A high income may shorten the path to early retirement, but stock-heavy pay may make the path less simple. If I earn $350,000 to $600,000+ in big tech, FIRE may depend less on earning more and more on three things: cash flow control, tax planning, and limiting employer-stock risk.

Here’s the short version:

- I may have a FIRE path in 10 to 15 years if my savings rate stays high.

- That path may get off track if too much of my net worth sits in one company’s stock.

- RSUs may be taxed at vest, even if I keep the shares.

- RSU withholding may fall short for high earners, which may leave a large tax gap by April.

- A taxable account may matter for spending before age 59½.

- A scattered setup across a 401(k), HSA, Roth IRA, ESPP, and brokerage may make it harder to track overlap, lot-level taxes, and stock concentration.

What this article gets right is simple: FAANG FIRE may be less about income and more about building rules. Some households base spending on salary, treat RSUs and bonuses as savings fuel, keep a tax reserve, sell stock at vest, and use account order with the goal of lowering tax drag.

If I boiled it down even more, the framework may look like this:

- Control lumpy pay

- Limit single-stock exposure

- Use tax-advantaged accounts first

- Keep enough taxable money for early retirement

- Track everything in one place

A quick side-by-side may make the point clearer:

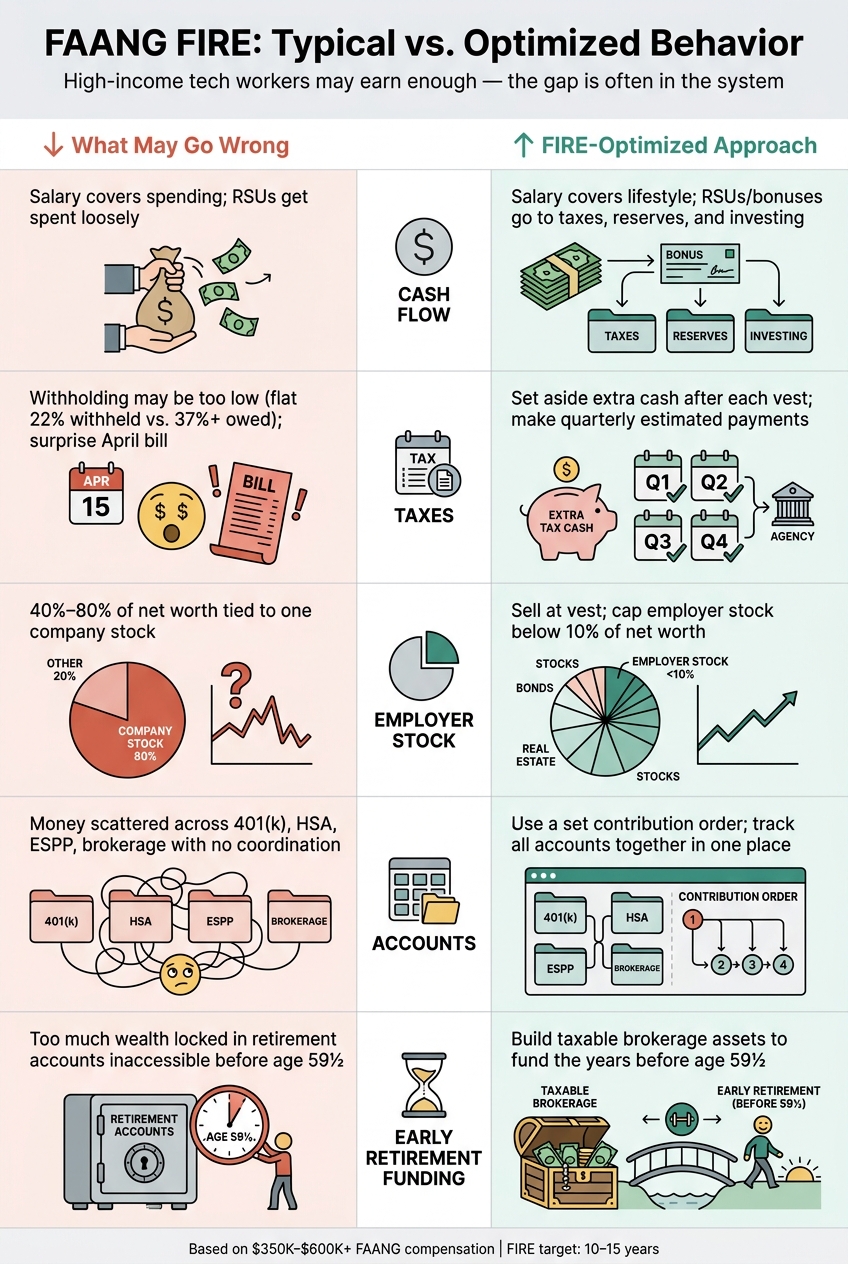

| Area | What may go wrong | What some people do instead |

|---|---|---|

| Cash flow | Salary covers spending, while RSUs get spent loosely | Salary may cover lifestyle; RSUs/bonuses may go to taxes, reserves, and investing |

| Taxes | Withholding may be too low | Some set aside extra cash after each vest and make estimated payments |

| Employer stock | Net worth may get tied to one company | Some sell at vest and cap employer stock at a small share of net worth |

| Accounts | Money sits across many platforms with little coordination | Some use a set contribution order and track all accounts together |

| Early retirement funding | Too much wealth stays in retirement accounts | Some build taxable assets for the years before 59½ |

That’s the core idea: early retirement in big tech may come down to a system, not just a paycheck.

FAANG FIRE: Typical vs. Optimized Behavior Across 5 Key Areas

He Turned His FAANG Salary into Early Retirement - Andre Nader

