Want the short answer? I may calculate my lifetime wealth ratio by dividing my current net worth by my total lifetime gross income.

That gives me one simple number that may show how much of what I’ve earned still remains today. A higher ratio may suggest I’ve kept more of my income as wealth. A lower or negative ratio may simply reflect an early career stage, debt, or a high-cost period.

Here’s the whole idea in plain English:

- Formula: Net Worth ÷ Lifetime Gross Income

- Net worth: what I own minus what I owe

- Lifetime gross income: total pre-tax earnings, plus items like inheritances if I include them on both sides

- Best use: track it once a year using the same method

- Main point: the trend over time may say more than one one-year number

A quick example:

- If my lifetime gross income is $1,500,000

- And my net worth is $900,000

- My lifetime wealth ratio may be 0.60, or 60%

That may sound simple. And it is. The hard part usually isn’t the math - it may be pulling the numbers in a consistent way from Social Security records, tax forms, account balances, home value, and debts.

Below, I break down what to count, what to leave out, how some people gather the numbers in the U.S., and how a low, rising, or negative ratio may be read in context.

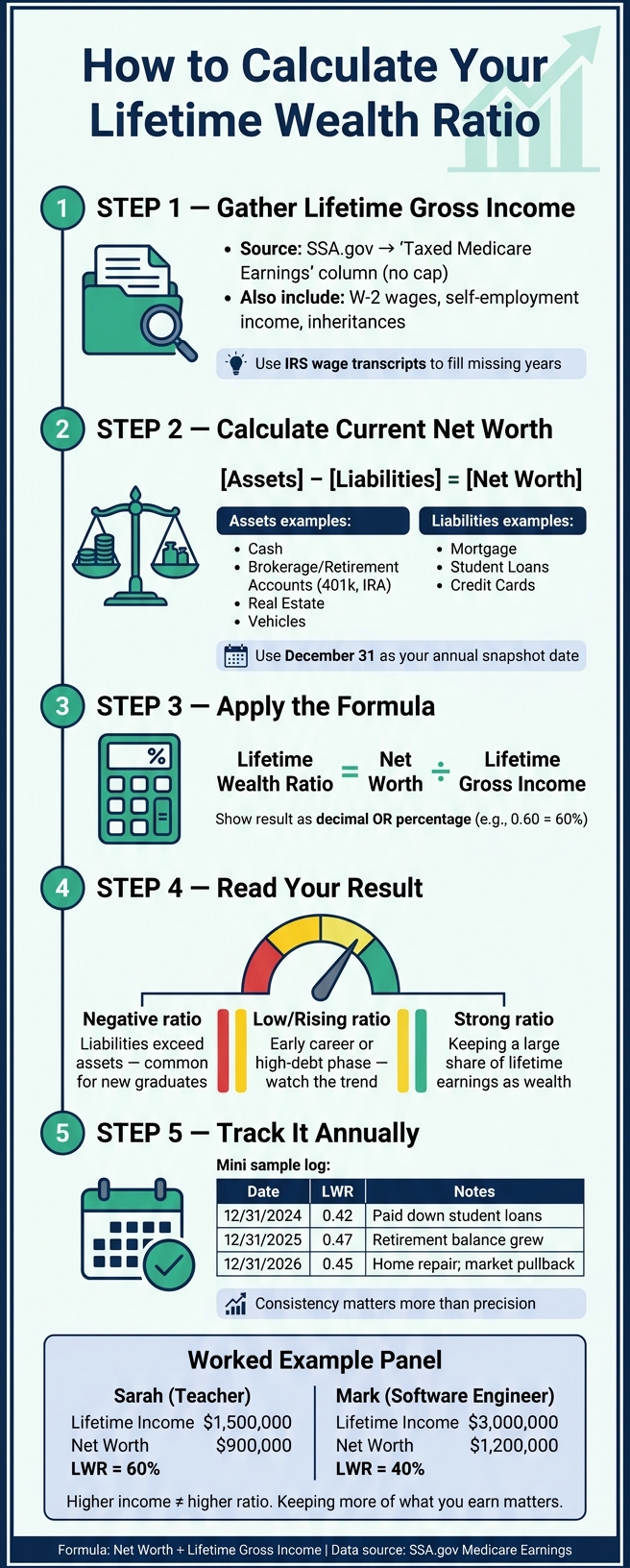

The formula and what goes into it

To calculate your ratio, start with two inputs: lifetime gross income and current net worth.

