Tracking your net worth is key to understanding your financial health. It’s not just about income - it’s about knowing what you own (assets) minus what you owe (liabilities). If you have real estate, investments, and cash, keeping an accurate picture can feel overwhelming. Here’s how to make it easier:

- Include the right assets and liabilities: Focus on liquid assets (cash, savings), investments (stocks, 401(k)), and real estate (homes, rental properties). Subtract debts like mortgages, loans, and credit card balances.

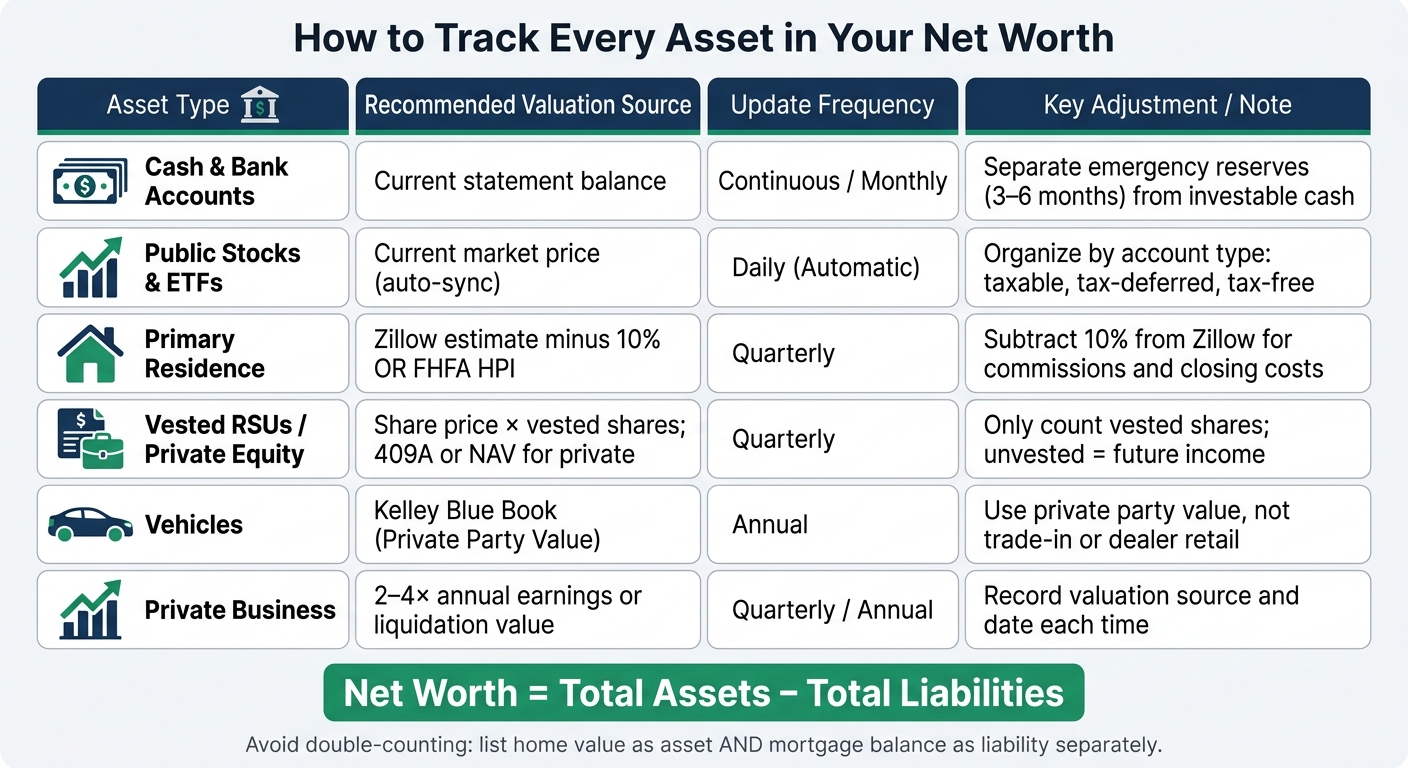

- Use consistent valuation methods: For example, estimate home values with tools like Zillow (minus 10% for selling costs) and adjust 401(k) balances for taxes. Stick to the same sources for accuracy over time.

- Leverage tools for simplicity: Platforms like Mezzi can securely sync your accounts, consolidate data, and track changes automatically - helping you save time and stay organized.

- Update regularly: Liquid assets and investments may need frequent updates (daily or monthly), while real estate and private equity can be reviewed quarterly.

Tracking your net worth helps you see progress, identify inefficiencies, and align with long-term goals like retirement. By using tools and consistent methods, you can simplify the process and gain clarity over your financial picture.

