assets may remain outside the trust to support spending needs.

Mezzi organizes the data. Your estate attorney drafts the trust, and your CPA files Form 709.

Conclusion: When a SLAT Makes Sense and When to Hold Off

A SLAT may fit best when a couple has taxable estate exposure, strong outside liquidity, and assets with meaningful future appreciation. In other cases, holding off may make more sense.

The right SLAT depends on full visibility into assets, cash flow, and spending needs. Without that clarity, an irrevocable transfer may introduce more risk than it removes. The wrong assets or timing may erase the planning benefit.

FAQs

Who should consider a SLAT?

A Spousal Lifetime Access Trust may be most relevant for high-net-worth married couples whose assets approach or exceed the federal estate and gift tax exemption of $15 million per person. In some cases, it may reduce a future taxable estate while still preserving indirect access through a spouse.

It may be a fit for couples who hold growth assets, such as pre-IPO stock, closely held businesses, real estate, or marketable securities. Because the trust is irrevocable, it may be better suited to couples with a stable marriage who are comfortable giving up direct control and who may not need the transferred assets for day-to-day living expenses.

How much liquidity should remain outside a SLAT?

Keep enough liquid assets outside a SLAT to support your standard of living without depending on trust distributions.

Because assets moved into a SLAT are irrevocable, they generally may not be taken back if your financial situation changes. Before funding the trust, make sure you may still support your current and future lifestyle with assets that remain outside it.

Can a SLAT reduce both gift and estate taxes?

Yes. A SLAT may reduce both by moving assets into an irrevocable trust, using the donor spouse’s federal gift tax exemption, and removing those assets - and any future appreciation - from the taxable estate.

The donor spouse’s payment of income taxes on trust earnings may also further reduce the taxable estate without triggering additional gift taxes.

Disclosures:

• This content is for informational purposes only and does not constitute investment, tax, or legal advice. Consult your own attorney, tax advisor, or financial professional before making any decisions regarding trusts or estate planning.

• Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

• Savings and performance examples are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.