If you’re earning over $200,000, deciding between a Roth and Traditional 401(k) is one of several tax strategies for high-net-worth individuals that can significantly impact your lifetime savings. Here's the quick breakdown:

- Roth 401(k): Pay taxes upfront, but enjoy tax-free withdrawals in retirement. Ideal if you expect higher future tax rates or want to avoid Required Minimum Distributions (RMDs).

- Traditional 401(k): Get an immediate tax deduction, but withdrawals are taxed later. Best if your retirement tax rate will be lower than your current one.

Key Factors to Consider:

- Your current tax bracket (e.g., 37% for top earners in 2025).

- Future tax rate expectations (e.g., potential increase to 39.6% after 2025).

- RMD rules (Traditional accounts require withdrawals; Roth accounts don’t if rolled into a Roth IRA).

- Estate planning advantages (Roth assets transfer tax-free to heirs).

Quick Tip: Many high earners split contributions between Roth and Traditional accounts to balance tax benefits now and later. Starting in 2026, catch-up contributions for those earning over $145,000 must go into a Roth account.

Quick Comparison:

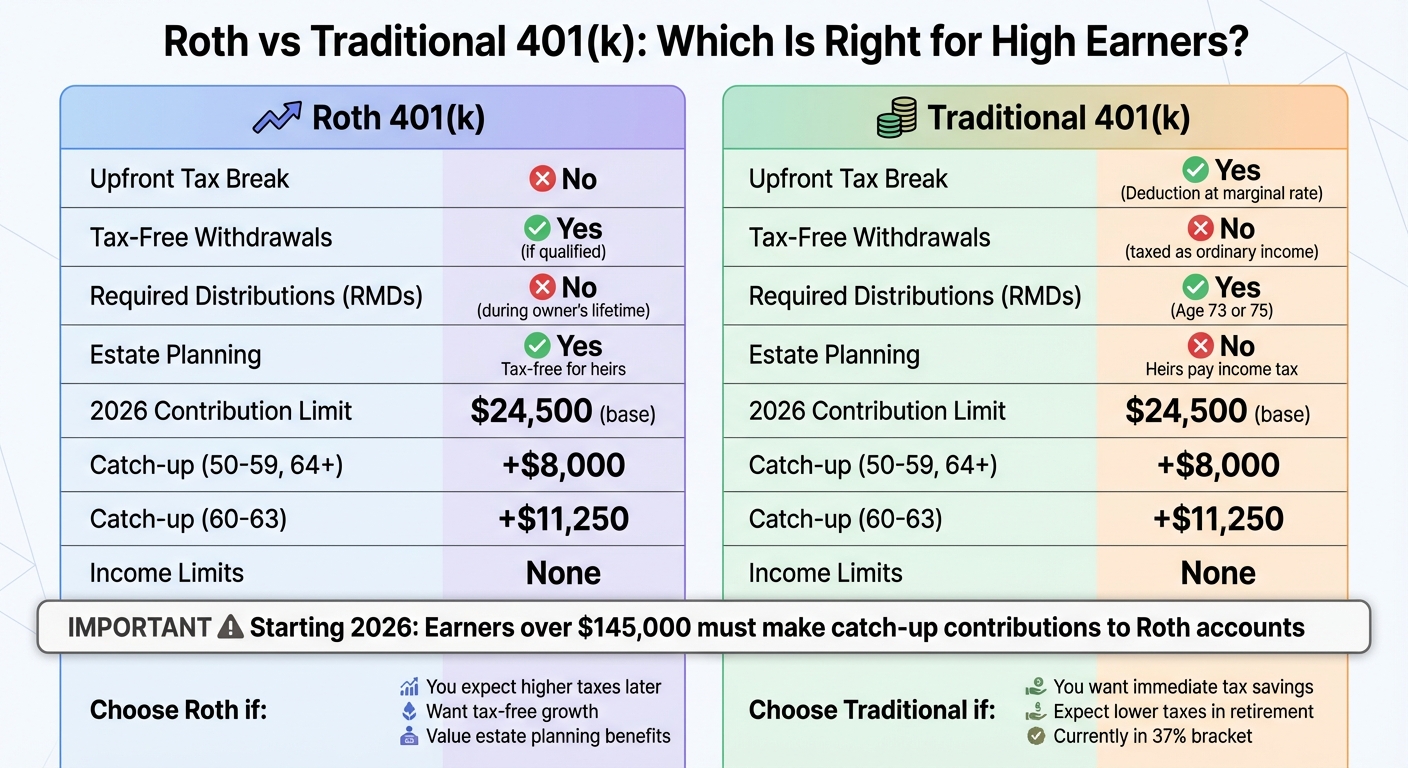

| Feature | Roth 401(k) | Traditional 401(k) |

|---|---|---|

| Upfront Tax Break | No | Yes |

| Tax-Free Withdrawals | Yes (if qualified) | No (taxed as income) |

| Required Distributions | No (if rolled to Roth IRA) | Yes (age 73/75) |

| Estate Planning | Tax-free for heirs | Taxable for heirs |

| Income Limits | None | None |

Bottom Line: Choose Roth if you expect higher taxes later or value tax-free growth. Opt for Traditional if you want immediate tax savings and expect lower taxes in retirement.

Roth vs Traditional 401(k) Comparison for High Earners

1. Roth 401(k)

Tax Treatment

Contributing to a Roth 401(k) means you're using after-tax dollars, which won't reduce your current taxable income. For example, if you're in the 37% tax bracket and contribute $24,500, you won't see an immediate tax break.

