An ILIT may keep life insurance out of your taxable estate only if you give up all control over the policy. That usually means the trust owns the policy, the trustee runs it, premium payments move through the trust, and any transferred policy may need to clear the 3-year rule under IRC §2035.

Here’s the short version:

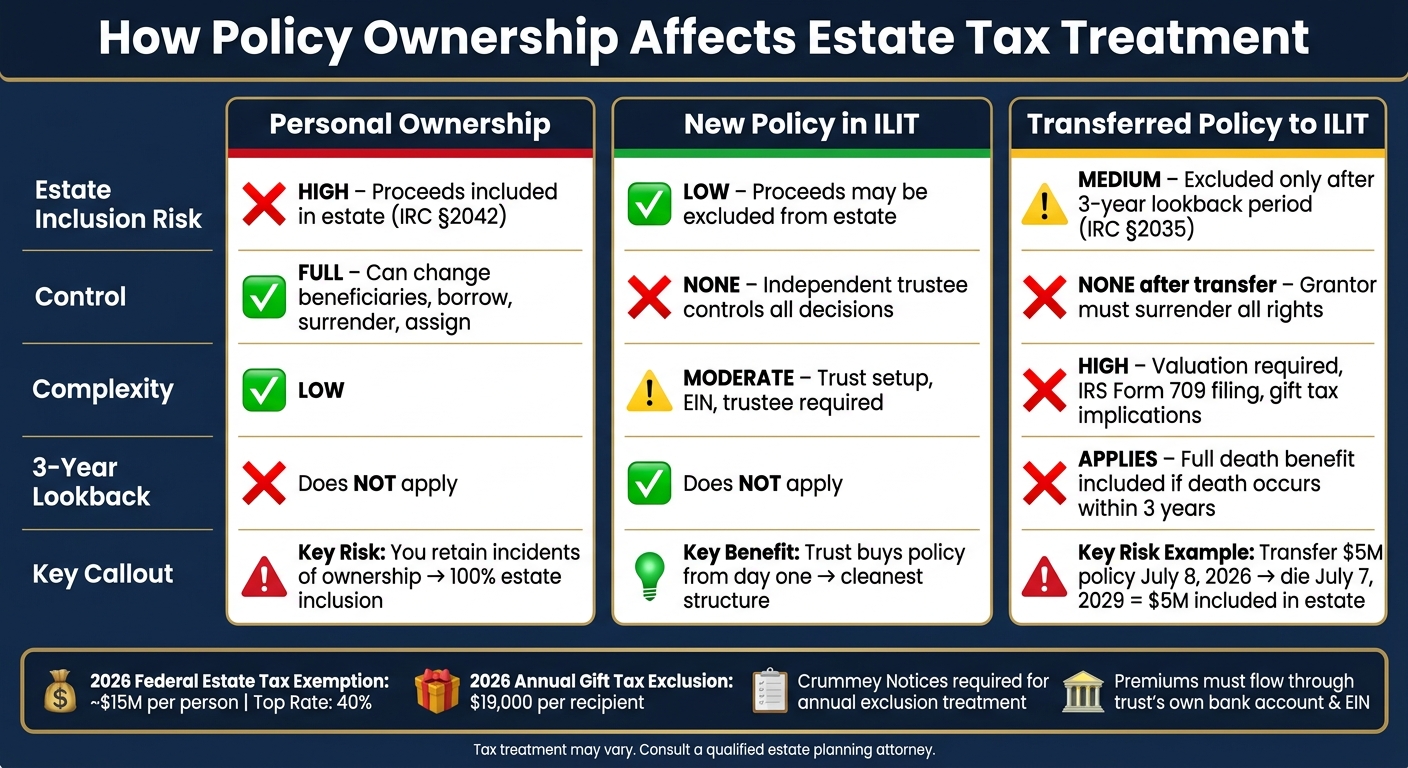

- If you own the policy, the death benefit may be included in your estate under IRC §2042

- If a new policy starts inside the ILIT, estate inclusion risk may be lower

- If you transfer an existing policy, the death benefit may still be included if you die within 3 years

- Premium gifts may need Crummey notices if the goal is annual exclusion treatment

- In 2026, the federal estate tax exemption is about $15 million per person, with a top rate of 40%

- In 2026, the annual gift tax exclusion is $19,000 per recipient

- ILIT setup and admin may add costs, paperwork, and loss of access to policy value

This comes down to one question: Have you fully given up ownership rights, or not? If not, the tax result may not change.

| Setup | Estate tax treatment may look like | Main risk |

|---|---|---|

| Personal ownership | Proceeds may be included in estate | You still control the policy |

| New policy owned by ILIT | Proceeds may stay outside estate | Setup and admin errors |

| Existing policy transferred to ILIT | May stay outside estate after 3 years | Death during 3-year lookback |

If I were summarizing the whole article in one line, I’d put it this way: an ILIT may work, but only if ownership, timing, and paperwork all line up.

