If you want into many private deals, the first question may be simple: do you meet the SEC’s accredited investor rules? In most cases, that may come down to one of a few tests: income above $200,000 alone or $300,000 with a spouse or spousal equivalent for the last 2 years, net worth above $1,000,000 excluding your primary home, or a qualifying license like Series 7, 65, or 82.

Here’s the short version:

- Accredited investor status may affect access, not investment quality.

- The main tests are income, net worth, licenses, and some entity rules.

- Timing matters: qualification is generally judged on the investment date.

- Rule 506(b) offerings may allow self-certification.

- Rule 506(c) offerings usually require added verification, often with documents from the last 90 days.

- Common proof may include tax returns, W-2s, brokerage statements, credit reports, or a third-party letter from a CPA, attorney, or RIA.

- Your primary residence usually does not count toward the $1,000,000 net worth test.

A separate point that many people miss: being accredited may only mean you’re allowed to invest. It may say nothing about whether a hedge fund, startup, syndication, or private placement fits your cash needs, risk level, or total portfolio.

If I were trying to check my status fast, I’d start by matching myself to the cleanest path, gathering the records tied to that path, and then confirming whether the deal uses 506(b) or 506(c). That may tell me how much proof the issuer is likely to request.

How to Verify Accredited Investor Status for 506(c) Deals

What an accredited investor is under U.S. law

Rule 501(a) of Regulation D lays out who may qualify as an accredited investor for certain private securities offerings that are exempt from SEC registration. The SEC uses this standard for people who may be able to assess risk on their own and may be able to absorb a loss without the added protections that come with SEC registration. In plain English, this standard may shape which private deals you’re allowed to access.

Accredited status grants access; it does not judge the investment. The SEC does not vet private investments or vouch for them. Qualifying simply means you may be eligible to participate. It says nothing about whether a specific deal may be sound, suitable for your situation, or likely to return anything at all.

The main question is whether your income, assets, or professional status may meet one of the SEC’s tests. It also helps to know that a qualified purchaser is a separate, higher standard used for a narrower group of private funds.

Why the designation matters in private markets

You’ll usually see this requirement in private equity, venture capital, hedge funds, private placements, and real estate syndications. These investments often come with less disclosure, lower liquidity, longer holding periods, and higher minimums. That may affect how people size up the tradeoffs, just as much as the question of whether they qualify.

Next, we’ll break down the income, net worth, and other paths that may qualify you.

