Need cash but don’t want to sell investments? A pledged asset line may be one option - but the tradeoff may be sharp.

If I borrow against a taxable portfolio, I may keep my holdings invested and may avoid selling stock for a $250,000 down payment, tax bill, or short bridge need. But that loan may come with variable rates, maintenance calls, and forced sales if the market moves against the account.

Here’s the short version:

- A pledged asset line (PAL), also called an SBLOC, may let me borrow against a taxable brokerage account

- IRAs and 401(k)s usually do not qualify

- Minimum asset levels may start near $100,000 and may run much higher by firm

- Credit limits may depend on the mix of holdings, with Treasuries and bond funds often getting higher advance rates than single stocks

- PAL money may be used for things like real estate, taxes, or business cash needs

- PAL money may not be used to buy securities or pay margin debt

- Rates are often variable and may be tied to SOFR plus a spread

- A market drop may trigger a maintenance call, and the lender may sell holdings

So when might a PAL make sense?

Usually, it may fit best when three things are true:

- I have a large taxable portfolio

- I need cash for a short-term use

- I have a clear way to repay the balance

When those pieces are missing, selling investments, using a HELOC, or even taking no loan at all may be the cleaner path.

How to Access Liquidity Without Selling Investments | Pledged Asset Lines

Quick comparison

| Option | What it may suit | Main tradeoff | Time to funds |

|---|---|---|---|

| PAL / SBLOC | Down payment, taxes, bridge cash | Call risk tied to market moves | 3–7 days |

| Selling investments | Simple cash need | Taxes and lost market exposure | Same day to few days |

| Margin loan | Buying securities | Call risk and use limits | Same day |

| HELOC | Home-related borrowing | Home secures the debt | 30–60 days |

| Personal loan | Borrowing without assets pledged | Higher rates, lower limits | Days to weeks |

A simple way I’d frame it: a PAL may work when I want liquidity without selling, but only if the portfolio may hold up under stress and repayment may be clear.

What a pledged asset line is and who it is for

A pledged asset line (PAL), also called a securities-based line of credit (SBLOC), is a revolving line of credit backed by assets in a taxable brokerage account. Your investments stay in the market, and you may draw cash when needed.

Retirement accounts don't qualify. Pledging an IRA may count as a taxable distribution and may trigger penalties. Using a 401(k) as collateral may disqualify the plan. For that reason, PALs are generally limited to taxable brokerage accounts.

Minimum portfolio requirements often start around $100,000 at firms like Charles Schwab and Wells Fargo, move up to $500,000 at JPMorgan, and may reach $1,000,000+ at Goldman Sachs. In practice, PALs may fit investors with large taxable portfolios who need short-term liquidity and already have a clear way to pay the balance back, such as a bonus or an asset sale. They may be a poor fit when the cash need has no clear end point or when repayment may be uncertain. That gap is a big reason PALs look very different from margin, home equity, and unsecured borrowing.

How a pledged asset line differs from margin, HELOCs, and personal loans

The biggest difference is use of proceeds. Margin loans are used to buy securities. PALs are not. PAL funds can't be used to buy securities or to repay margin debt.

Compared with a HELOC, a PAL may be faster to set up and may come with a lower rate, but the tradeoff may be more call risk if the portfolio drops. Rates are variable and are generally tied to 30-day SOFR plus a spread. PAL rates generally range from 5.80% to 7.95%, while HELOCs are closer to 8.50% to 10.50%.

Which accounts and assets typically qualify

Eligible accounts are often:

- Individual taxable brokerage accounts

- Joint taxable brokerage accounts

- Revocable trust taxable brokerage accounts

Borrowing value usually depends on what you hold. U.S. Treasuries and investment-grade bonds often support the highest values. Large-cap ETFs, mid-cap or sector funds, and international or small-cap stocks usually support less. Penny stocks, options, restricted stock, unvested RSUs, lockup shares, and private equity stakes often count for little or not at all.

If a portfolio is concentrated in a single stock, the credit limit may be lower, and the odds of a maintenance call may be higher.