Lifetime Wealth Ratio = Net Worth ÷ Lifetime Gross Income

You may show the result as a decimal or a percentage. For example, 0.25 and 25% mean the same thing.

What counts as lifetime gross income

Lifetime gross income refers to all pre-tax income and major receipts you choose to include. That may include:

- W-2 wages, salaries, bonuses, commissions, and tips

- Self-employment income

- Inheritances

If you include an inheritance in net worth, include it in lifetime income as well.

What counts as current net worth

Net worth = assets minus liabilities.

Assets may include cash, investment accounts, property, and other items of value, such as:

- Cash and savings accounts

- Brokerage and retirement accounts (401(k)s, IRAs)

- Real estate, including your primary home and rentals

- Vehicles and other valuable personal property

Liabilities may include debts such as:

- Mortgages, student loans, credit card balances, and other personal loans

Leave out unvested equity and expected inheritances.

How to handle joint accounts and hard-to-value assets

If you share finances with a spouse or partner, it may make sense to pick one method and stick with it: individual or household. For a household ratio, combine both partners' lifetime earnings in the denominator and use total joint assets and liabilities in the numerator.

For private business interests, private equity stakes, or other illiquid holdings, some people use a conservative current value and apply the same valuation method each year.

Next, gather those numbers from records and account statements.

How to gather your numbers in the United States

You only need two inputs: lifetime earnings and current net worth.

Estimate lifetime earnings from Social Security and tax records

Start with the lifetime income number from the formula above. Open your my Social Security account at ssa.gov and pull the Medicare earnings column for each year. Social Security earnings are capped. Medicare earnings are not.

"I used 'your taxed Medicare earnings' instead of 'your taxed Social Security earnings' because the former has no limit and provides a more accurate overview." - J.D. Roth, Founder, Get Rich Slowly

If recent years are missing, IRS wage transcripts may help fill those gaps. For older missing years, some people estimate from average annual income. If you were self-employed, old Form 1040s and Schedule C filings may be the main source.

Build a current net worth snapshot

Pick one as-of date - December 31 works well - and record each account balance and debt balance as of that date. For real estate, use market value minus the remaining mortgage balance. Mezzi may pull connected accounts into one current view.

Use a spreadsheet or calculator

A simple setup may look like this:

| Tab | Key Fields | Source |

|---|---|---|

| Lifetime Earnings | Year, Medicare earnings, Windfalls/Inheritances | SSA.gov, tax returns |

| Net Worth Snapshot | Assets and liabilities | Account statements, Mezzi |

| Summary | Total Lifetime Earnings, Total Net Worth, Lifetime Wealth Ratio | Calculated via formula |

In the Summary tab, one formula does the work: =Total Net Worth / Total Lifetime Earnings.

You may want to refresh the earnings tab once a year, then recalculate.

With both totals entered, the next step is the calculation.

How to calculate and read your ratio

How to Calculate Your Lifetime Wealth Ratio: Step-by-Step Guide

Step-by-step calculation with worked examples

Once you have your numbers, the formula is simple:

Lifetime wealth ratio (LWR) = current net worth ÷ total lifetime gross income

Use the totals you already pulled together. You may show the result as a decimal or as a percentage.

- Add up your total lifetime gross income

- Calculate your current net worth

- Divide net worth by lifetime gross income

Use the same inputs each year. That way, changes in the ratio may reflect actual progress instead of inconsistent math.

Here’s a simple worked example:

| Scenario | Lifetime Gross Income | Current Net Worth | LWR |

|---|---|---|---|

| Sarah, teacher | $1,500,000 | $900,000 | 60% |

| Mark, software engineer | $3,000,000 | $1,200,000 | 40% |

Higher income does not always lead to a higher ratio. In this example, Sarah’s ratio is stronger because she kept a larger share of what she earned.

