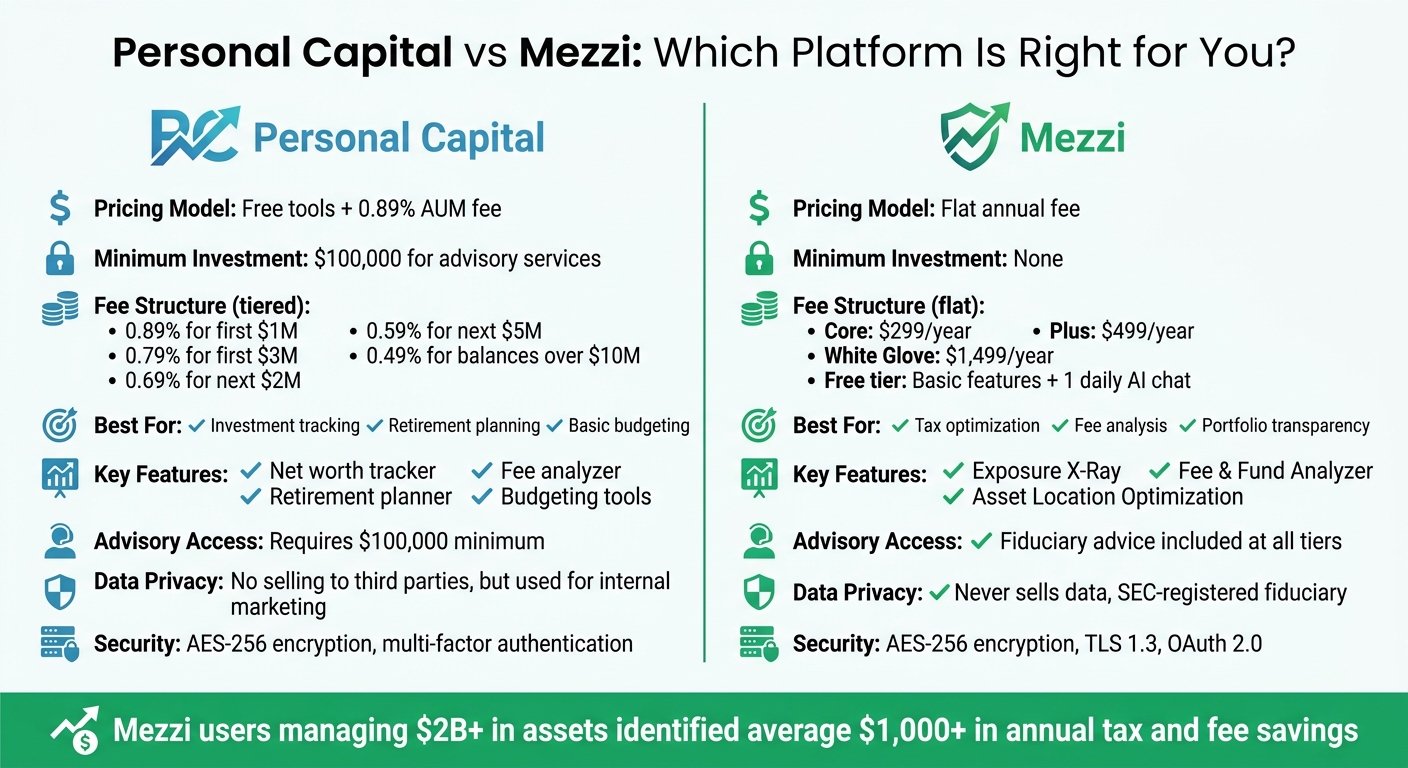

Personal Capital, now part of Empower, offers free financial tools like investment tracking and retirement planning. However, these tools are designed to encourage users to opt for its wealth management services, which charge an annual fee starting at 0.89% of assets under management (AUM) for portfolios of $100,000 or more. While the free tools provide insights like fee analysis and portfolio tracking, users may experience frequent upselling efforts.

For a simpler pricing model, Mezzi charges a flat annual fee ranging from $299 to $1,499, regardless of portfolio size. Mezzi focuses on tax optimization, fee analysis, and portfolio transparency, offering AI-driven insights without percentage-based fees or upselling. Both platforms prioritize data security but differ in their approach to pricing and services.

Key Takeaways:

- Personal Capital's free tools come with a focus on upselling wealth management services (minimum $100,000 investment, 0.89% AUM fee).

- Mezzi charges a fixed fee ($299–$1,499 annually) for all users, emphasizing transparency and fiduciary-level advice.

- Personal Capital is better for basic budgeting and retirement planning, while Mezzi caters to users seeking in-depth portfolio analysis and tax strategies.

