If part of your money sits in euros, pounds, or other non-U.S. currencies, your net worth may move even when you do nothing. FX swings of 10% to 20% a year may change your total almost as much as saving or investing.

Here’s the short version: I may keep each account in its native currency, convert everything into one base currency such as USD, use one FX rate rule on the same date each month, and track market movement separately from currency movement. That setup may make month-to-month changes easier to read.

At a glance, the article covers:

- What counts in multi-currency net worth: assets and debts across bank accounts, brokerages, property, RSUs, loans, and mortgages

- Why totals may differ across apps: different FX sources, update times, and pricing rules

- How to pick a base currency: often the one linked to spending, taxes, and long-term plans

- How to set one FX policy: for example, USD base, mid-market rate, last business day of each month

- How to convert balances: record the local amount first, then convert once

- How to avoid bad math: no double-counting, no mixed FX dates, no mixed rate sources

- How to split changes: local asset return vs. FX impact

- How to run it monthly: in a spreadsheet or a tool that may sync balances and FX data

A simple example: if I hold €48,000 and the euro moves against the dollar, my USD net worth may change even if that euro balance stays the same. That’s the core idea.

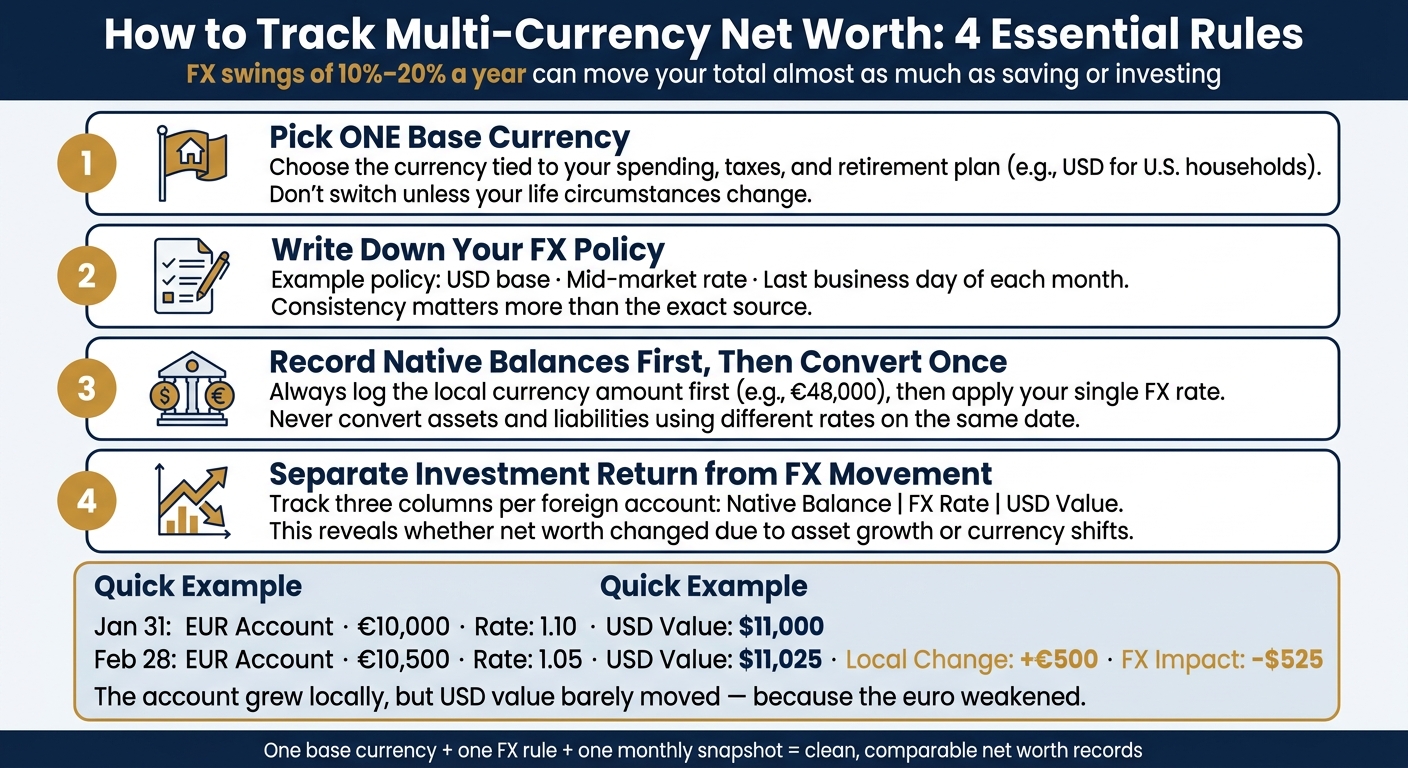

If I want a clean multi-currency net worth view, this article points to four rules: pick one base currency, write down one FX rule, record native balances first, and separate investment return from FX effects.

How to Track Net Worth in Multiple Currencies: 4 Key Rules

Choose one home currency and write down your rules

For most U.S. households, USD may be the practical base currency. The IRS requires capital gains and foreign account reporting to be calculated in USD, which may make it the natural default for tracking net worth over time.

Pick the currency that matches your spending, taxes, and long-term plan

For most U.S. households, USD may be the right base currency because it lines up with spending, taxes, and retirement planning. In plain English, your base currency may be the one tied to where you spend, file taxes, and expect to retire.

Once that base currency is fixed, every account may need to be converted the same way on each reporting date. That keeps your records clean and makes month-to-month comparisons easier to follow.

Set one FX policy for every reporting date

Next, pick the single FX rule you'll use for every snapshot. The table below covers the two methods that matter most:

| FX Timing Method | Pros | Cons | Best Use Case |

|---|---|---|---|

| Month-End Snapshot | Simple, reproducible, smooths intra-month swings | Misses mid-month currency moves | Long-term net worth tracking |

| Transaction Date | Essential for tax compliance and cost basis | Requires diligent record-keeping | Tax reporting and performance attribution |

