A personal balance sheet may give you one number that scattered account logins don’t: your net worth. In plain terms, I’d sum up everything I own, subtract everything I owe, and use that snapshot to see my cash, investments, property, and debt in one place.

Here’s the short version:

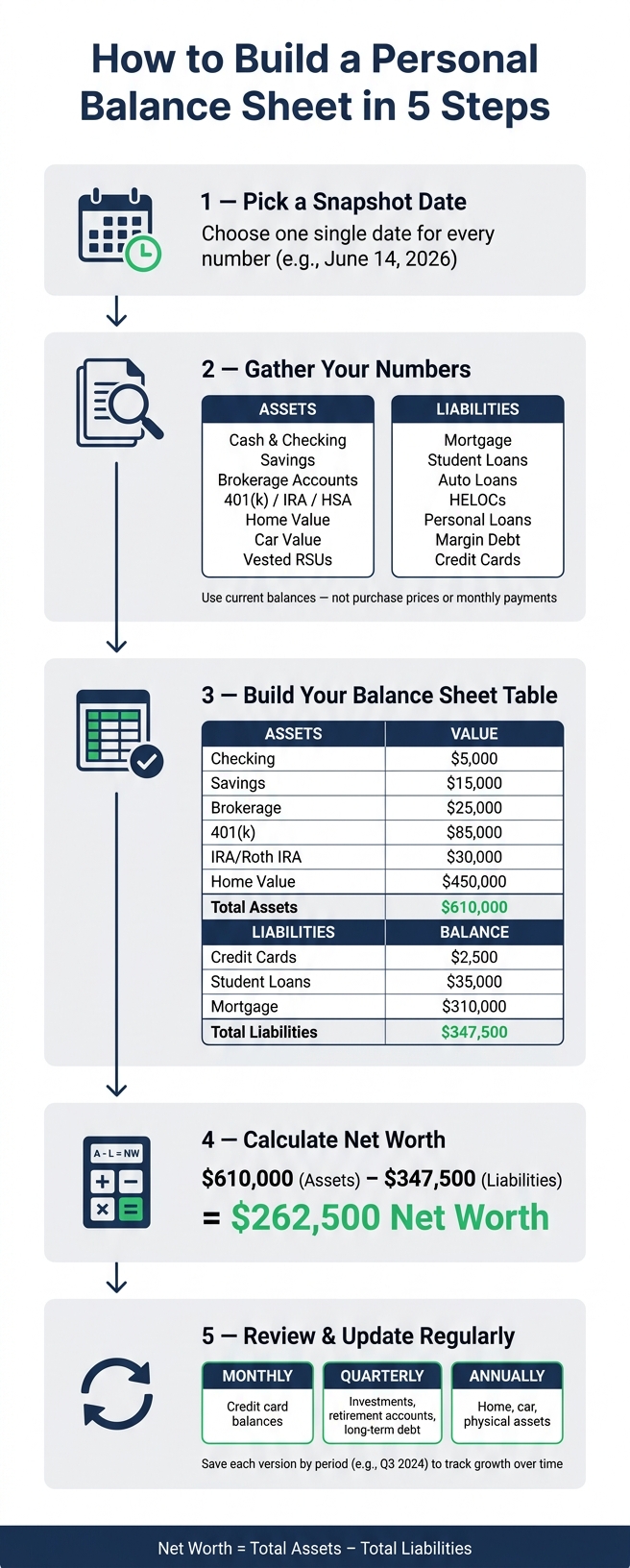

- Pick one date for every number, such as June 14, 2026

- List assets like cash, brokerage accounts, 401(k)s, IRAs, home value, car value, and vested RSUs

- List liabilities like credit cards, student loans, auto loans, HELOCs, personal loans, margin debt, and mortgages

- Use current values, not purchase prices or monthly payments

- Calculate net worth with: Assets - Liabilities

- Review it monthly, quarterly, or yearly so changes may be easier to spot

A few things stand out from the article:

- A $450 car payment may say little about your finances on its own, but the full loan balance may say more

- A home worth $450,000 with a $310,000 mortgage may show why listing both numbers side by side matters

- In the sample sheet, $610,000 in assets minus $347,500 in liabilities comes to $262,500 in net worth

If I wanted one clean view before a home purchase, refinance, job change, or new investment, this kind of snapshot may be one of the simplest ways to get it.