How FAANG Compensation Gets in the Way of FIRE

FAANG FIRE may break down less from low income than from timing. Salary, bonus, RSUs, and ESPP proceeds arrive on different schedules, face different tax rules, and land in different accounts. Salary and bonus are taxed as ordinary income when paid. RSUs are taxed at vest. ESPP discounts and gains are taxed based on whether the sale is qualifying or disqualifying. That mix may create three problems: cash-flow shocks, tax drag, and concentration risk.

RSU withholding also may come up short versus actual tax owed. Employers often withhold at a flat 22% supplemental rate, but many senior tech workers may fall into the 37% federal bracket. In California, combined federal and state tax may go above 50%. The gap may not show up until April.

Scattered accounts add another layer of friction. A 401(k), Roth IRA, HSA, and taxable brokerage spread across firms may look diversified on the surface. But that setup may hide overlap, skew net worth tracking, and make tax-aware moves harder to time. It may also mask how much employer stock runs through the full portfolio.

Cash flow shocks, tax drag, and employer-stock concentration

These three problems may stack on top of each other. Uneven cash inflows may leave cash-flow gaps. Heavy employer-stock exposure may add risk without extra expected return. And split-up accounts may make it harder to see the whole picture or act at the right time.

A side-by-side comparison makes the mismatch easier to spot.

| Feature | Typical FAANG Behavior | FIRE-Optimized Behavior |

|---|---|---|

| Stock concentration | Accumulates RSUs; 40%–80% of net worth in one stock | Sells at vest; employer stock stays below 10% of net worth |

| Tax planning | Reactive; large surprise bill each April | Proactive; quarterly estimated payments, tax-loss harvesting, and optimal asset location |

| Account usage | Maxes pre-tax 401(k) only | Maxes 401(k), HSA, Backdoor Roth IRA, and Mega Backdoor Roth |

| Cash flow | Relies on monthly salary; RSUs are treated as extra | Uses a liquid reserve bucket to bridge gaps between vest dates |

That concentration risk may become more serious when employer stock drops while both compensation and portfolio value fall at the same time. For many people, fixing those three problems may start with a system for lumpy pay, not just a higher savings rate.