The real advantage comes later. Once you hit age 59½ and have held the account for at least five years, all withdrawals - both your contributions and any investment growth - are completely tax-free. This setup can be especially appealing for high earners who expect to remain in a high tax bracket or see their tax rates increase during retirement.

"Roth dollars hold greater value since withdrawals are tax free, unlike traditional 401(k) dollars which remain subject to tax." – Bernstein

Understanding these tax benefits is just the beginning. It's also important to know the contribution rules and limits.

Contribution Rules and Limits

In 2026, employees can contribute up to $24,500 to a Roth 401(k), regardless of income. Unlike Roth IRAs vs. Roth 401(k)s, where IRAs have income restrictions, Roth 401(k)s are open to everyone, even high earners.

For those aged 50 or older, there's an opportunity to make catch-up contributions. These allow an additional $8,000, bringing the total contribution limit to $32,500. If you're between 60 and 63, the catch-up amount increases to $11,250, raising the total to $35,750. Starting in 2026, anyone earning more than $150,000 in the prior year will need to allocate all catch-up contributions to their Roth account.

| Age Group | Regular Deferral | Catch-up Limit | Total Employee Limit |

|---|---|---|---|

| Under 50 | $24,500 | N/A | $24,500 |

| 50–59 | $24,500 | $8,000 | $32,500 |

| 60–63 | $24,500 | $11,250 | $35,750 |

| 64+ | $24,500 | $8,000 | $32,500 |

Retirement Withdrawal Impacts

Roth 401(k)s provide flexibility during retirement. Since qualified withdrawals are tax-free, you can manage your income without worrying about triggering higher tax brackets. Another key perk: starting in 2024, Roth 401(k)s are no longer subject to Required Minimum Distributions (RMDs) during your lifetime.

Employer Match Considerations

To maximize your benefits, ensure you're contributing enough to capture your full employer match - this is essentially free money. Typically, unless your employer has implemented specific SECURE 2.0 rules, matching contributions go into a traditional (pre-tax) account rather than your Roth balance. This creates a mix of taxable and tax-free savings, giving you options when planning withdrawals in retirement.