What to Include in Your Net Worth

Assets and Liabilities Defined

Your net worth is calculated as Assets – Liabilities. Assets represent everything you own that holds financial value, while liabilities are all the debts or obligations you owe.

When listing assets, they generally fall into three main categories:

- Liquid assets: These include checking accounts, savings accounts, money market funds, and CDs.

- Investment assets: This category covers brokerage accounts, retirement accounts like 401(k)s and IRAs, as well as stocks, bonds, and ETFs.

- Real estate: Include your primary residence, vacation homes, or any rental properties.

Liabilities, on the other hand, encompass obligations such as mortgage balances, auto loans, student loans, credit card debt, and any co-signed loans where you're legally responsible - even if someone else is making the payments.

The next step is deciding which assets and liabilities to include and determining their value.

How to Decide What to Include and How to Value It

Focus on including only those assets you could realistically sell in an emergency. Items like furniture, clothing, and most personal electronics are typically excluded.

For the assets you do include, how you value them is key:

- Primary Residence: Use a Zillow estimate and subtract 10% to account for commissions and closing costs.

- Retirement Accounts: Adjust balances to reflect post-tax values. For instance, a $500,000 401(k) might be reduced by 25–30% to estimate what you'd actually retain.

- Vested RSUs and Stock Options: Only count vested shares. Unvested equity should be treated as potential future income.

- Vehicles: Use the private party value from Kelley Blue Book (KBB) for accuracy.

Avoid double-counting. For example, if your home is worth $600,000 and you owe $350,000 on your mortgage, list $600,000 as an asset and $350,000 as a liability. Only the $250,000 difference contributes to your net worth.

Once you’ve identified which assets to include, it’s critical to maintain consistent valuation methods over time.

How to Keep Valuations Consistent

To simplify the process, tools like Mezzi can sync valuation sources for you. Consistency in valuation is more important than pinpoint precision. Switching valuation methods - such as using a Zillow estimate one quarter and a formal appraisal the next - can skew your trend line and make it harder to assess whether changes in net worth stem from actual performance or a shift in methodology.

Stick to one valuation source per asset type. For example, the FHFA Home Price Index (HPI) offers a reliable monthly indicator for adjusting property values between formal appraisals. For public stocks and ETFs, automated daily updates through Mezzi ensure your values remain current without requiring manual updates.

It’s also a good idea to record the source and date of each valuation. For example, note something like "KBB private party value on 06/12/26." Mezzi enables you to attach these details directly to each asset, providing a clear history of why and how your net worth has changed over time.

| Asset Type | Recommended Valuation Source | Update Frequency |

|---|---|---|

| Cash & Bank Accounts | Current statement balance | Monthly / Continuous |

| Public Stocks & ETFs | Current market price (auto-sync) | Daily |

| Primary Residence | Zillow (–10%) or FHFA HPI | Quarterly |

| Vested RSUs | Share price × vested shares | Quarterly |

| Vehicles | Kelley Blue Book (Private Party) | Annual |

| Private Business | 2–4× annual earnings or liquidation value | Quarterly / Annual |

How to Track Your Net Worth (Free Tool)

How to Build a Net Worth Tracking System

Net Worth Tracking: Asset Types, Valuation Methods & Update Frequency

Connect All Your Accounts to Mezzi

Managing finances across multiple institutions can quickly become overwhelming. On average, Americans have accounts at 5.3 different institutions, making manual tracking a daunting task. Mezzi simplifies this process by securely integrating with Plaid and Finicity (Mastercard). These connections are read-only, meaning Mezzi can access your balances and transactions but cannot move money or execute trades on your behalf.

You can link all types of accounts without sharing your login credentials, ensuring your information remains secure. Once connected, Mezzi consolidates everything into one place, giving you a streamlined view of your financial situation.

Build a Unified Net Worth Statement

After consolidating your accounts, the next step is creating a clear snapshot of your net worth. Mezzi does this automatically, organizing your accounts into a personal balance sheet. It categorizes liquid assets, investment portfolios, and liabilities without requiring manual input. Think of it as a financial roadmap that helps you navigate your money more effectively.

"A net worth statement is to personal finance what a compass is to navigation. It's not exciting, but essential." - Greg Nelson, Family Office Advisor, First National Wealth Management

This unified view helps you uncover important insights. By aggregating your accounts, Mezzi can highlight overlapping investments, identify areas of inefficiency, and even point out opportunities for tax optimization and high-net-worth investing strategies.

How Often to Update Your Net Worth

Not all assets require frequent updates. The key is to align update frequency with how often an asset's value is recalculated. Over-updating illiquid assets, for instance, can create unnecessary noise and lead to poor financial decisions.

