An NQDC balance may look like extra retirement money, but it may act more like a future paycheck tied to your employer. The short version: track each deferral by year, vesting date, payout trigger, payout form, and tax year - then line that up with salary, equity, retirement income, and employer stock exposure.

Here’s the core idea in plain English:

- NQDC may not work like a 401(k). It may stay on your employer’s balance sheet, and you may be an unsecured creditor if the company runs into trouble.

- Taxes may show up at more than one point. FICA may apply at vesting, while income tax may apply when money is paid out.

- Your election timing may matter a lot. Section 409A may limit when you can change payout timing, and mistakes may lead to current tax plus a 20% extra federal tax.

- Each deferral year may need its own record. One tranche may pay at retirement, another on a fixed date, and another in installments.

- Payout timing may shape your tax bill. A lump sum in your final working year may stack on top of salary, bonus, and RSUs. Installments may spread income across later years.

- Employer risk may be bigger than it looks. If NQDC, unvested equity, company stock, and pay all point to one employer, your net worth may be more tied to that company than you think.

A few facts stand out:

- 401(k) catch-up limits for 2026 may be capped, while NQDC deferrals may be plan-defined and often much higher.

- Public-company specified employees may face a 6-month payout delay after separation from service.

- Installments over 10+ years may have a different state-tax result in some cases.

- Some planners use a rough cap of 1 to 2 years of pay for NQDC exposure, though that may vary by person.

If I were boiling the full article down to one sentence, it would be this: treat NQDC like a dated cash-flow schedule with tax rules and company risk attached - not like a simple account balance.