Quick Comparison:

| Feature | Personal Capital | Mezzi |

|---|---|---|

| Pricing | Free tools + 0.89% AUM fee (min. $100,000) | Flat fee: $299–$1,499/year |

| Best For | Investment tracking, retirement planning | Tax and fee analysis, portfolio clarity |

| Advisory Access | Requires $100,000 minimum | Included at all tiers |

| Privacy | Data used for internal marketing | No data selling, SEC-registered fiduciary |

Personal Capital vs Mezzi: Pricing and Features Comparison

1. Personal Capital

Pricing Model

Personal Capital follows a freemium approach, offering free financial tools to draw users in, while promoting its paid wealth management services. To access these advisory services, users need at least $100,000 in investable assets. The annual fee for these services starts at 0.89% of assets under management for the first $1 million. For those with larger portfolios, the fee structure becomes tiered: 0.79% for the first $3 million, 0.69% for the next $2 million, 0.59% for the next $5 million, and 0.49% for balances exceeding $10 million. High-net-worth clients in the Private Client tier also gain access to dedicated advisors and estate planning services.

Features and Tools

The free tools provided by Personal Capital are quite extensive. They include:

- Net Worth Tracker: Offers real-time monitoring of assets and liabilities.

- Budgeting and Transaction Categorization: Automates budget tracking and organizes transactions.

- Retirement Planner: Runs simulations to gauge retirement preparedness.

- Investment Checkup Tool: Evaluates portfolio allocation and compares performance against benchmarks.

- Fee Analyzer: Highlights hidden fees in 401(k) plans, which could add up to as much as $155,000 over a lifetime.

Additionally, the platform offers Personal Capital Cash, a high-yield account with no minimum balance requirement. Notably, account links are read-only, ensuring that funds cannot be moved through the Personal Capital dashboard.

Advisory Services

For users who meet the asset threshold, Personal Capital provides access to financial advisors, tailored portfolio management, and tax-loss harvesting software. Each advisor typically handles around 200 clients, offering a mix of personalized guidance and portfolio oversight.

Privacy and Data Usage

Personal Capital has a clear stance on data security and usage. While it does not sell user data to third parties, it uses financial information internally to promote advisory services offered by its parent company, Empower. However, some users have reported that wealth advisors accessed their account data during complimentary consultations without prior consent. On the security front, the platform employs AES-256 encryption, multi-factor authentication, and a security bounty program to identify and address vulnerabilities. These measures reflect an emphasis on safeguarding user information while integrating it into their broader business strategy.

Personal Capital Review: Is It Worth the Hassle?

2. Mezzi

Mezzi takes a straight-shooting approach when it comes to pricing and transparency, offering clear membership options without hidden fees.

Pricing Model

Mezzi follows a flat annual fee structure with three membership tiers: Core ($299), Plus ($499), and White Glove ($1,499) per year. There’s also a free tier that provides basic account aggregation and one daily AI chat session.

What’s unique about this pricing model is that the fee remains the same no matter the size of your portfolio - whether you’re managing $100,000 or $10 million. This flat-rate approach lays the foundation for Mezzi’s suite of tools and privacy-focused services.

Features and Tools

Mezzi connects to over 10,000 financial institutions, pulling data from brokerages like Fidelity and Vanguard, along with 401(k)s, IRAs, and even cryptocurrency accounts. Among its standout tools are:

- Exposure X-Ray: This tool uncovers hidden stock concentrations in ETFs and mutual funds, giving users a clearer picture of their portfolio's risks.

- Fee & Fund Analyzer: It identifies funds with high expense ratios and suggests lower-cost alternatives that offer similar market exposure.

According to Mezzi, users managing over $2 billion in connected assets have, on average, identified over $1,000 in annual tax and fee savings. For example, reinvesting a single tax saving of $10,221 could potentially grow to $76,123 over 30 years, assuming a 7% annual return. Additionally, Mezzi’s Asset Location Optimization evaluates whether your investments are housed in the most tax-efficient accounts, such as Roth IRAs versus taxable accounts.

Privacy and Data Usage

Mezzi operates as an SEC-registered investment adviser, which means it adheres to strict fiduciary responsibilities and federal oversight. The platform uses secure, read-only access via trusted providers like Plaid and Finicity, ensuring your bank credentials and account numbers are never stored. Security measures include AES-256 encryption, TLS 1.3, and OAuth 2.0 for authentication. Mezzi also promises never to sell your data to third parties.

To deliver accurate insights, Mezzi requires a complete view of your financial landscape, including both assets and liabilities. This comprehensive approach, paired with robust privacy measures, underscores Mezzi’s dedication to safeguarding user data while offering actionable financial insights.