How those borrowing values turn into a credit limit is the next step.

How pledged asset lines work in practice

Collateral, loan-to-value, and credit limits

Once a lender identifies eligible accounts, it turns the portfolio into a borrowing limit. The key point: the line is sized from the assets in the account, not only from income. Each asset class gets an advance rate, which is the share of that asset's value that may count toward the credit line. Representative rates by asset class are below.

| Asset Class | Typical Advance Rate |

|---|---|

| U.S. Treasury ETFs and Notes | 85% – 95% |

| Investment-Grade Municipal/Corp Bonds | 75% – 85% |

| Diversified Equity ETFs (e.g., VTI, VOO) | 65% – 75% |

| Large-Cap Individual Stocks | 50% – 70% |

| Mid-Cap / Small-Cap Stocks | 30% – 50% |

| Concentrated Positions (>25% of account) | 25% – 50% |

| Restricted or Unvested Shares (RSUs) | 0% |

Your total credit limit comes from the weighted average advance rate across the full account. In plain English, a mix of many holdings may support a higher line than a portfolio built around one stock.

Two limits matter after the line opens:

- Your first draw may not exceed the account's weighted average advance rate.

- Maintenance thresholds often fall in the 70% to 85% range of the borrowing limit; if the account drops below that range, the lender may issue a call.

If markets fall fast, that may lead to a call and, in some cases, forced sales.

Once that limit is in place, the next piece is the day-to-day side of the line: how money comes out, how it gets paid back, and what rules stay attached to it.

Drawing funds, repayment, interest rates, and use-of-funds rules

A PAL works much like a revolving credit line. You may draw only what you need, through a wire, check, or transfer to a linked account, then repay and draw again without filing a new application each time. Interest accrues only on the amount actually borrowed, not the full limit, and lenders usually bill it monthly. Repayment is often interest-only, with no set principal schedule.

Rates are variable and are usually quoted as a spread over 1-month SOFR. Bigger balances often come with smaller spreads. Some agreements have a 3- to 5-year term with a balloon payment at the end, while others may renew on their own.

There is one firm rule across lenders: PAL proceeds cannot be used to purchase, trade, or carry marketable securities, under Federal Reserve Regulation U. Uses such as real estate, taxes, business expenses, and general liquidity needs are usually allowed. The lender also usually keeps the right to demand repayment at any time.

Tax treatment

Borrowing itself is not taxable because no sale takes place. The tax treatment of the interest depends on how the borrowed funds are used. Proceeds used for investment purposes may qualify for the investment interest expense deduction, while proceeds used for personal expenses generally may not. The IRS requires interest tracing, so some borrowers keep PAL proceeds in a separate account instead of mixing them with personal cash. That may make the tracing process cleaner and lines up with the use-of-proceeds rule already attached to the line.

Those mechanics tend to matter most when the cash need may be short-term; the next section looks at when a PAL may fit, and when it may not.

Best use cases, key risks, and when a pledged asset line is the wrong fit

Common situations where investors use a pledged asset line

Once you understand how a PAL works, the next step is figuring out when the leverage may be worth the risk.

A PAL may fit best for short-term cash needs with a clear payoff date. Real estate is one of the most common examples. A buyer may use a PAL to fund an all-cash offer or a down payment in days, not weeks, without selling appreciated positions or changing the portfolio’s allocation. In a competitive housing market, that speed may matter.

Tax season is another common use case. Investors facing a large bill from a business sale, stock vesting, or a Roth conversion may borrow against a portfolio to pay the IRS without selling appreciated positions and triggering added capital gains taxes.

Some business owners also use PALs for short-term working capital, though that approach may involve pledging personal assets.

A PAL may also offer temporary liquidity during a market downturn. If a known expense is coming up, the line may cover that need while the portfolio has more time to recover instead of being sold at a lower price.

The biggest risks: maintenance calls, rising rates, and forced sales

The upside only holds if the portfolio may absorb a drop without forcing a sale.