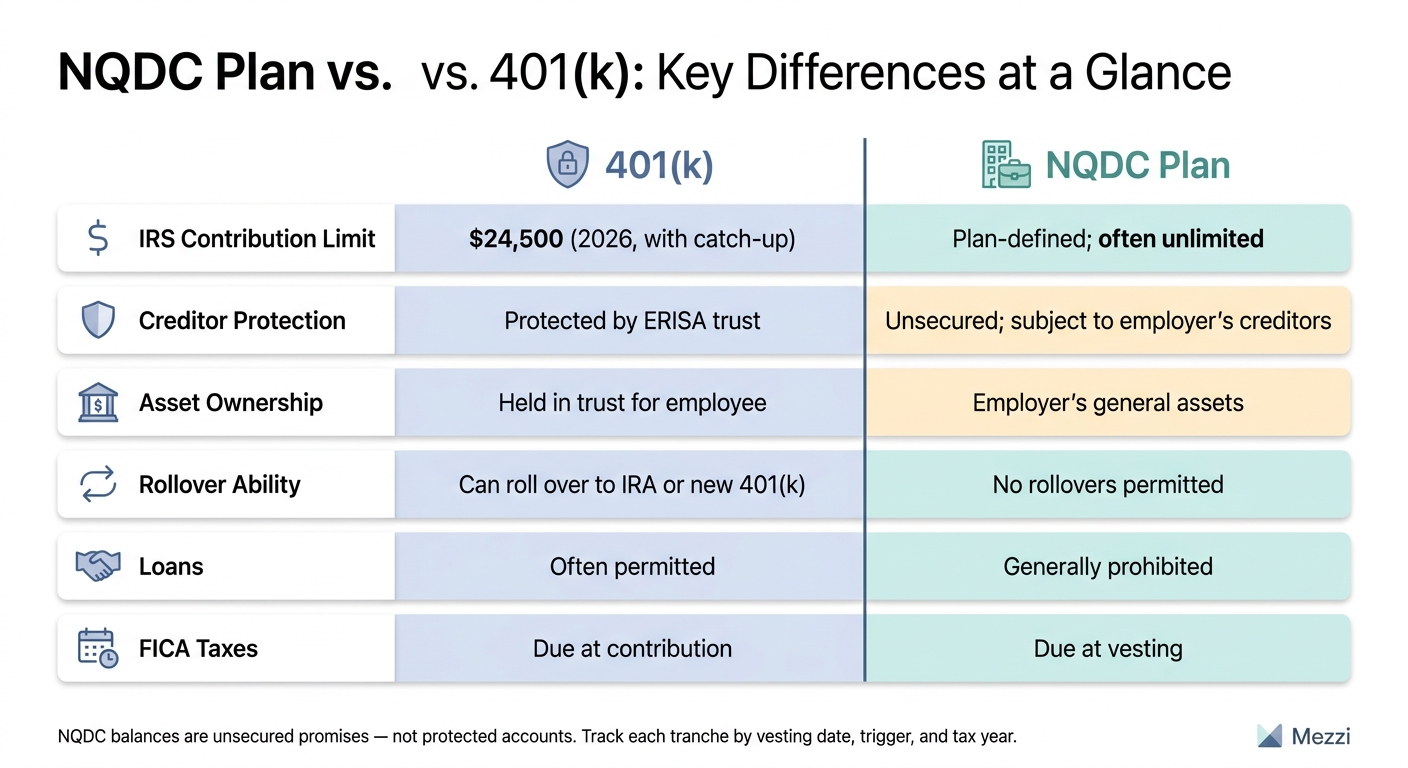

NQDC Plan vs. 401(k): Key Differences at a Glance

Non-Qualified Deferred Compensation (NQDC) - Risks, Rewards & What to Know Before You Elect

1. Know the NQDC rules that drive planning

With the basics out of the way, the next step is to focus on the plan rules that shape taxes and payout timing.

How NQDC differs from a 401(k)

Start here: an NQDC plan is a deferred-pay promise from your employer, not a retirement account. A 401(k) is protected by ERISA, which means assets are held in a trust and may be shielded from company creditors. NQDC assets stay on the employer's balance sheet and may be subject to creditor claims if the company fails.

The main upside may be more deferral flexibility. NQDC plans have no IRS contribution cap, while 401(k) plans do. The trade-off is that distributions are taxed as ordinary income when paid and may not be rolled over into an IRA.

| Feature | 401(k) | NQDC Plan |

|---|---|---|

| IRS Contribution Limit | $24,500 (2026, with catch-up) | Plan-defined; often unlimited |

| Creditor Protection | Protected by ERISA trust | Unsecured; subject to employer's creditors |

| Asset Ownership | Held in trust for employee | Employer's general assets |

| Rollover Ability | Can roll over to IRA or new 401(k) | No rollovers permitted |

| Loans | Often permitted | Generally prohibited |

| FICA Taxes | Due at contribution | Due at vesting |

Once you know what the plan is, it helps to track how each deferral earns, vests, and grows.

Deferrals, vesting, and notional investments

You usually elect salary or bonus deferrals before the tax year starts. For performance-based compensation, elections may sometimes be made up to six months before the end of a 12-month performance period.

Deferred balances may also vest over time. FICA taxes, including Social Security and Medicare, are generally due when the compensation is no longer subject to a substantial risk of forfeiture, rather than when it's paid out.

The balance grows through notional investment elections. You choose benchmarks, such as an S&P 500 index, company stock, or a 401(k)-style fund lineup, and your account is credited with the returns those benchmarks generate, not actual owned securities. In plain English, the account may track market-like results without giving you direct ownership of the underlying holdings. That may make the crediting method a key input in future cash-flow forecasts.

Those rules matter because the election made at deferral time sets the payout path.

Distribution elections and 409A timing limits

Your deferral election sets when and how you get paid. Under Section 409A, you must specify both the trigger for payment and the form of payment, such as a lump sum or installments, when you defer. Common triggers include:

- Separation from service

- A fixed date or year

- Disability

- Death

- An unforeseeable emergency

- A change in control

Later changes are tightly restricted. Any modification must be submitted at least 12 months before the originally scheduled payment date, and the new date must be pushed out by at least five additional years. If 409A is violated through an improper acceleration of payment or a documentation error, that may trigger immediate ordinary income tax on all vested amounts, plus a 20% additional federal tax and interest charge.

If you're a public-company specified employee, a mandatory six-month delay applies to any payout triggered by separation from service. That election then becomes the backbone of your payout forecast.

2. Build a tracking system for future cash flow

Once you know the rules, turn them into a living record for each NQDC tranche.

Collect plan documents and key fields for each tranche

Each year's deferral - often called a tranche - may have its own vesting date, distribution trigger, and payout form. That's why it makes more sense to track NQDC at the tranche level, not just at the plan level.

Pull together these four documents: the plan document or Summary Plan Description (SPD), your enrollment and election forms, your current account statements, and the vesting schedule. Taken together, they show what you deferred, when it vests, and when it may pay out.