Build a FIRE System Around Lumpy Pay

Lumpy pay needs structure, not willpower. The goal is to route uneven compensation through the same system before spending happens, so RSUs and bonuses may turn into more steady FIRE progress. That usually means a rules-based cash flow setup, not monthly self-control.

Set up cash buckets before money disappears into spending

Run every dollar through fixed buckets. Taxes and savings get funded first. Spending gets what’s left.

A simple starting point is to split spending money from tax money and investment money. Some households use RSU proceeds to steady day-to-day spending while salary covers tax-advantaged accounts.

| Cash Bucket | Purpose | Target Size | Recommended Vehicle |

|---|---|---|---|

| Operating Cash | Monthly bills and spending | 1 month of expenses | Checking account |

| Emergency Fund | Job loss or major surprise | 3–12 months of expenses | HYSA or money market |

| Bridge Reserve | Covers salary shortfall from maxing 401(k) | One vest cycle plus buffer | Short-duration Treasury ETF (e.g., SGOV) |

| Tax Reserve | Covers RSU/bonus withholding gap | The gap between withholding and your actual tax bill | HYSA or Treasury fund |

| Taxable brokerage | Early retirement funding | Remainder of net RSU/bonus | Taxable brokerage (index funds) |

The tax reserve may deserve extra attention. Setting aside the withholding gap after each vest may reduce the odds of an April surprise.

Set a realistic FIRE number and savings rate for a high-cost lifestyle

The 25x rule may be a useful starting point, but high-cost households may need a larger target.

For a household spending $150,000 per year, that works out to about $3.75 million at a 4% withdrawal rate and about $5 million at a 3% withdrawal rate. Many early retirees prefer a 3% to 3.5% withdrawal rate for a 40-plus-year horizon.

One rule of thumb some households use: base lifestyle spending on base salary only. In that setup, bonuses and RSUs are treated more like savings fuel than spendable income. For households trying to keep a high-cost lifestyle in early retirement, saving 25% or more of gross income may be part of the picture.

Once cash flow is ring-fenced, new savings may be directed by account priority.

The right account contribution order for big-tech workers

The order below is designed for high-income tech workers who want to put tax-free and tax-deferred compounding ahead of taxable-account funding.

| Priority | Account | 2026 Limit | Why It Matters |

|---|---|---|---|

| 1. Employer match | 401(k) | Varies | Immediate 100% return on contributions |

| 2. 401(k) deferral | Pre-tax or Roth 401(k) | $24,500 | May reduce taxable income or lock in tax-free growth |

| 3. HSA (if eligible) | Health Savings Account | $4,400 (individual) / $8,750 (family) | Triple-tax advantage: deductible, grows tax-free, withdraws tax-free for medical |

| 4. ESPP shares | Stock purchase plan | $25,000 (pre-discount) | Capture the 15% discount, then sell quickly |

| 5. Mega Backdoor Roth | After-tax 401(k) + in-plan conversion | Up to $72,000 total | Large lever for tax-free compounding |

| 6. Backdoor Roth IRA | Traditional → Roth conversion | $7,500 | Tax-free growth for earners above Roth income limits |

| 7. Taxable brokerage | Individual or joint account | No limit | Liquidity for early retirement before age 59½ |

Across multiple accounts, some investors place higher-growth assets in Roth accounts, bonds in pre-tax accounts, and broad index funds in taxable accounts to reduce tax drag.

Before counting on the Mega Backdoor Roth, verify that your 401(k) plan supports after-tax contributions and in-plan Roth conversions. Not every employer plan allows it. It may also make sense to confirm whether your employer offers a match true-up if you front-load contributions early in the year, since missing that detail may mean fewer match dollars in later pay periods.

Cut Stock Risk and Tax Drag Without Losing Control

The next issue is the stock itself. Many FAANG employees may hold a large share of their net worth in employer stock. That may create single-stock risk, especially when the same company also pays their salary. One way some people handle this is with a written selling policy and a tax-aware diversification plan.