Irrevocable Life Insurance Trusts: Do You Really Need an ILIT?

What an ILIT does and how ownership changes the tax result

ILIT vs. Personal Ownership vs. Transferred Policy: Estate Tax Comparison

An ILIT owns the policy, so the death benefit may pass through the trust instead of your estate. But that result may hinge on one thing: whether the insured gave up control.

The control test: what the insured must give up

The IRS looks at control, not just title. Under IRC Section 2042, if the insured holds any ownership right at death, the full death benefit may be pulled back into the taxable estate.

That means giving up every ownership right, including the right to change beneficiaries, borrow against the policy, surrender it, assign it, or pledge it. An independent trustee handles policy administration, premium payments, and communication with the insurance carrier.

That shift in control marks the line between personal ownership and ILIT ownership.

Personal ownership vs. ILIT ownership vs. transferred policy

| Feature | Personal Ownership | New Policy in ILIT | Transferred Policy to ILIT |

|---|---|---|---|

| Estate Inclusion Risk | Included in estate if you own it | Excluded if the trust buys it | Potentially included for 3 years after transfer |

| Control | Full (can change beneficiaries, borrow) | None (trustee controls) | None (grantor must surrender) |

| Complexity | Low | Moderate (trust setup required) | High (valuation & gift tax filings) |

| 3-Year Lookback | N/A | Does not apply | Applies (IRC §2035) |

How the policy gets into the trust may shape the tax result. A new policy bought inside the ILIT may avoid transfer risk. An existing policy may still work, but the three-year rule may pull the proceeds back into the estate.

Two ways to place a policy in an ILIT

ILIT funding usually comes down to two setups: buy the policy inside the trust, or move an existing policy into it. That starting point may shape the tax treatment.

New policy inside the trust: the cleaner structure

This route is usually the cleaner fit for the control test. If the ILIT buys a brand-new policy directly, the insured never owns it in a personal capacity, which may avoid transfer risk.

The order of steps matters here. The trust agreement should be drafted first, and the trustee must get an EIN before applying. After that, the trustee - not the insured - applies as the owner and beneficiary from day one. Once the policy is issued, the trustee should request written confirmation from the insurer showing that the trust is the sole owner and beneficiary.

This setup works only if the trust owns the policy from day one.

Transferring an existing policy: useful, but exposed to the three-year rule

The tradeoff here is timing risk, not ownership confusion. An existing policy may be assigned to the ILIT, but that transfer starts the three-year clock under IRC Section 2035.

That three-year period starts when the transfer is complete. Here’s why that timing may matter: if you transfer a $5 million policy to an ILIT on July 8, 2026, and die on July 7, 2029, the full $5 million may be included in your taxable estate. If you survive until July 9, 2029, the proceeds may be excluded.

Moving an existing policy may also trigger a gift tax event based on the policy’s value. That may require filing IRS Form 709 and may use part of your lifetime gift tax exemption.

Once ownership is settled, premium funding becomes the next failure point.

Funding premiums correctly and avoiding mistakes that undo the strategy

Premium gifts, annual exclusion treatment, and Crummey notices

After the trust owns the policy, the next place things may go off track is funding.

A common setup may look like this: cash is gifted to the ILIT's bank account, Crummey notices are sent, the withdrawal period runs for about 30 to 60 days, and only then is the premium paid from the trust.

Crummey powers may turn what would otherwise be a future-interest gift into one that may qualify for the annual exclusion. For 2026, that exclusion is $19,000 per recipient.