For each tranche, record these fields:

| Field | What to Track |

|---|---|

| Plan/Class Year | The year the deferral was made |

| Source of Deferral | Base salary, annual bonus, or performance incentive |

| Deferred Amount | Dollar amount deferred |

| Vesting Date | When the substantial risk of forfeiture lapses |

| Notional Investment Allocation | The benchmark credited to the account |

| Distribution Trigger | The event that starts payout |

| Payout Form | Lump sum or installments |

| First Payout Date | First payment date based on your election |

The vesting date may also determine when FICA is due.

That snapshot becomes the base for your payout calendar.

Create a simple annual payout view

Once you have tranche-level data, roll it into a calendar view. The aim is a single sheet that shows, by year, how much NQDC income may be paid before taxes, whether it may come as a lump sum or installments, and how much of the total balance may still be unvested.

That calendar may support decisions about tax-saving strategies and retirement tax strategies - topics covered in the next section. It may also make it easier to spot whether a distribution starts in the year you retire or the year after, which may affect the tax bracket you land in.

After the calendar is set up, place it next to the rest of your household accounts.

Centralize NQDC with the rest of your household balance sheet in Mezzi

A payout schedule is only part of the picture. Mezzi lets you consolidate NQDC alongside your brokerage accounts, IRA, 401(k), and HSA, so future cash flow and concentration risk may stay visible in one place. That broader view may show whether NQDC adds concentration risk or whether a lump sum may overlap with a Roth conversion. It also helps to capture the election correctly upfront, since changes may be limited.

3. Plan distributions around taxes and high-income years

Map NQDC payouts against your income timeline

That payout calendar gets a lot more useful when you line it up with the other income you may expect in the years ahead: salary, annual bonus, equity vesting, Social Security, Required Minimum Distributions (RMDs), and your target retirement date.

The main issue is simple: which years may absorb NQDC income, and which years may create a tax spike? A year when you're still earning a full salary and RSUs are vesting may be a poor time for a large NQDC lump sum. A year after retirement, when other income may be lower, may be a better fit.

If a distribution starts in the same calendar year you retire, it may stack on top of your final salary and place more income in a higher federal bracket. Delaying the start until the first full calendar year after separation may help avoid that overlap. Public-company specified employees may also face a six-month delay. That timing should be built into the plan so the shift may not land in an unintended tax year.

Once the income timeline is mapped, the next call is how each tranche may pay out.

Compare lump sum vs. installments before the election window closes

Lump sum vs. installments may be the biggest NQDC tax choice. It has to be decided before the election window closes, because later changes are tightly restricted.

A large lump sum may push most of the balance into one high-tax year. Installments may spread that tax liability across several years, but the unpaid balance stays inside the plan and remains subject to employer credit risk until the last payment.

There may also be a state tax angle here. Installments paid over 10 or more years are usually taxed in your state of residence when paid, not where the income was earned. So if you plan to move from California or New York to a no-income-tax state such as Florida or Texas, electing a 10-year installment schedule before you leave may help avoid source-state taxation on those payments.

| Feature | Lump-Sum Distribution | Installment Distributions |

|---|---|---|

| Tax concentration | High; entire balance taxed as ordinary income in one year | Lower; spreads tax liability across multiple years |

| Cash-flow flexibility | High; immediate access to the full balance | Moderate; steady income stream |

| Employer credit exposure | Ends immediately upon payout | Continues until the final payment |

| Tax-deferred growth | Ends upon distribution | Remainder continues to grow tax-deferred |

| Planning simplicity | Simple; one-time event | Requires coordination with RMDs and Social Security |

| State tax treatment | Often taxed by the state where the income was earned | May avoid source-state tax if paid over 10+ years |

Once the payout form is set, the next step is fitting it into retirement income and other bracket-sensitive moves.

Coordinate NQDC with retirement, Roth conversions, and major spending needs

NQDC distributions and Roth conversions may compete for the same tax brackets. Large payouts may reduce room for Roth conversions, while installments that keep annual NQDC income lower may preserve space for conversions at 22% or 24%.

A common sequencing goal is to have NQDC installments end before RMDs begin at age 73. If NQDC income lands on top of RMDs and Social Security in your mid-70s, the combined income may create a tax issue later. Large payouts may also increase Medicare premiums two years later through IRMAA.

NQDC isn't only for retirement. Some people use class-year laddering to assign tranches to specific years, such as college tuition, a second-home purchase, or an early-retirement bridge before Social Security starts. That approach may let cash flow line up with major spending needs without concentrating income in peak-tax years.

Tax timing matters, but it does not remove employer credit risk.

4. Manage employer solvency and concentration risk

After tax timing, the next issue may be simpler and more uncomfortable: does the payout make it to you at all?