Write a policy for RSUs, ESPP, and concentration limits

A written policy may make it easier to avoid holding on for "just a little longer." A common guideline is to cap employer stock at 10% to 15% of net worth. Anything above 20% to 25% may be viewed as an unacceptable level of risk, especially if income is tied to the same company.

The table below offers a simple framework for when some people may act:

| Employer Stock % of Net Worth | Risk Level | Recommended Action |

|---|---|---|

| < 10% | Low to Moderate | Monitor closely; consider trimming |

| 10%–20% | High | Sell new vests and trim older lots |

| 20%+ | Unacceptable | Trim aggressively |

RSUs vest as ordinary income, so some people sell at vest unless they have a specific reason to hold.

For ESPP shares, the math may look a bit different. A qualifying disposition - holding more than two years from the grant date and more than one year from the purchase date - may lower taxes. But if diversification is the priority, selling right away still locks in the 15% discount as near-certain profit.

For insiders, or for anyone who tends to second-guess these calls, a Rule 10b5-1 plan may put selling on autopilot. It is pre-scheduled, works within blackout-window rules, and removes in-the-moment decision-making.

Once the selling rule is in place, the next step may be deciding which lots to sell and how to limit extra tax drag.

Tax-aware selling, loss harvesting, and withdrawal planning

Selling with a plan may matter as much as selling on a regular basis. When trimming older lots with embedded gains, specific identification (SpecID) lets you choose which shares to sell. That may mean picking high-basis lots to reduce taxable gains, or selecting loss lots to harvest.

Tax-loss harvesting may offset gains from stock sales. But there’s a catch: wash sale rules apply across all accounts. If a lot is sold at a loss and a substantially identical security is bought within 30 days before or after in another account, the loss is disallowed. That approach only works when every account is tracked together.

Brokers may report RSU and ESPP cost basis as $0, or only the purchase price, on Form 1099-B. Manually adjusting Form 8949 to reflect ordinary income already taxed on the W-2 may prevent tax from being paid twice on the same dollars.

Taxable brokerage may fund the gap to age 59½. In lower-income years, tax-gain harvesting may help. That may involve selling appreciated assets at the 0% long-term capital gains rate, which applies to taxable income up to $98,900 for married filing jointly in 2026.

Equity compensation strategies compared side by side

No single approach fits every case. The table below compares the main options across the factors that often matter most for FIRE planning:

| Strategy | Concentration Risk | Tax Complexity | Liquidity | FIRE Effect |

|---|---|---|---|---|

| Immediate sale (sell-at-vest) | Lowest; instant diversification | Low; taxed as ordinary income at vest | High; cash available immediately | Provides stable, diversified growth |

| Staged sale | Moderate; reduces risk over 2–3 years | Moderate; requires tracking lots across years | Moderate; tied to schedule | Balances tax drag with market risk |

| Hold-and-monitor | Highest; full single-stock exposure | Low to high | Low; capital locked in stock | Can derail FIRE if stock drops sharply |

| Donate appreciated shares | Low; removes position | High; requires itemization or a DAF | None; assets go to charity | Best for those with philanthropic goals |

For many FAANG workers, sell-at-vest plus staged diversification of older lots may be the default path. Exchange funds may fit rare, long-horizon cases. They may not fit early-retirement liquidity needs.

The remaining challenge may be keeping those rules visible across every account and tax lot.

Use Mezzi to Track the Full Plan and Stay on Course

After you set account priorities and stock-sale rules, one risk still tends to stick around: losing sight of the whole picture across too many logins. A FAANG pay package may stretch across payroll, a 401(k), an HSA, an ESPP, and a stock plan portal. When everything sits in different places, concentration creep may be easier to miss. Cross-account wash-sale conflicts may slip by too.

Get a full view of net worth, overlap, and tax opportunities across all accounts

Mezzi connects those accounts with read-only access, so your full household balance sheet may be visible in one place. It may flag concentration creep, surface tax-loss opportunities throughout the year, and flag potential wash-sale conflicts around new vests and recent sales.