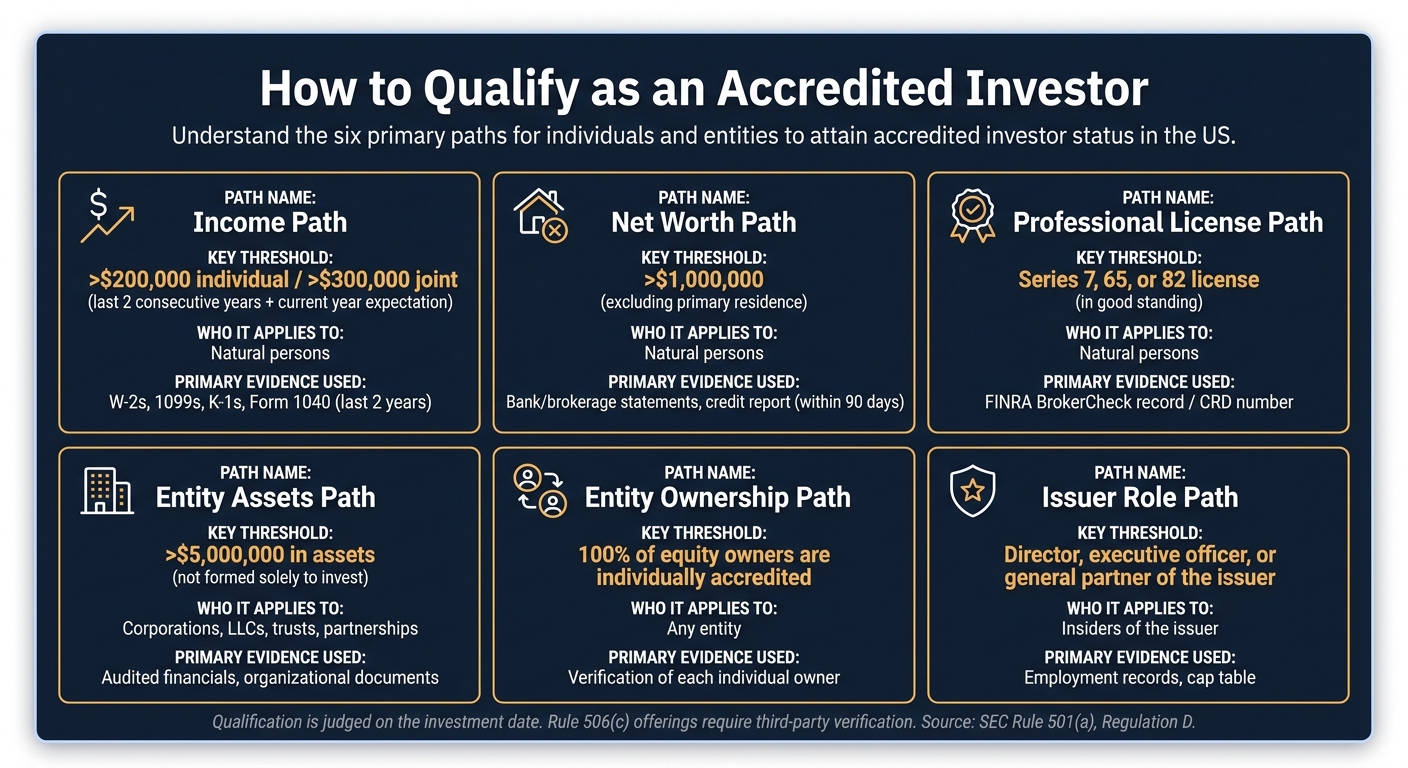

The main ways individuals and entities can qualify

Accredited Investor Qualification Paths: Requirements & Proof

Eligibility is judged on the investment date, not at year-end or when taxes are filed.

Income test: more than $200,000 individually or $300,000 jointly

Under the income path, a person may qualify by earning more than $200,000 individually or more than $300,000 combined with a spouse or spousal equivalent in each of the two most recently completed calendar years, and by expecting to reach that level again this year. Each prior year has to clear the line on its own. A high-income year may not be averaged with a lower one.

Qualifying income may include wages, self-employment income, capital gains, rent, and business distributions. Issuers often ask for Forms W-2, 1099, Schedule K-1, and Form 1040 for the two most recent years, plus a signed written statement about current-year expectations. If an investment happens before the latest return is filed, the usual approach may be to use the two earlier years' returns along with that current-year statement.

If this route doesn't fit, the next common path may be net worth.

Net worth test: more than $1,000,000 excluding a primary residence

A person's net worth may need to exceed $1,000,000, either alone or jointly with a spouse or spousal equivalent, at the time of purchase. The primary residence does not count toward that total. Mortgage debt on that home is also left out up to the home's fair market value. Any underwater portion counts as a liability, and new home debt taken on within 60 days of the investment also counts.

Assets that may count toward the $1,000,000 threshold include bank accounts, brokerage accounts, retirement accounts such as 401(k)s and IRAs, other investments, vehicles, and secondary real estate. Verification often includes recent bank and brokerage statements, plus a credit report to show liabilities. For Rule 506(c) offerings, that paperwork generally may need to be dated within 90 days of the investment.

If neither financial path fits, another route may come from a license or a role tied to the issuer.

Other qualification routes: professional licenses, issuer roles, and entities

People with a Series 7, Series 65, or Series 82 license in good standing may qualify as accredited investors regardless of income or net worth.

Certain insiders may also qualify. That group includes directors, executive officers, and general partners of the issuer, and the qualification applies to that issuer's offerings.

Entities may qualify too. One path applies to entities with more than $5,000,000 in assets, as long as they were not formed just to buy the securities. Another path may apply when all equity owners are accredited.

| Path | Key Threshold | Who It Applies To | Primary Evidence Used |

|---|---|---|---|

| Income | >$200,000 (individual) / >$300,000 (joint) | Natural persons | W-2s, 1099s, K-1s, Form 1040 (last 2 years) |

| Net Worth | >$1,000,000 (excluding primary residence) | Natural persons | Bank/brokerage statements, credit report |

| Professional License | Series 7, 65, or 82 in good standing | Natural persons | FINRA BrokerCheck record |

| Entity Assets | >$5,000,000 in assets | Corporations, LLCs, trusts, partnerships | Audited financials, organizational documents |

| Entity Ownership | 100% of equity owners are accredited | Any entity | Verification of each individual owner |

| Issuer Role | Director, executive officer, or general partner | Insiders of the issuer | Employment records, cap table |

Next, use these paths to gather the records issuers typically ask for.

How to verify your accredited investor status

Now that you know which path may fit, the next step is proving it before you invest.

Step 1: match your situation to the right qualification path

Start with the path you may document most cleanly.