For most households, the month-end mid-market rate may be the most sustainable method. The bigger point: use one conversion method every month. Consistency may matter more than the exact source.

Write the rule in one line: Base currency USD; FX source mid-market; valuation date last business day of the month.

When changing your base currency makes sense

A base currency change may make sense when your financial life changes, not when markets move. The main cases are a permanent move to another country or a clear decision that retirement may be funded in a different currency.

If you switch, some households start a new series and leave prior balances untouched, so historical trend lines may stay clean.

Convert each asset and liability the same way every time

Once your FX policy is set, use the same process for every balance. Record the amount in its native currency first. Then convert it to your base currency one time.

That sounds simple, but it may keep your reporting cleaner. The examples below show how the rule may apply to cash, securities, property, and debt.

Record native balances first, then convert to your base currency

Say you have a French bank account with EUR 48,000. Start by recording the euro balance as-is. Then apply the EUR/USD rate from your valuation date.

If the exchange rate changes next month, the USD reporting value may change even if the EUR balance stays the same. That’s normal. The account itself didn’t move in local terms; only the converted reporting value may have changed.

How to handle brokerage accounts, foreign cash, RSUs, property, and debt

Use the same sequence for each item: value it in local terms first, then convert once.

| Account Type | Native Currency | Conversion Approach |

|---|---|---|

| U.S. brokerage | USD | Report in USD; no conversion needed |

| Foreign bank account | Local currency | Record the exact local balance; convert it using your month-end rate |

| Vested RSUs | Usually USD | Use the vested market value, then convert |

| Overseas property | Local currency | Estimate the market value locally, subtract any local mortgage, then convert the net equity |

| Foreign mortgage or loan | Local currency | Record it as a negative balance in native currency; its USD value may change with FX |

For property, calculate net equity in local currency first. Then convert that figure to your base currency. In other words, don’t convert the home value and mortgage separately unless that matches your reporting method all the way through.

Common mistakes that distort net worth

Once the conversion method is standardized, the main issue may be inconsistency.

Don’t count the same asset twice in both native currency and USD. A safer setup may be to make the converted amount a calculated field instead of a manual entry.

Using different FX rates for assets and liabilities on the same reporting date may also skew the numbers. Use one FX rate for every asset and liability on each reporting date. Annual FX swings of 10% to 20% are common, so even a gap of a few days may add noise to your balance sheet, especially when large liabilities are involved.

