A private family foundation may fit when you want two things at once: an upfront charitable deduction and family control over grants for years to come. But that control may come with tradeoffs: a 5% annual payout rule, a 1.39% excise tax on net investment income, public Form 990-PF filings, and yearly costs that may run from $5,000 to $30,000+.

Here’s the short version:

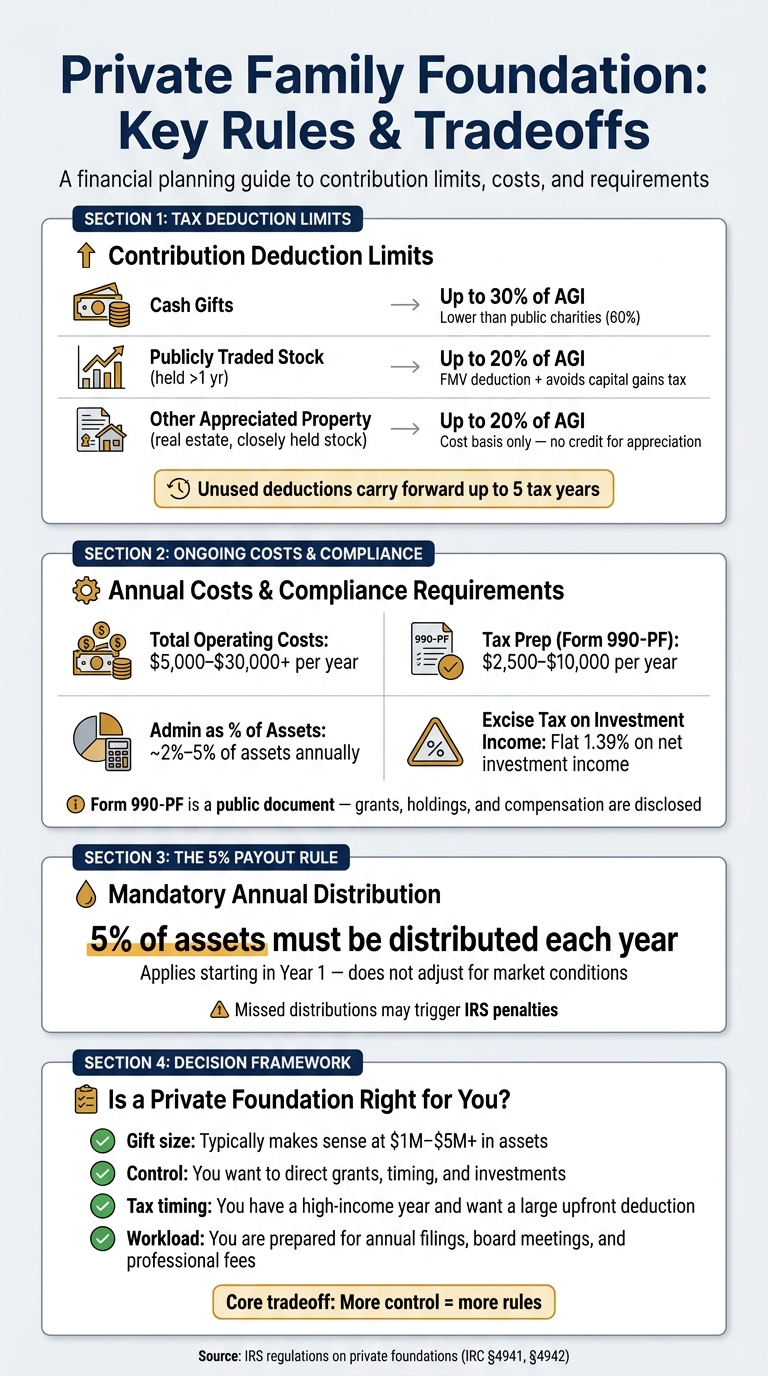

- You may deduct cash gifts up to 30% of AGI

- You may deduct long-term publicly traded stock up to 20% of AGI

- Extra deductions may carry forward for up to five tax years

- Donated assets may leave your taxable estate

- Family members may keep board control, set grant timing, and shape the mission

- The setup often may make more sense when assets are around $1 million to $5 million or more, since costs may otherwise take up too much of the charitable pool

The basic tradeoff is simple: more control, more rules.

If I were sizing this up, I’d look at four things first:

- Gift size: Smaller amounts may not justify the setup costs

- Control: Some families want to pick grants, timing, and investments themselves

- Tax timing: A high-income year may make the upfront deduction more useful

- Workload: Annual filings, records, payout rules, and self-dealing limits do not go away

| Area | What may appeal to families | What may add friction |

|---|---|---|

| Tax treatment | Upfront deduction; estate tax removal | Lower AGI limits than public charities |

| Assets donated | Public stock may get FMV deduction and avoid capital gains tax | Nonstock appreciated property may be limited to cost basis |

| Control | Family-run board may choose grants and timing | IRS rules may limit scholarships, grants, and transactions |

| Administration | Long-term family giving structure | Public filing, excise tax, yearly costs, and payout rules |

So if your main goal is simple giving, a private foundation may feel heavy. If your main goal is keeping family control over philanthropy across generations, it may be worth a close look.