Future Tax Rate Projections

For high-income earners, future tax rates are a major consideration. With the Tax Cuts and Jobs Act set to expire after 2025, the top federal tax rate could rise from 37% to 39.6%. If you anticipate higher taxes in the future - or plan to retire in a state with higher tax rates - choosing a Roth 401(k) lets you lock in today's rates.

"If you think taxes will rise: Tilt toward Roth. Lock in today's rates." – SmartSMSSolutions Content Team

Balancing both Roth and traditional accounts can add flexibility. For instance, in a high-income year, you could rely on tax-free withdrawals from your Roth account, while in a lower-income year, you might save money by withdrawing from a traditional account at a reduced tax rate.

Next, we'll dive into the Traditional 401(k) to explore its tax benefits and strategies for high earners.

2. Traditional 401(k)

Tax Treatment

A Traditional 401(k) helps reduce your taxable income for the year you contribute. Since contributions are made with pre-tax dollars, your taxable income decreases, which can lower your immediate tax bill. For example, if you earn $500,000 and fall into the 37% federal tax bracket, contributing $24,500 could save you around $9,065 in taxes that year. Additionally, your investments grow tax-deferred, meaning no annual taxes on dividends or capital gains. However, withdrawals during retirement are taxed as ordinary income.

"Traditional 401(k)s offer an upfront tax break... However, you'll owe ordinary income tax on all your contributions and any associated earnings in retirement." – Kailey Hagen, CFP, The Motley Fool

This tax structure allows you to delay taxes until retirement, potentially benefiting from a lower tax rate when you begin taking distributions. For instance, with a standard deduction of approximately $15,000 for singles (or $30,000 for married couples) in 2025, you could withdraw up to these amounts tax-free. This feature is particularly appealing to high earners who wish to take advantage of their current high marginal tax rates - often 32%, 35%, or 37% - while planning for potentially lower rates in retirement.

Contribution Rules and Limits

For 2026, the employee deferral limit is set at $24,500. Unlike Roth IRAs, 401(k) contributions have no income restrictions.

If you're 50 or older, you can make additional catch-up contributions. These include an extra $8,000 for those aged 50–59 or 64 and older, and $11,250 for individuals aged 60–63. However, if you're classified as a Highly Compensated Employee (earning $155,000 or more in 2024 for 2025 testing), your contributions may be limited or partially refunded if your employer's plan doesn't pass IRS non-discrimination testing.

Retirement Withdrawal Impacts

Required Minimum Distributions (RMDs) must begin at age 73 or 75, depending on your birth year. These withdrawals are taxed as ordinary income, which could significantly increase your taxable income if you have large savings. High earners need to carefully plan their withdrawals to minimize tax burdens.

That said, the Traditional 401(k) offers some flexibility. If you retire early - before Social Security kicks in - you might find yourself in a lower tax bracket, making it a great time to withdraw funds at a reduced tax rate. Some people also explore partial Roth conversions during these lower-income years to reduce the impact of future RMDs.

Employer Match Considerations

Employer matching contributions always go into the Traditional account, even if you choose to contribute to a Roth 401(k). This means a portion of your retirement savings will remain taxable.

If you max out your contributions early in the year to hit the $24,500 limit, check whether your plan includes an annual "true-up" provision. Without it, you could miss out on employer match contributions for the rest of the year once your contributions stop. This highlights the importance of understanding employer-specific rules to maximize your retirement benefits.

Future Tax Rate Projections

The Tax Cuts and Jobs Act is set to expire after 2025, potentially increasing the top federal tax rate from 37% to 39.6%. This uncertainty makes it essential for high-income earners to weigh immediate tax savings against deferred tax benefits when planning their retirement strategy.

If you live in a high-tax state like California or New York, taking the deduction now could be even more beneficial, especially if you plan to retire in a no-income-tax state like Florida or Texas. Reducing your Adjusted Gross Income (AGI) today can also help you stay below phase-out thresholds for certain tax credits or lower Income-Driven Repayment amounts if you're pursuing Public Service Loan Forgiveness.