If you’re using the income path, that may work best when two years of tax records are above the threshold. The net worth path may be simpler when your assets and liabilities are easy to show. The license, issuer-role, and entity paths usually depend on status, ownership, or entity records. For issuer-role and entity paths, issuers may ask for proof of status, assets, or ownership.

Step 2: gather the documents issuers typically request

The paperwork usually depends on the path you’re using.

For the income path, issuers often ask for the last two years of Forms W-2, 1099s, Schedule K-1s, and Form 1040, plus a signed written statement about your current-year income expectations.

For the net worth path, they may request recent bank, brokerage, and retirement account statements, along with a current credit report so they may review your liabilities.

For the professional license path, issuers usually ask for your FINRA CRD number. They may use it to check your active status through FINRA BrokerCheck or the SEC's Investment Adviser Public Disclosure system.

For entities, the usual request includes organizational documents and financial statements showing assets or investments above $5 million, or proof that all equity owners are individually accredited.

One practical note: you can usually redact your Social Security number and full account numbers from financial statements before sending them, as long as your name and the figures that matter stay visible.

Step 3: choose a verification method and keep records

The verification standard may depend on the exemption being used. Rule 506(b) offerings typically allow self-certification. Rule 506(c) offerings require the issuer to verify your status.

| Verification Method | Who Performs It | Typical Documentation Burden | Where It's Commonly Used |

|---|---|---|---|

| Self-Certification | Investor | Low: checkbox/questionnaire and signature | Rule 506(b) offerings |

| Review by the fund or platform | Fund/platform compliance team | High: tax returns, bank statements, and credit reports | Rule 506(c) offerings; smaller issuers |

| Third-Party Letter | CPA, attorney, or RIA | Medium: professional reviews records and issues a letter | Rule 506(c) offerings; investors who want more privacy |

| Verification Service | Specialized platform (e.g., Verify Investor, Parallel Markets) | Medium: document upload to a secure portal | Rule 506(c) offerings; high-volume platforms |

For net worth reviews and many third-party letters, issuers often want documents dated within the last 90 days.

It may help to keep copies of every statement, letter, certification, and approval. If you invest again later, you may only need an updated certification.

Verification may confirm eligibility for one specific offering. It does not replace investment due diligence.

Limits of accredited status and how Mezzi can help you assess eligibility alongside your full financial picture

Once you verify eligibility, the next step is simpler to say than to sort out: does the investment belong in your portfolio? Accredited status only confirms that you may invest. It does not judge the investment itself.

Private deals may be opaque, illiquid, and concentrated. You may have less information to judge valuation and risk. These investments are also often hard to sell, which may create liquidity constraints and concentration risk at the same time.

In borderline cases, a qualified CPA, securities attorney, or compliance professional may help confirm whether you actually meet the standard before you commit capital. That may come up if your income varies, you combine income with a spouse or spousal equivalent, or you need to value something less straightforward, like an underwater mortgage or pension. After that, it may make sense to look at how the deal fits into your broader balance sheet.

Eligibility answers one question. Portfolio fit answers the more important one.

Once you know you qualify, the next issue is whether the deal fits your finances. Mezzi is designed to help you judge fit, not just eligibility. As an SEC-registered fiduciary with read-only access to your connected accounts, Mezzi may help you track:

- Net worth

- Investable assets

- Liquidity needs

- Concentration risk in context, including whether your primary residence may need to be excluded from the calculation

Before you commit to a private deal, you may also see how it may affect your broader portfolio allocation and tax situation.

Accredited status answers can you invest. Tools like Mezzi may help you answer should you invest.

FAQs

Can I qualify if my income changes year to year?

Yes - under the income test, you may qualify only if you earned more than $200,000 on your own, or $300,000 with a spouse or spousal equivalent, in each of the two most recent calendar years and reasonably expect the same this year.

If your income fluctuates and you don’t meet that three-year pattern, you may not qualify through income. You may still qualify through the separate $1 million net worth test or certain professional licenses.

Does my 401(k) count toward net worth?

Yes. Your 401(k) may count toward net worth when determining accredited investor status.

People often include most other financial assets too, such as IRAs, pension values, cash, investments, and other personal property. Then they may subtract liabilities, while excluding a primary residence and the mortgage debt tied to it.

How often do I need to verify my status?

It may depend on the offering and your history with the issuer.

Under Rule 506(c), issuers may need to take reasonable steps to verify your status. That often means reviewing documents such as tax forms or financial statements from the prior three months.

If the same issuer has already verified you and knows of no changes, a written representation may be enough. That representation remains valid for five years from your original verification date.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.