Private Family Foundation: Tax Rules, Costs & Deduction Limits at a Glance

Using Private Family Foundations to Save Millions | Dana Whiting Law

What a private family foundation is and why families use one

A private family foundation is a tax-exempt charitable entity funded mainly by one family and set up as a separate nonprofit corporation or charitable trust.

That setup is different from writing a check straight to a charity. With a foundation, the family may receive an immediate tax deduction, then distribute grants to causes over months or years. That's the basic tradeoff: tax treatment on one side, long-term control on the other.

How the structure gives families control

The main feature here is family-controlled governance. The board does not need to be independent, which means the family may control the board, choose recipients, set grant amounts, and decide timing, subject to the 5% annual payout rule.

Because a foundation may exist in perpetuity, it may also serve as a legal structure for passing philanthropic values to children and grandchildren through active board participation.

Common uses for wealthy U.S. families

Many families contribute cash or appreciated stock and then make grants over time. Appreciated stock held for more than one year may be especially useful, because the donor may avoid capital gains tax while receiving a deduction for the stock's fair market value.

Foundations may also fund scholarships and other individual grants, though only under IRS rules. For families that want more than one generation involved, a foundation may provide a structured setting for active board participation and shared decision-making across the family.

Cash, appreciated stock, and scholarships all show the same basic pattern: families may keep control over who receives support and when. Next: how cash and appreciated stock contributions shape the deduction.

Tax deductions and funding strategies: where the financial upside comes from

The main tax upside may come from two places: an upfront deduction when the foundation is funded, and the option to contribute appreciated assets without selling them first.

Cash, appreciated stock, and deduction limits

When you contribute cash to a private foundation, the deduction is generally capped at 30% of your adjusted gross income (AGI). If you contribute long-term appreciated publicly traded stock, that cap drops to 20% of AGI. For long-term publicly traded stock, you generally deduct fair market value and avoid capital gains tax.

There’s one key line to draw here. That fair market value treatment generally applies to publicly traded stock held for more than one year. For nonstock appreciated property, the deduction is usually limited to cost basis.

If your contribution goes above either AGI limit in a given year, the excess carries forward and may be deducted over the next five tax years.

| Contribution Type | AGI Deduction Limit | Valuation Basis | Caveat |

|---|---|---|---|

| Cash | 30% of AGI | Cash amount contributed | Lower limit than public charities (60%) |

| Publicly traded stock (held >1 year) | 20% of AGI | Fair market value | Avoids capital gains tax |

| Other appreciated property (real estate, closely held stock) | 20% of AGI | Cost basis only | No credit for appreciation |

This setup may give families room to claim the deduction now and decide on grants later. That’s one reason some families choose to fund a foundation in a high-income year, then spread grants out over time.

There’s another tax item in the background. Private foundations are tax-exempt, but they still pay a flat 1.39% excise tax on net investment income. That includes interest, dividends, and realized capital gains from selling donated assets. It may look small on paper, but it’s still part of the math.

Why contribution timing can matter more than the grant schedule

A private foundation may let you separate funding from grant timing. You may make a large contribution in a year when income jumps - after a business sale, a large bonus, or a year with major capital gains - claim the deduction subject to the AGI limits, and then distribute grants over time.

That timing gap may be the main draw. The tax event happens now. The grantmaking schedule may happen later.

There’s also an estate planning angle. Assets transferred to a foundation are removed from your taxable estate, which may matter for families with federal estate tax exposure. Charitable bequests to private foundations receive an unlimited estate tax deduction, so the foundation may work as both a current-year tax tool and a longer-term estate planning structure.

For high earners, recent deduction limits may make contribution size and timing more important.

The next question isn’t just how much to give. It’s how much control the family may want to keep.

Philanthropic control, family governance, and long-term legacy

For many families, the tax deduction may matter less than control. A private foundation may let them direct grants, set policy, and keep a family mission in place over time. But that kind of control may only hold up if the family writes down how decisions are made.

Control over grants, recipients, and timing

The board sets grant policy, mission priorities, and approval standards. Families may also reset grant priorities and mission focus over time.

The board may also connect the endowment to the mission through a written Investment Policy Statement (IPS). Those rules may keep decision-making more consistent as leadership changes. Scholarships and hardship grants come with specific IRS procedures and may require advance approval.