Mezzi simplifies this process for liquid accounts by syncing them automatically. Public equities, ETFs, bonds, and cash balances update daily, ensuring your investment data stays current. For less liquid assets like real estate or private equity, a quarterly review is often sufficient. Tools like the FHFA House Price Index can guide these updates without adding unnecessary complexity.

| Asset Type | Update Frequency | How Mezzi Helps |

|---|---|---|

| Cash & Bank Accounts | Continuous / Monthly | Auto-syncs balances via Plaid |

| Public Stocks & ETFs | Daily (Automatic) | Real-time market price sync |

| Primary Residence | Quarterly | Manual input; FHFA HPI as a drift guide |

| Vested RSUs / Private Equity | Quarterly | Manual update based on 409A or NAV |

| Liabilities (Loans, Mortgages) | Continuous (Automatic) | Outstanding principal synced automatically |

For private assets, spend about 10 minutes each month reviewing and updating their values. Record any changes along with the source and date for accuracy. Mezzi allows you to attach these details directly to each asset, making it easy to track how and why your net worth changes over time.

How to Track Real Estate, Equity, and Cash

Each type of asset has its own valuation methods and tax considerations. Combining them without a clear approach can lead to a net worth calculation that’s less accurate or even misleading. Here's how to handle each category effectively.

How to Track Real Estate Equity

Many people calculate real estate equity by subtracting the mortgage balance from the market value. However, this method often overlooks key factors like cost basis adjustments, depreciation, and principal payments. A more precise method includes tracking your cost basis - the purchase price plus any capital improvements - and accounting for accumulated depreciation. For example, installing a new roof or renovating your kitchen increases your cost basis, while routine repairs do not. Residential rental properties, for instance, are typically depreciated over 27.5 years under MACRS tax rules.

To estimate your property’s value between formal appraisals, you can use a dual-anchor method. This involves pairing a primary anchor, like your most recent appraisal or a Broker Price Opinion, with a secondary drift anchor, such as the FHFA House Price Index. This approach helps keep your valuation aligned with market trends. Mezzi allows you to manually input these details, ensuring your net worth statement reflects a reliable number rather than relying solely on automated tools. Accurate real estate equity tracking contributes to a comprehensive net worth snapshot in Mezzi.

Next, let’s address equity holdings with similar attention to detail.

How to Track Equity Holdings

Equity accounts vary significantly in their tax implications. For example, taxable accounts and Roth IRAs result in different after-tax outcomes. To get a clearer understanding of what you truly retain, organize your holdings by account type: taxable, tax-deferred (like a traditional 401(k) or IRA), and tax-free (such as a Roth IRA).

Employer stock requires additional care. Update the value of vested RSUs to their fair market value and use current 409A or NAV data to assess private equity holdings. Mezzi’s X-Ray tool can help by scanning all your connected accounts to detect duplicate exposures. For instance, owning an S&P 500 index fund in your 401(k) and a large-cap growth ETF in your taxable account may result in overlapping investments and duplicate fees. Mezzi identifies these overlaps and offers rebalancing suggestions to streamline your portfolio. By tracking equity holdings at this level, your net worth statement in Mezzi reflects a more accurate after-tax position.

Finally, let’s ensure your liquid assets are properly categorized.

How to Track Cash and Short-term Reserves

When tracking cash, it’s important to separate emergency reserves from investable funds to avoid confusion. Divide your cash into two categories:

- Emergency reserves: Typically three to six months of expenses, ideally kept in a high-yield savings or money market account.

- Investable cash: Funds that are available for market or real estate investments.

This distinction ensures your net worth statement doesn’t confuse your financial safety net with funds meant for investment.

"A budget tells you where your money is going this month. Net worth tells you whether your money decisions are making you wealthier over time." - Surplus Budget

Mezzi simplifies cash tracking by syncing your checking, savings, and money market accounts through Plaid. This keeps your cash position updated without requiring manual input. Additionally, its AI-powered insights notify you of significant changes in your cash balance, helping you spot underutilized funds that could impact your long-term returns. Clear categorization of your cash completes the unified net worth view Mezzi offers across all asset types.

How to Analyze and Improve Your Net Worth Over Time

Set a Baseline and Track Changes

Start by documenting your entire net worth today - this includes all accounts, properties, and debts. This snapshot serves as your baseline, giving every future update a meaningful context. Tracking changes over time helps you understand your financial trajectory.

It’s important to distinguish between changes driven by market performance and those resulting from your own actions. For example, if your net worth increased by $18,000 last quarter, was it due to a rising portfolio value, or because you paid $12,000 toward your mortgage principal and added $6,000 to your 401(k)? Tools like Mezzi automatically categorize these changes, helping you see whether growth is coming from smart financial decisions or favorable market conditions. This clarity is crucial when deciding how to adjust your spending, investing, or borrowing habits.