The details matter here. Different funding methods may lead to different tax treatment:

- If the insured pays the insurer directly, estate inclusion risk may increase

- If gifts are made without Crummey notices, they may use lifetime exemption

- If funding goes through Crummey notices, it may qualify for the annual exclusion, but notices and a waiting period are still part of the process

There’s also a limit that may trip people up. If a gift in a given year goes over the five-and-five limit - the greater of $5,000 or 5% of trust assets - the withdrawal right may stay open into later years.

Common mistakes that bring the death benefit back into the estate

The biggest risk is control.

Under IRC §2042, if the insured keeps the power to change beneficiaries, borrow against cash value, or cancel the policy, those rights may count as incidents of ownership. If that happens, the death benefit may be brought back into the taxable estate.

Premium payments may create problems too. Instead of paying the insurer from a personal account, the payment may need to come from the trust’s separate bank account and use the trust’s own EIN. That may sound picky, but this is one of those areas where paperwork and process may matter as much as intent.

Skipping Crummey notices may also create issues. So may paying the premium before the withdrawal window ends. In either case, annual exclusion treatment may be lost.

Even if the premium funding is handled cleanly, the trust may still need to justify the added cost and the fact that the insured gives up control.

When an ILIT fits, when it does not, and the key takeaways

Who is a good candidate for an ILIT

Once the mechanics are clear, the next step is simpler: Are the tradeoffs worth it?

An ILIT may fit households with estates near or above the federal exemption, especially when life insurance may push the estate deeper into taxable territory. At a 40% federal estate-tax rate, a $3 million policy may create up to $1.2 million of federal estate-tax exposure before exemptions.

That kind of tax impact may matter most when the policy is large enough to change the estate-tax outcome. Business owners, people in second marriages, and families with heirs who may need managed distributions often use ILITs for that reason. The trust may control the policy and may also control how the proceeds are paid out. Creditor protection may come with that setup, but it is usually a side effect rather than the main reason for using it.

The current exemption is temporary. If it drops to about $7 million per person, more estates may need this kind of planning.

Put plainly, an ILIT may make sense when the possible tax savings are large enough to offset the loss of access and the added admin work.

When an ILIT may not be worth the tradeoffs

The same rules that may create the tax benefit also create the friction.

If your total estate - including the death benefit - may sit well below the federal exemption, and you live in a state with no estate tax, the setup may not justify the cost or the extra moving parts. Setup often starts at about $5,000 in legal fees, and annual trustee and admin fees often run about 0.5% to 1.5% of trust assets.

An ILIT may also be a poor fit if you may need the policy’s cash value later for retirement, business liquidity, or collateral. There usually isn’t an easy exit if family circumstances shift, such as a divorce or a falling out with a beneficiary.

Conclusion: the rules that matter most

An ILIT may work only when ownership, control, and funding are handled with precision. The trust must be irrevocable. The trustee must own and control the policy. Transferred policies must outlast the three-year lookback under IRC §2035. Premium gifts must move through the trust’s own bank account, and Crummey notices must be issued and honored before the premium is paid.

An ILIT is a legal and tax structure, not just an insurance wrapper. The drafting, funding, and administration all need to line up.

FAQs

Do I lose all access to the policy in an ILIT?

Yes. Once an ILIT is set up and funded, you generally give up control of the policy and access to it.

Because the trust is irrevocable, you usually can't change its terms, take the policy back, or borrow against its cash value for your own use. The trustee, not you, controls the policy. If you keep that control, the IRS may include the death benefit in your taxable estate.

Who should serve as trustee for an ILIT?

The grantor generally may not serve as trustee of their own ILIT. If the grantor keeps control, or retains any incidents of ownership, the life insurance proceeds may be pulled back into their taxable estate. The grantor’s spouse also generally may not be a good fit for this role.

In many cases, an independent trustee may be preferred. That may include a corporate trustee or a trusted friend. The idea is simple: put someone in place who may handle premium payments, keep records, and send Crummey notices without tying that control back to the grantor.

Can an ILIT help with state estate taxes too?

Yes. An ILIT may also help reduce state estate taxes, since some states have estate tax thresholds that are lower than the federal exemption.

If you own the policy, the proceeds are generally included in your gross estate. That may push your estate above a state's threshold. When ownership is moved to an ILIT, those proceeds may be removed from your taxable estate, which may reduce state-level estate tax exposure.

Disclosures:

• This content is for informational purposes only and does not constitute investment, tax, or legal advice. Please consult your own tax, legal, or financial advisor regarding your specific situation.

• Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.