How to Build a Personal Balance Sheet in 5 Steps

Personal Balance Sheet: Measuring Your True Net Worth and Taking Control of Your Financial Life

Step 1: gather your numbers before you build

Pull together every balance first. Then move straight into your asset list.

Collect balances for cash, investments, retirement accounts, and property

Log in to each bank and brokerage account and write down the current balance - not what you deposited and not what you paid at the start.

That means checking:

- Checking and savings accounts

- Brokerage accounts

- 401(k)s

- IRAs

- HSAs

If you own individual stocks or crypto, use the current market value instead of cost basis.

For real estate, skip the purchase price. A current market estimate may be a reasonable starting point. For a car, use the private-party resale value rather than the trade-in value. If you have vested RSUs, include their current value too.

All of these go on the asset side of your balance sheet.

Collect payoff balances for credit cards, student loans, mortgages, and other debt

For each debt, use the total outstanding balance, not the monthly minimum payment.

A $450 monthly car payment may tell you almost nothing about what you still owe. The payoff balance does. Log in to each lender portal, or check your latest statement, and note the remaining balance for:

- Mortgages

- Student loans

- Auto loans

- HELOCs

- Personal loans

- Margin debt

- Credit cards

For credit cards, record what you currently owe, not your credit limit.

Skip regular monthly bills like rent and utilities. Only list balances that are still owed. These go on the liability side.

Pick a tracking method you will actually update

The simplest options are a spreadsheet or a connected tool like Mezzi.

A spreadsheet gives you full control over categories and formulas, and you keep control of the data. The tradeoff: each update may require logging in to every account and entering balances by hand.

A connected tool like Mezzi links to your accounts with read-only access, so balances may sync on their own and you may get the full picture without pulling each number manually. That may be useful if your accounts sit across several institutions.

Pick one method and update it on a steady schedule.

Once you have the numbers, sort them into assets and liabilities.

Step 2: list assets and liabilities in a clear structure

Now that you have the numbers, put them into a simple balance sheet.

Record assets by category and separate liquid from illiquid holdings

Start by grouping assets based on how easy they may be to access.

Checking and savings accounts, money market funds, CDs, and taxable brokerage accounts are usually the most accessible. Retirement accounts like 401(k)s, IRAs, Roth IRAs, and HSAs also belong on the balance sheet, but they may be less liquid because withdrawal rules may apply. Homes, rental property, vehicles, and other personal property usually take more time to sell.

This split does more than organize the page. It may show both your net worth and how much financial flexibility you may have. Money tied up in a house or retirement account may be less available for near-term spending.

For illiquid assets, use one conservative valuation method across the board. And leave out ordinary household items unless they may have meaningful resale value.

Record liabilities by balance owed and group short-term and long-term debt

Do the same thing with debt. Split liabilities into short-term and long-term buckets.

Short-term liabilities may include:

- Credit card balances

- Medical bills

- Buy-now-pay-later balances

Long-term liabilities may include mortgages, student loans, and auto loans.

For each liability, list:

- Balance owed

- Interest rate

- Minimum payment

That extra detail may make the balance sheet more useful later, especially if you want to review cash flow pressure or compare debt costs.

Use a simple assets-versus-liabilities table

Here’s what a clean, straightforward balance sheet may look like in practice:

| Category | Item | Value / Balance |

|---|---|---|

| Liquid Assets | Checking Account | $5,000 |

| Savings Account | $15,000 | |

| Brokerage Account | $25,000 | |

| Investable Assets | 401(k) | $85,000 |

| IRA / Roth IRA | $30,000 | |

| Illiquid Assets | Home Value (Conservative) | $450,000 |

| Short-Term Liabilities | Credit Card Balances | $2,500 |

| Long-Term Liabilities | Student Loans | $35,000 |

| Mortgage Balance | $310,000 | |

| Summary | Total Net Worth | $262,500 |

Listing the home and mortgage separately may make the equity easier to see.