Pros and Cons

When comparing financial tools, it's worth noting that while Personal Capital offers "free" features, these often come with hidden costs tied to its advisory services. Personal Capital is well-regarded for its investment tracking and retirement planning tools, attracting over 2 million users who monitor their finances through the platform. However, these free tools often act as a gateway to high-cost advisory services, which require a minimum of $100,000 in assets and charge a 0.89% annual fee based on assets under management (AUM).

Mezzi, on the other hand, stands out with its flat-fee pricing model, which remains consistent regardless of portfolio size. Whether you're managing $100,000 or $10 million, you'll pay the same fixed annual fee - $299 for Core, $499 for Plus, or $1,499 for White Glove. This approach eliminates the potential conflicts of interest associated with percentage-based fees. Tools like Mezzi's Exposure X-Ray and Fee & Fund Analyzer help uncover hidden stock concentrations and high-cost funds, offering actionable insights to improve portfolio transparency. Here's a side-by-side comparison of key features:

| Feature | Personal Capital | Mezzi |

|---|---|---|

| Pricing Model | Free tools + 0.89% AUM fee for advisory (min. $100,000) | Flat annual fee: $299–$1,499 (no minimum) |

| Best For | Investment tracking, retirement planning | Tax optimization, fee analysis, portfolio transparency |

| Budgeting Tools | Basic cash flow tracking | Not a primary focus |

| Advisory Access | Requires $100,000 minimum | Fiduciary advice included at all tiers |

| Data Privacy | "We do not sell or allow your information to be used for any purpose other than to market our own products and services" | Never sells data; SEC-registered fiduciary |

While Personal Capital's budgeting tools allow for basic cash flow tracking, they fall short compared to specialized expense tracking platforms. Mezzi, meanwhile, prioritizes investment optimization over day-to-day expense management. If your main goal is monitoring spending habits, neither platform may fully meet your needs. However, for those focused on understanding fees, taxes, and portfolio overlap, Mezzi provides more detailed insights without the push toward percentage-based advisory services.

Privacy and security are another area of distinction. Personal Capital uses military-grade 256-bit AES encryption and read-only access, ensuring funds cannot be withdrawn through the app. Mezzi employs similar security measures but adds the assurance of being an SEC-registered fiduciary, which legally binds it to act in your best interest. Unlike Personal Capital, Mezzi does not use your data as a lead-generation tool for higher-fee services, emphasizing its commitment to transparency and client trust.

Conclusion

Personal Capital provides a range of free tools to help users track their net worth, monitor cash flow, and plan for retirement. However, these tools are part of a larger strategy aimed at steering users toward their fee-based wealth management services.

Mezzi, on the other hand, takes a straightforward flat-fee approach with pricing tiers of $299 for Core, $499 for Plus, and $1,499 for White Glove. This pricing remains consistent whether you're managing a modest portfolio or handling millions of dollars. There’s no minimum investment requirement or percentage-based fees that increase as your portfolio grows. As an SEC-registered fiduciary, Mezzi is committed to acting in your best interest while maintaining strict data privacy standards.

These differences underscore the distinct approaches of each platform. If your primary need is basic budgeting and cash flow tracking without upfront costs, Personal Capital’s free tools might meet your expectations. However, if your focus is on investment insights - such as identifying hidden fees, exploring tax-loss harvesting opportunities, or addressing overlapping holdings - Mezzi delivers these advanced services at a fixed, transparent cost.

For those prioritizing data privacy and control, Mezzi offers additional peace of mind. While Personal Capital employs strong security measures like AES-256 encryption and multi-factor authentication, Mezzi provides read-only access through secure aggregators like Plaid and Finicity, coupled with a heightened focus on safeguarding user data.

FAQs

Will Personal Capital call or message me after I link my accounts?

When you link your accounts with Personal Capital, they may reach out if you opt for their full-service wealth management, which provides access to financial advisors. However, if you're only using their free tools, you typically won't receive direct calls or messages.

What does a 0.89% AUM fee actually cost per year in dollars?

A 0.89% fee based on assets under management (AUM) means you'll pay $8.90 each year for every $1,000 invested. Since this fee is percentage-based, the total cost increases as the size of your investment grows. For larger portfolios, this can lead to notably higher annual expenses.

Which Mezzi tier should I choose for tax and fee savings?

The Core plan, priced at $299 per year, may suit those looking to manage taxes and fees effectively. It includes tools designed to help lower tax liabilities and analyze returns to uncover potential fee-saving opportunities. For those seeking more advanced features, the Plus plan at $499 per year adds AI-driven insights and personalized support. That said, the Core plan offers a range of practical tools at a lower cost, making it a solid choice for many users.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- Registration does not imply a certain level of skill or that the SEC has approved the company or its services.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.