Your own ratio may look very different, but the basic reading stays the same: it shows how much of your income still remains as wealth.

You may apply the same framework to your own numbers, then compare the result from one year to the next.

How to read a low, rising, or negative ratio

The number by itself may matter less than the direction over time.

A low ratio does not mean failure on its own. It may be common early in a career, especially when debt remains high and assets have had less time to compound. For many people, the most useful comparison may be their own year-over-year trend.

A negative ratio means liabilities are higher than assets, so net worth falls below zero. That may happen for recent graduates with student loans or for people carrying a large amount of consumer debt.

A rising ratio may be the main signal to watch. It often suggests someone may be saving more, paying down debt, and giving compounding more time.

The ratio may work best as a personal benchmark. Age, housing costs, and career stage may all change what a solid ratio looks like, so comparing your current result with your past result may be more useful than chasing someone else’s number.

What drives the ratio up or down over time

A few main factors may explain why one person’s ratio rises faster than another’s.

| Driver | How it moves the ratio | What to review |

|---|---|---|

| Savings rate | May improve the ratio by growing net worth | Monthly budget and automated transfers |

| Investment returns | May improve the ratio through compounding | Asset allocation and risk tolerance |

| Fees | May reduce the ratio by lowering net growth | Expense ratios and management fees |

| Taxes | May reduce the ratio by lowering what remains to compound | Tax-loss harvesting and account location |

| Debt decisions | May reduce the ratio by increasing liabilities | Interest rates and debt paydown priority |

| Housing costs | Mixed; equity may help, but interest and maintenance may offset it | Mortgage terms and total cost of ownership |

These levers may help explain why the ratio changes from year to year.

Use the ratio as an annual benchmark

Track the trend and keep your inputs consistent

Once you know the formula, make it a yearly habit. The point of the lifetime wealth ratio may come from using the same formula, the same inputs, and the same timing over many years. One calculation gives you a baseline. Repeating it each year may give you a clearer view of progress.

Pick one date and stick with it each year - December 31 or your birthday both work well. On that date, recalculate the ratio using the SSA "Taxed Medicare Earnings" column in your Social Security record for each year, and update your net worth using the same accounts. The goal here may be consistency, not perfect precision.

It may help to save each year's result in a dated table and add a short note beside it. Those notes may give context to changes in the ratio, whether they were associated with income, debt, spending, or investment growth.

Here’s a simple way to log it:

| Date | Lifetime Wealth Ratio | Notes |

|---|---|---|

| 12/31/2024 | 0.42 | Paid down student loans |

| 12/31/2025 | 0.47 | Higher income; retirement balance grew |

| 12/31/2026 | 0.45 | Home repair costs; market pullback |

Early gains may look slow. Compounding may show up more clearly later.

If you track the ratio the same way every year, the trend may become the main signal.

Conclusion: key points to remember

The lifetime wealth ratio uses one formula: current net worth ÷ total lifetime gross income.

This ratio may work best when used alongside yearly net worth tracking and tax-aware planning. If the method stays the same from year to year, the annual trend may be more useful than any single result.

"The first calculation sets your baseline. Every later one shows your trajectory." - Marcus, Author, Simple Money Habits

FAQs

Should I use gross or net income?

Use gross (pre-tax) income for your lifetime earnings. Gross earnings are the standard, most accessible figure for calculating your Lifetime Wealth Ratio.

In many cases, you may find this on your Social Security statement under “Earnings Taxed for Medicare.” That amount may give you a steady baseline for comparing your total past earnings with your current net worth.

What if my net worth is negative?

If your net worth may be negative, your lifetime wealth ratio may be negative too. That's simply a starting point, not necessarily a sign of poor financial decisions or a bad overall position.

Many people have student loans, credit card balances, or other liabilities that may create negative net worth, especially early in their careers. It may make sense to treat that number as a baseline for tracking progress over time as debt goes down and wealth builds.

Should I calculate this individually or as a household?

You may calculate your lifetime wealth ratio on your own or at the household level. For many people, the household version may offer a fuller picture of shared financial progress, saving, and investing.

Whichever route you use, keep the inputs consistent: net worth and lifetime income should both reflect the same financial unit.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.