Measure how much of your net worth depends on your employer

Many high earners may have a large share of their wealth tied to one company. Your NQDC balance may be only part of that picture. Add unvested RSUs, vested company stock in a brokerage account or 401(k), any SERP value, plus your salary and bonus, and the total may add up fast.

A simple way to look at it is to list each employer-linked source as a share of total net worth:

| Source of Employer Exposure | Description | Example % of Net Worth |

|---|---|---|

| NQDC Balance | Unsecured deferred compensation | 15% |

| Unvested Equity | RSUs, PSUs, and stock options | 20% |

| Vested Company Stock | Shares held in brokerage or 401(k) | 10% |

| SERP Value | Present value of supplemental pension | 5% |

| Total Employer-Linked Assets | Sum of all above | 50% |

Many planners use a target range of 10% to 15% of net worth for total employer exposure. The example above shows how that number may climb to 50% without much effort. That’s why NQDC may need its own line in the math, not a footnote.

NQDC is unsecured, so employer distress may delay payment or eliminate it. A rabbi trust does not protect against bankruptcy.

Once you know your total exposure, the next step may be to focus on the parts you still have room to change.

Adjust what you can control in other accounts

You generally may not reduce your NQDC balance after deferrals are made, since 409A rules lock in the structure. But you may still reduce overlap elsewhere.

If your NQDC notional investments include company stock, moving those balances to diversified options may reduce exposure to the firm’s equity performance, even though that does not remove the underlying credit risk.

Then look beyond the plan. If your 401(k) and taxable brokerage account also hold employer stock, or lean hard into the same sector, your concentration may build on itself. Trimming that overlap in accounts you control may be one of the more direct levers available. In a taxable account, direct indexing may be one way to underweight your employer’s sector.

A common rule of thumb is to keep total NQDC balances at no more than one to two years of pay. If exposure already looks high, some people use shorter in-service payout elections to reduce future concentration.

Use Mezzi's X-Ray and monitoring to keep risk visible

Once you have that full picture, it may help to keep employer stock and deferred compensation in one place instead of scattered across accounts.

Use Mezzi's X-Ray to surface employer stock and other concentrated holdings across connected accounts. Mezzi gives you a read-only view of your household accounts, which may make it easier to keep the risk visible, decide what to change, and track the impact over time.

Conclusion: make NQDC part of your wealth plan

Once you know the rules, timing, and exposure, NQDC may stop feeling like a vague perk and may start to look more like a planning input. It may be most useful when it's tracked like future income: by tranche, by tax year, and by employer risk.

The value may not come from the benefit alone. It may come from treating each tranche as a dated cash-flow decision. That means tracking each tranche, mapping payout years, and measuring employer exposure as a single number against your net worth.

Mezzi lets you centralize NQDC alongside your 401(k), IRA, taxable brokerage, and cash accounts in one read-only household view, so the payout schedule and concentration risk may stay visible in one place. That may turn a hidden benefit into part of your cash-flow plan.

NQDC may work best when you see it next to the rest of your balance sheet.

FAQs

How risky is an NQDC plan if my employer struggles?

An NQDC plan may carry meaningful risk if your employer runs into trouble, because it’s an unsecured promise to pay. That’s the key difference from a 401(k): the assets stay part of the company’s general assets, not a protected trust.

If the company goes bankrupt, you may become a general unsecured creditor and may recover only a fraction of your balance. Even a rabbi trust may not shield those assets from creditors during insolvency.

Should I choose a lump sum or installments?

It may depend on your tax planning, cash needs, and employer credit risk.

A lump sum gives you immediate control, but it may also create a large one-time tax bill. Installments may keep annual income lower and may extend tax-deferred growth.

That said, installments may also keep you exposed to your employer for longer, since NQDC assets are unsecured obligations. Some people look at their total employer exposure, cash flow needs, and other income when weighing the tradeoff.

Under Section 409A, changing your election is strictly limited.

What should I track for each NQDC deferral year?

Track each deferral year on its own. For every year, record:

- election deadline

- distribution trigger

- payout method

- employer solvency risk

- possible stacking with other income

- expected state of residency at payout

Keep all of it in one dashboard or spreadsheet. Section 409A changes may be hard to make and may trigger penalties or tax spikes, so accurate tracking from the start may matter.

Disclosures:

- This content is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

- Past performance is not indicative of future results. No guarantee of future performance or outcomes is implied.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.