The main risk is simple: if the pledged portfolio falls far enough, the lender may issue a call for more collateral or repayment. Lenders are not required to give advance warning before selling holdings to meet that call, and they may decide which positions to liquidate.

Sharp selloffs may trigger maintenance calls fast, as March 2020 showed.

PALs are also floating-rate loans. Since the rate resets over time, interest costs may climb during a rate-hiking cycle. There’s renewal risk too. Most agreements run 3 to 5 years, and a lender may decline to renew or may change the spread at maturity.

When a pledged asset line is usually the wrong tool

This is where PALs tend to break down: when repayment is unclear or the collateral may be too concentrated.

A PAL is usually a poor fit for recurring living expenses. Using a revolving line for regular costs without a repayment plan may turn a short-term tool into long-term debt. And because the rate floats, that setup may get harder over time.

Borrowing against a concentrated position may also be risky. If one stock makes up more than 25% of the account, a single-name drop may trigger a call even if the rest of the market stays steady.

| Situation | Best Fit | Why |

|---|---|---|

| Real estate down payment or bridge | Strong | Fast funding and a clear repayment path |

| Covering a large tax bill | Strong | May avoid selling appreciated investments |

| Business working capital, short-term | Moderate | May cost less than some other options, but requires pledging personal assets |

| Ongoing personal expenses | Poor | No clear repayment source |

| Speculative ventures | Poor | Repayment may depend on uncertain future success |

| Concentrated or volatile holdings | Poor | A single-name drop may trigger a call |