From there, total each side and subtract liabilities from assets to calculate net worth. Once the table is filled out, add up total assets and total liabilities to find the final number.

Step 3: calculate net worth and read the result

Apply the formula: net worth = total assets minus total liabilities

Once your table is done, add up both sides and subtract liabilities from assets. The formula is simple: Total Assets − Total Liabilities = Net Worth.

Using the example above, that comes to $610,000 in total assets minus $347,500 in total liabilities. The result: $262,500 in net worth.

Use one date for every number. If the dates are mixed, the snapshot may give a skewed picture.

A negative or modest net worth may be a starting point, not a judgment. After you run the math, the next step is to look at what may be driving the result.

Check your snapshot for liquidity, debt load, and concentration risk

Now read the snapshot, not just the total.

- Liquidity: This shows how much money you may access fast, such as cash or cash-like accounts.

- Debt load: This shows which balances may take up the most space on your liability side.

- Concentration risk: This shows whether a large share of your wealth may sit in one asset.

That baseline may become more useful when you update it on a set schedule.

Keep it current and use it to make better decisions

Update monthly or quarterly and track changes over time

Once the snapshot is built, the next step is keeping it current. A balance sheet may be most useful when it reflects recent choices instead of old numbers.

A simple rhythm may look like this:

- Review short-term items like credit card balances monthly

- Revisit investments, retirement accounts, and long-term debt quarterly

- Refresh personal property - your home, car, or other physical assets - annually or right after a major purchase

A few events may also call for an immediate update. A large market swing, an RSU vesting event, a home purchase, or a major debt paydown may all change net worth in a meaningful way. If you wait too long, you may end up making choices based on stale numbers.

It may also help to save each version by period - like "Q3 2024" - instead of overwriting the old one. That gives you an easy way to compare changes over time. At that point, net worth may become more than a static number. It may start to work like a decision tool.

"Updating your balance sheet every quarter or year allows you to visually track your net worth growth, which is a huge motivator." - Spencer Lanoue, Product Builder

Use one current view to support bigger financial decisions

A current balance sheet may be useful because it gives you one baseline before a major money decision. That may include buying a home, refinancing debt, changing jobs, adjusting your savings plan, or sizing a new investment.

Without a current baseline, major decisions may turn into guesswork. With one up-to-date view, you may compare a refinance, home purchase, job change, or new investment against your actual financial position. It may also help you set spending and savings targets based on current and expected liquidity.

As Andrew Izyumov, CFA, puts it:

"Make better investment decisions (allocation, sizing, exit) in the context of the whole portfolio, improving your asset allocation strategy." - Andrew Izyumov, CFA

A consolidated view may make it easier to move forward without wondering whether your numbers are out of date.

Conclusion: the steps and why they are worth doing

The process comes down to five repeatable steps: pick a single snapshot date, gather current balances across all accounts, list assets and liabilities in a clean structure, subtract liabilities from assets to get your net worth, and update on a consistent schedule.

"A personal balance sheet isn't just a document, it's a tool that provides clarity and direction." - Spencer Lanoue, Product Builder

The payoff may be simple but useful: faster clarity on where you stand, a steady base for bigger financial decisions, and a way to spot issues - like liabilities growing faster than assets - before they build up. That kind of control may be hard to get from a scattered set of account logins.

FAQs

What should I leave off a personal balance sheet?

Leave out anything that doesn’t have a clear dollar value or doesn’t reflect your financial position. That may include personal items with little resale value, along with income and monthly expenses that aren’t part of net worth.

Instead, focus on assets and liabilities you can put a number on, such as cash, investments, real estate, loans, and credit card debt.

How do I value my home or car accurately?

Use current market value, not the original purchase price or an optimistic estimate.

For your home, look at a recent appraisal, online estimates, or similar sales nearby, and stay conservative. For your car, check Kelley Blue Book, CarGurus, or a similar source to find the private-party or trade-in value based on what it may realistically sell for today.

What if my net worth is negative?

A negative net worth may be common, especially early in your career or while paying down student loans. It may not mean you're failing.

It may help to think of net worth as a snapshot of where you are right now, not a verdict on your financial health. A personal balance sheet is mainly a way to track change over time as liabilities may go down and assets may grow.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.