Separate market performance from currency movement

Once every account uses the same conversion method, split each change into asset performance and FX movement. A higher net worth total may reflect stronger investment returns, a weaker U.S. dollar, or some mix of the two. That difference may affect how someone reads the numbers for planning.

Measure investment change in local currency before applying FX

Start with the return in the asset’s local currency. Then treat the currency move as a separate effect.

Here’s a simple example. An investor buys a $10,000 U.S. ETF when EUR/USD is 1.10, so the cost is €9,091. One year later, the ETF grows 8% in USD to $10,800. If EUR/USD moves to 1.20, the ending value in euros becomes €9,000. So the asset posted a gain in its local market, but the investor still saw a loss in base-currency terms because of the FX move.

Tag contributions, withdrawals, dividends, and currency trades separately. Those are cash flows, not performance.

Use a monthly time series to isolate the FX effect

Use the same month-end timestamp and store the local balance, FX rate, and base-currency value in separate columns. Over time, that may give you a clean record of what changed and what may have driven the change.

Use one monthly template for every account so the local move and the FX impact stay visible.

| Date | Asset (Native) | Native Balance | FX Rate (to USD) | USD Value | Local Change | FX Impact |

|---|---|---|---|---|---|---|

| Jan 31 | EUR Account | €10,000 | 1.10 | $11,000 | - | - |

| Feb 28 | EUR Account | €10,500 | 1.05 | $11,025 | +€500 | -$525 |

In the example above, the account grew by €500 in local terms, but the USD value barely changed because the euro weakened. Without the native balance column, it may be tough to tell whether the move came from the asset itself or from currency movement.

This method may show whether net worth changed because assets grew or because FX moved.

Build a repeatable system and the key rules to follow

Run the process monthly in a spreadsheet or in Mezzi

Use the same month-end date from the previous step and update balances once a month. At month-end, pull each balance in its native currency, convert it one time with your fixed FX rate, and record the result in USD.

For each foreign account, track three columns:

- Native balance

- FX rate

- USD value

That setup may make errors easier to spot. Manual entry may increase error risk, and FX rates may change quickly.

The main goal is to choose a workflow you may repeat without changing the FX rule. Mezzi may bring linked accounts into one place, update FX automatically, and flag overlapping exposure.

| Feature | Spreadsheet | Mezzi |

|---|---|---|

| FX Rates | Manual or formula-based | Automatic updates |

| Data Entry | Manual entry for each account | Automated via read-only sync |

| Separates market moves from FX | Often mixes FX and market gains | Helps separate FX from asset return |

| Security | Local-file risk | Encrypted storage, read-only access |

Conclusion: 4 rules that keep multi-currency net worth clean

Four rules may help keep the numbers steady over time. Pick one base currency and avoid switching it unless your life circumstances change in a meaningful way. Write down your FX policy - the rate source and the reporting date - so each update follows the same logic. Always record the native balance first, then convert it; that may preserve the local record of each account and may prevent old data from shifting each time rates move. And separate investment performance from currency movement so you may see whether your net worth changed with asset growth or with a weaker dollar.

With one base currency, one FX rule, and one monthly snapshot, your net worth may stay more comparable from month to month - and your records may stay clean enough to use with confidence.

FAQs

How do I choose my base currency?

Choose the currency you use to think about your money and spending most naturally. In many cases, that may be your home currency. For many U.S. readers, that may be USD.

Using one main currency may make net worth tracking easier to read over time. For accuracy, assets and liabilities may stay in their original currencies, then be converted with consistent, current exchange rates.

Should I use the same FX rate every month?

Usually, no. Using the same FX rate every month may distort your net worth, especially when exchange rates move a lot.

A better approach may be to use a steady method, such as the month-end rate for each period or the actual rate tied to each asset or transfer. It may also make sense to update rates regularly and separate currency moves from actual asset performance.

How do I separate investment gains from FX changes?

Track each asset’s return in its native currency first. Then convert it to your base currency with the same FX rate source each time. For every valuation or cash event, record the exchange rate you used.

That approach may let you separate the currency translation effect from the asset’s own performance. In plain English, you may get a cleaner view of how much of a net worth change may be tied to investment gains versus FX moves.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.