For most people, updating net worth monthly strikes a good balance - it’s frequent enough to catch meaningful trends but avoids the distraction of daily market fluctuations.

By separating market-driven changes from your proactive contributions, you can better align your financial progress with your long-term goals.

Connect Net Worth Tracking to Long-term Goals

Knowing your net worth is helpful, but understanding how it aligns with your goals is what truly matters. Mezzi takes your net worth data and ties it directly to retirement planning. Instead of relying on generic calculators, it uses your actual account balances - like your 401(k), Roth IRA, real estate equity, and spending patterns - to answer questions like whether you can retire by 58.

"Net worth is still one of the best broad measures of household financial health." - Federal Reserve

Mezzi also allows you to benchmark your progress against reliable data, helping you identify areas where growth may be lagging. By linking your net worth to specific milestones, you can stay focused on achieving financial independence.

Cut Taxes and Manage Risk

Tracking your net worth is only part of the equation - protecting your wealth is equally essential. Mezzi provides insights that can strengthen your financial strategy by identifying opportunities to reduce taxes and manage risks.

For taxes, Mezzi highlights tax-loss harvesting opportunities throughout the year and offers advice on asset location - helping you decide which investments should go into tax-advantaged accounts like a Roth IRA versus taxable accounts. If you sell assets to capture a loss, Mezzi monitors the 30-day wash sale rule and notifies you when it’s safe to repurchase, ensuring compliance with tax laws.

On the risk side, Mezzi flags over-concentration in your portfolio, which is especially useful for tech employees heavily invested in RSUs. It also evaluates your portfolio’s overall health with a scoring system. For real estate investors, Mezzi tracks metrics like Loan-to-Value (LTV) and Debt Service Coverage Ratio (DSCR), alerting you when leverage levels suggest it might be time to consider refinancing.

Here’s a snapshot of the tax and risk issues Mezzi monitors:

| Risk or Tax Issue | What Mezzi Flags | Asset Class |

|---|---|---|

| Tax-loss harvesting | Year-round harvesting opportunities | Equities |

| Wash sale risk | Tracks 30-day window across accounts | Equities |

| Asset location | Optimizes account placement for tax savings | All holdings |

| Over-concentration | Alerts for single-stock or sector exposure | Equity (RSUs) |

| LTV/DSCR thresholds | Flags leverage and refinancing opportunities | Real Estate |

Conclusion: Start Tracking Your Net Worth with Mezzi

Keeping tabs on your net worth - spanning real estate, investments, and cash - doesn't have to be overwhelming. The concept is straightforward: link all your accounts, use consistent valuations, and regularly review your net worth to ensure you're on the right track.

The challenge comes from the fact that different assets update on varying schedules. For example, rental properties, 401(k)s, brokerage accounts, and savings accounts don’t sync up perfectly. Trying to manage this manually can lead to missed details, like forgetting an old retirement account, underestimating home equity, or overlooking growing debt.

Mezzi simplifies this process by securely consolidating your accounts through read-only access. It provides a clear net worth statement, tracks real estate data, highlights potential tax benefits, and aligns with your retirement objectives - all without handling any money transfers. Currently, over 50,000 users across the U.S. and Canada rely on Mezzi to manage more than $40 billion in assets.

Experts emphasize the importance of this approach:

"Your income tells you the rate at which money enters your life. Your net worth tells you how much of it you've actually kept, grown, and converted into lasting financial security." – Avenue Editorial

Despite this, only 33% of Americans have a long-term financial plan with clear savings and investment goals. Studies show that households actively tracking their net worth are more likely to feel financially secure and prepared for unexpected expenses. A consistent and clear system can make all the difference - and Mezzi is designed to be that system. Start consolidating your accounts with Mezzi today and take a step toward greater financial clarity.

FAQs

Should I track net worth pre-tax or after-tax?

Tracking your net worth after-tax provides a clearer understanding of your financial situation by factoring in tax obligations. This method gives a more realistic view of the actual value of your assets and liabilities, which may help guide more informed financial choices.

How do I value private equity and unvested RSUs?

To estimate the value of private equity, rely on the latest fair market value provided by your investment platform or recent appraisals. For unvested RSUs, adjust their value on vesting dates according to the stock's fair market value at that time. Be sure to include vested RSUs when calculating your net worth. Tools such as Mezzi can assist in tracking these valuations over time, offering a clearer picture of your overall financial standing.

What should I do if my net worth swings a lot month to month?

If your net worth changes frequently, it’s important to adjust how often you update valuations for different assets. For instance, real estate values might only need updates quarterly or annually - unless something major happens. Keep an eye on trends monthly to avoid reacting too strongly to short-term shifts. Also, make sure to document your valuation methods to keep things accurate. During times of market volatility, you might want to temporarily update valuations more often to get a clearer picture of your financial standing.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.