Next, we’ll dive into a comparison of the pros and cons of the Traditional 401(k) and Roth 401(k) to guide your decision-making process.

Where Most People Get the Roth vs Traditional Math Wrong

Advantages and Disadvantages Compared

When deciding between a Traditional 401(k) and a Roth 401(k), it really comes down to how you want to handle taxes now versus in retirement. If you're currently in a high tax bracket, like 35% or 37%, and expect to drop into a lower bracket later, a Traditional 401(k) might be the better choice. Why? Because you get an immediate tax deduction, which lowers your taxable income and could save you thousands each year. However, keep in mind that withdrawals in retirement will be taxed as ordinary income, and required minimum distributions (RMDs) could push you into a higher tax bracket down the road. Plus, if your heirs inherit the account, they’ll need to withdraw the funds within 10 years and pay taxes on them as well.

On the other hand, Roth 401(k)s shine when it comes to tax-free growth and withdrawals - provided you meet the qualifications. This makes them especially appealing for high earners who max out their contributions. For instance, $24,500 in after-tax dollars keeps its full value, unlike pre-tax contributions that shrink when taxes come due later. Roth accounts also act as a safeguard against future tax rate increases, and heirs can inherit these funds tax-free, which is a big plus for estate planning. The downside? You’ll pay taxes upfront at your current marginal rate, which can be a tough pill to swallow if you’re already in the 37% bracket.

"Traditional contributions give you a tax deduction now, lowering your current taxable income. But you'll pay taxes later in retirement. Roth contributions are made with after-tax dollars... but your withdrawals in retirement are tax-free." – TJ van Gerven, Founder, Memento Financial Planning

For high-income earners, the key is often finding the right balance. Many choose to split their contributions between the two options to create "tax diversification." This approach gives you flexibility in managing your taxable income during retirement.

| Feature | Traditional 401(k) | Roth 401(k) |

|---|---|---|

| Upfront Tax Break | Yes (Deduction at marginal rate) | No (Paid with after-tax dollars) |

| Taxation of Withdrawals | Taxed as ordinary income | Tax-free (if qualified) |

| RMD Requirements | Yes (Age 73 or 75) | No (during owner's lifetime) |

| Estate Planning | Heirs pay income tax | Heirs receive tax-free |

| Income Limits | None | None |

| 2026 Contribution Limit | $24,500 ($35,750 if 60–63) | $24,500 ($35,750 if 60–63) |

These comparisons highlight the importance of tailoring your 401(k) strategy to your individual financial situation and long-term goals.

Using AI Tools to Choose Your 401(k) Strategy

Deciding between Roth and Traditional 401(k) contributions isn’t a one-and-done choice - it evolves as your income changes, tax laws shift, and retirement approaches. That’s where Mezzi steps in. This tool analyzes your entire financial landscape in real time, showing how different strategies could influence your long-term wealth.

Mezzi connects to all your accounts - 401(k), Roth IRA, taxable brokerage accounts, and more - through read-only access. It then models scenarios for your entire portfolio. For instance, if you have substantial non-retirement investments generating capital gains, Mezzi factors that in when determining whether Roth or Traditional contributions make more sense. It also explores strategies like Roth conversions during early retirement (before Social Security begins), helping you take advantage of lower tax brackets and potentially reduce future required minimum distributions (RMDs). This level of insight extends to adapting to new regulations as they arise.

Take the upcoming 2026 mandatory Roth catch-up rule, for example. Under this regulation, high-income earners over 50 who made more than $145,000 in the previous year must direct their catch-up contributions to a Roth account. Mezzi models how this change could affect your tax strategy.