The X-Ray feature scans ETFs, mutual funds, and individual positions to show hidden overlap. If the same fund appears in your 401(k) and taxable account, X-Ray shows that overlap. It also shows how much of your net worth may sit in employer stock.

Mezzi is an SEC-registered fiduciary and does not execute trades or move money. It surfaces opportunities; you execute the trades.

Use ongoing AI-driven check-ins instead of one-time planning

That kind of visibility may matter most when vesting, bonus timing, or a job change shifts your tax picture. A one-time financial plan may go stale fast when RSU vesting schedules change, bonuses vary, or income drops sharply after leaving a company. Mezzi's AI-driven check-ins work from your actual connected balances, not hypothetical inputs typed into a form.

You may ask a specific question - whether a Roth conversion may fit your first year after leaving big tech, or whether your account locations may still reduce tax drag - and get an answer in minutes based on real data. Some people use those check-ins to adjust selling, tax, and account-location decisions as balances change.

Conclusion: Disciplined Systems, Lower Tax Drag, and Full Visibility Are the Shortest Path to FAANG FIRE

FIRE may be within reach for high-income tech workers, but the path may take more than a high salary. It may involve turning lumpy, multi-source compensation into a repeatable cash-flow system, managing employer stock with intent before concentration becomes too high, placing assets in the right account types with the goal of reducing lifetime tax drag, and tracking all of it across the full household balance sheet as the plan changes.

Those parts may not work well on their own. The cash-flow system depends on knowing what's already in each account. The selling policy depends on knowing what share of net worth may already be in employer stock. The tax strategy depends on seeing every lot, every account, and every upcoming vest at the same time. The plan may work best when the full balance sheet stays visible.

That's the practical case for full-portfolio visibility - and why the tools and systems used to track the plan may matter as much as the plan itself.

The tax and legal information in this article is general educational content for U.S. readers. It is not personalized tax or legal advice. Outcomes depend on your individual tax situation, account details, and market performance. Mezzi is an SEC-registered fiduciary that provides fiduciary advice and insights but does not execute trades, move money, or prepare tax returns. Consult a qualified tax professional for advice specific to your circumstances.

FAQs

How much taxable money do I need before retiring early?

Start with your FI number: multiply your expected annual expenses by 25, based on a 4% withdrawal rate. Some early retirees use 3% to 3.5% instead, which may mean a larger nest egg.

Include healthcare, housing, and taxes. While high-income earners may pay 25% to 35% in taxes during their working years, tax-efficient withdrawals and account management may lower that to 10% to 15%.

Should I sell my RSUs as soon as they vest?

Usually, yes. For many people, the rational default may be to sell RSUs when they vest.

Here’s the key point: RSUs are generally taxed as ordinary income at vesting whether you sell the shares or keep them. So once they vest, holding the stock may be an active choice, not a passive one.

Keeping the shares may also increase concentration risk. Your income and employee benefits may already be tied to your employer, and holding more company stock may add to that exposure.

A simple way some people think about it:

If you would not buy your company’s stock with your own cash today, sell and diversify.

That framing may help separate habit from intent. Instead of asking, “Should I keep what I already have?” it may be more useful to ask, “Would I choose to buy this stock right now with new money?” If the answer may be no, selling may be the cleaner move.

How do I avoid a big tax bill from RSUs and bonuses?

First, some people start by maxing out tax-advantaged accounts like a pre-tax 401(k), HSA, and, if available, a mega backdoor Roth. Doing that may lower taxable income and may improve tax efficiency.

For RSUs, taxes are generally due when they vest, so that bill may not be avoidable. Selling shares right away may reduce concentration risk. If shares are held, capital gains taxes may apply later. In some cases, tax-loss harvesting or donating appreciated shares may help offset taxes.

Disclosures:

• This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

• Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

• Registration does not imply a certain level of skill or that the SEC has approved the company or its services.

• The tax and legal information in this article is general educational content for U.S. readers. It is not personalized tax or legal advice. Outcomes depend on your individual tax situation, account details, and market performance. Consult a qualified tax professional for advice specific to your circumstances.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.