Using the foundation as a family governance tool

A foundation may give families a formal way to make charitable decisions together over time. Assigning board roles like President, Treasurer, and Secretary may create clearer accountability. Regular board meetings, along with written grant criteria, may make giving more repeatable across generations.

Succession planning is often the part families may spend too little time on early. Governing documents may spell out how future board members are appointed, what voting thresholds apply to major decisions, and how the mission is protected as generations change. Formal roles, voting rules, and a clear mission statement may help preserve family control as leadership shifts.

These documents may turn family influence into governance that lasts.

| Governance Tool | What It Does |

|---|---|

| Mission Statement | Anchors giving priorities and may reduce mission drift across generations |

| Succession Rules | Defines how leadership transitions to the next generation |

| Investment Policy Statement (IPS) | Documents asset allocation and spending policy for the endowment |

| Written Grant Criteria | Turns unstructured giving into a structured, repeatable process |

| Conflict of Interest Policy | May guard against self-dealing and internal disputes |

Family members may also be hired as paid staff to manage day-to-day operations, as long as compensation is reasonable under IRS rules.

The tradeoffs: compliance, costs, and how to decide if it fits

A private family foundation is not a set-it-and-forget-it structure. The tax deduction and level of philanthropic control may appeal to some families, but those features come with annual work, rules, and costs that do not go away.

What ongoing administration actually looks like

The upside only works if the foundation is set up to handle yearly filings, payout rules, and strict IRS limits.

Every foundation must file Form 990-PF each year. That return is public and lists grants, holdings, compensation, and transactions with disqualified persons. Tax prep alone typically runs $2,500 to $10,000 per year.

There is also the 5% annual distribution rule. It applies starting in year one, and it does not adjust for market conditions. If the requirement is missed, penalties may apply.

Self-dealing rules add another layer. Under IRC §4941, most transactions between the foundation and disqualified persons are prohibited. Penalties start at 10% of the amount involved and may rise to 200% if the issue is not corrected.

On top of that, annual administration often runs about 2% to 5% of assets, with total operating costs usually landing between $5,000 and $30,000+, before investment management fees.

A practical decision framework for Mezzi readers

If that workload still feels manageable, the next step is simpler: does the tax break and control justify the size of the gift?

For many people, the answer may come down to four points:

- How much are you planning to contribute? If the gift falls below the minimum funding threshold, admin costs may take up a meaningful share of what you meant to give away.

- Do you want direct control over investments and grantmaking? If that matters to you, a foundation may offer more room to shape both.

- Are you having an unusually high-income year? In that case, a large upfront deduction may reduce your tax bill in a more meaningful way.

- Are you prepared for multi-year compliance? That may include annual filings, board meetings, grant records, and professional fees that keep showing up year after year.

Mezzi may model the tax impact of donating appreciated shares and the portfolio effect of a large gift.

Conclusion: tax benefits are real, but control is what you are paying for

That’s the tradeoff in one line: control and tax benefits versus recurring compliance.

The compliance work does not pause. The 990-PF is public. Costs may add up whether or not the market cooperates. If your main goal is simplicity, a private foundation may bring more complexity than you want. If your main goal is philanthropic control, and you want a structure that may carry that forward across generations, a private family foundation may feel worth the cost. The core question is whether the tax benefit and control outweigh the compliance burden.

FAQs

When does a private family foundation make sense?

A private family foundation may make sense if you want long-term control over your giving and have enough assets to handle the extra admin work that comes with it. In many cases, people tend to view this route as more workable when there’s at least $1,000,000 in assets behind it.

It may also be a fit if you want to do more than write grants. For example, some families use a foundation to:

- manage investments

- hire staff

- involve multiple generations in governance

- run their own charitable programs

- provide scholarships directly

- support organizations outside public charity grant rules

That added control may appeal to families who want a more hands-on role in how their philanthropy is structured and carried out.

Can I donate real estate or a business interest?

Yes. A private family foundation may be funded with real estate, business interests, cash, and securities.

That said, private foundations may face strict IRS rules, including self-dealing limits. Because of that, some families work with qualified legal and tax professionals to help with valuation and compliance and to reduce the chance of potential excise taxes.

How much control can my family actually keep?

A private family foundation may give your family a high level of control over its giving and long-term direction. As board members, family members may decide which causes to support, who may receive grants, and when those gifts may be made.

You may also oversee investments, bring multiple generations into governance, and hire family members as staff. While oversight is generally shared with at least three board members, founders often select relatives and trusted advisors to help carry out their vision.

Disclosures:

• This content is for informational purposes only and does not constitute investment, tax, or legal advice. Readers should consult qualified professionals regarding their specific circumstances.

• Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

• All examples and scenarios described are hypothetical and for illustrative purposes only. Actual results will vary based on individual circumstances, portfolio composition, market conditions, and fees.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.