"Beginning in 2026, high-income retirement plan savers over 50 years old must execute their employee deferral catch-up contribution as a Roth." – Kiplinger

For high-income earners, real-time adjustments like these are vital for fine-tuning 401(k) strategies. With Mezzi, you can ask targeted questions like, “Should I max out my Roth 401(k) or stick with Traditional based on my current tax bracket?” and get clear, personalized answers. It’s like having a financial advisor - without the $10,000/year price tag. Plus, as an SEC-registered fiduciary, Mezzi is legally obligated to prioritize your best interests, ensuring unbiased guidance without pushing commission-based products.

Conclusion

Deciding between Roth and Traditional 401(k) contributions depends heavily on your current income level and future tax expectations. If you're at the peak of your earning years - for example, earning over $751,600 as a married couple filing jointly in 2025 (placing you in the 37% tax bracket) - Traditional contributions often make more sense. They allow you to save significantly on taxes now, with the expectation of withdrawing funds during retirement at a lower effective tax rate. On the other hand, if you're early in your career or anticipate higher tax rates after the Tax Cuts and Jobs Act sunsets in 2025, Roth contributions provide tax-free growth and greater flexibility for the future.

Many high earners find balance by combining both account types. A common approach is allocating 60% to Traditional and 40% to Roth accounts. This strategy gives you flexibility in retirement: you can use Traditional withdrawals to fill lower tax brackets while accessing Roth funds for amounts exceeding that threshold, avoiding higher tax rates or Medicare surcharges.

State taxes also play a role. Traditional contributions can save you 6-13% in state taxes if you work in a high-tax state but plan to retire in tax-friendly states like Florida or Texas. Additionally, if you're focused on leaving a legacy, Roth accounts are ideal. They remain tax-free for heirs for 10 years after inheritance and don't require Required Minimum Distributions (RMDs) during your lifetime if converted to a Roth IRA. Staying informed about changing regulations is crucial to maximize these benefits.

"The fundamental rule is simple: if your tax rate will be higher in retirement than it is now, choose Roth. If your tax rate will be lower in retirement, choose traditional pre-tax." – SmartSMSSolutions

One important update: starting in 2026, catch-up contributions for individuals earning over $145,000 must go directly into a Roth account. Tools like Mezzi can help you adjust your 401(k) strategy dynamically as your financial situation and tax laws evolve.

FAQs

How do I estimate my tax rate in retirement?

To figure out your tax rate in retirement, it's essential to focus on your effective tax rate - the percentage of your income that goes toward taxes. Start by evaluating your current income and estimating what your income will look like in retirement. Be sure to account for all retirement income sources, like Social Security, pensions, or withdrawals from retirement accounts. Also, keep potential changes in tax laws in mind, as they could impact your future tax obligations. Tools like 401(k) calculators can be incredibly helpful in projecting whether your tax burden will increase or decrease once you retire.

Should I do Roth conversions before RMDs start?

Yes, individuals with higher incomes might find it worthwhile to consider Roth conversions before Required Minimum Distributions (RMDs) kick in at age 73 (or 75, depending on current regulations). By converting funds from a traditional 401(k) to a Roth account, you can potentially reduce future RMDs and lower your taxable income during retirement. Since qualified Roth withdrawals are tax-free, this approach could be particularly advantageous for those anticipating higher tax rates later on or looking to streamline estate planning for heirs.

How does my state’s taxes change the Roth vs. Traditional choice?

State taxes are an important factor when weighing the pros and cons of Roth versus Traditional 401(k) contributions. If your state imposes income taxes, contributing to a Traditional 401(k) can reduce your taxable income now, potentially lowering your current tax burden. However, keep in mind that when you retire, withdrawals from a Traditional 401(k) will likely be subject to both state and federal taxes.

On the other hand, Roth 401(k) contributions are made with after-tax dollars, meaning you won’t get an upfront tax break. But the big advantage? Withdrawals in retirement are tax-free. This can be especially appealing if you anticipate higher taxes in the future or currently live in a state with high income tax rates.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

- Registration does not imply a certain level of skill or that the SEC has approved the company or its services.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.