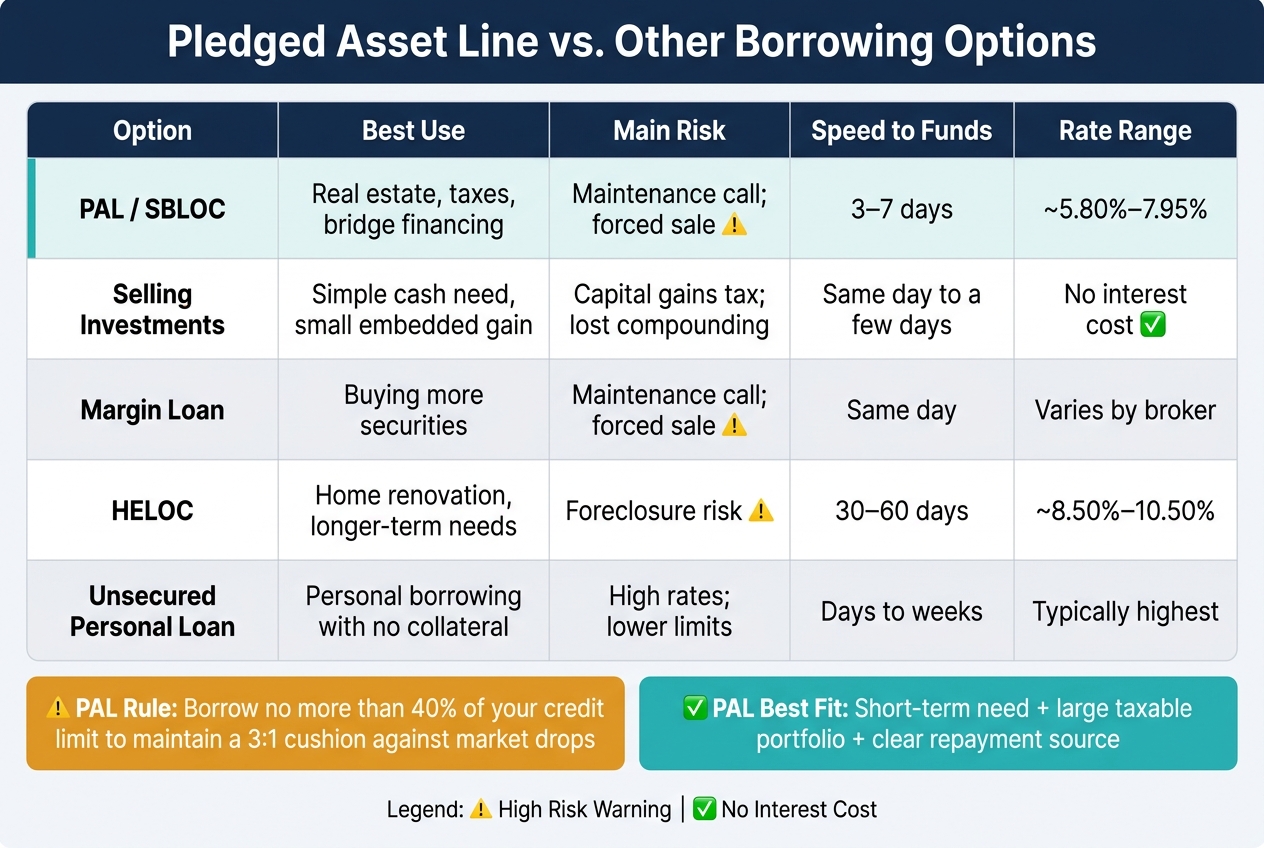

One practical guardrail some investors use: borrow no more than 40% of your limit. That keeps at least a 3:1 cushion between total credit capacity and the amount drawn. If that cushion may not hold, the PAL may be too large.

Pledged asset lines vs. selling investments and other borrowing options

Pledged Asset Line vs. Other Borrowing Options: A Side-by-Side Comparison

Pledged asset line vs. selling investments

Once you understand how a PAL works, the next step is simpler: does borrowing make more sense than selling?

Selling may be the easiest way to get cash. There’s no interest, no maintenance call risk, and no lender in the middle. But a sale may trigger capital gains right away, and it stops future compounding on the shares you sold. Borrowing may let you keep those investments in place and defer taxes, which for some people may outweigh the interest cost when the embedded gain is large.

A simple rule of thumb may look like this: borrow when the gain is large and repayment is clear; sell when the gain is small or you already want out of the position.

Pledged asset line vs. margin, HELOCs, and unsecured borrowing

One practical way to sort this out is to compare a PAL with the three options people look at most often.

| Option | Best Use | Main Risk | Speed to Funds |

|---|---|---|---|

| PAL | Real estate, taxes, bridge financing | Maintenance call; forced sale | 3–7 days |

| Margin Loan | Buying more securities | Maintenance call; forced sale | Same day |

| HELOC | Home renovation, longer-term needs | Foreclosure risk | 30–60 days |

| Unsecured Loan | Personal borrowing with no collateral | High rates; lower limits | Days to weeks |

Margin loans are set up for buying securities and are capped by brokerage rules. PALs are non-purpose loans, and they may come with higher advance rates and more flexible uses.

HELOCs don’t come with maintenance-call risk, but funding may take longer.

Unsecured personal loans don’t require collateral, though rates may run much higher and credit limits may be lower.

A short checklist for deciding if a PAL fits your situation

Before borrowing, it may help to pressure-test the idea with four questions:

- Do your assets qualify without creating account or tax issues? Only fully paid securities in taxable accounts typically qualify. IRAs and 401(k)s are generally off the table.

- Is this a short-term need? A PAL may work best when there’s a defined repayment event, like a home sale, a bonus, or a business distribution. Open-ended borrowing on a floating-rate line may increase both cost and repayment risk.

- Do you have a clear repayment source? If the answer is “I’ll figure it out,” the PAL may be the wrong tool.

- Can your portfolio handle a sharp drop without a call? If a sharp market drop may trigger a maintenance call at your current draw amount, your utilization may be too high.

Mezzi may help you see portfolio concentration and borrowing capacity before you decide.

FAQs

How much can I safely borrow?

Your lender may set borrowing capacity by applying advance rates to eligible holdings, often based on factors like liquidity and volatility. In many cases, limits may range from 50% to 95% of portfolio value.

A more conservative approach may make sense for some borrowers: borrowing well below the maximum may leave more room for market swings and may reduce the risk of a margin call, which may force the sale of securities.

What happens if my portfolio drops fast?

If your portfolio drops fast, the value of your collateral may fall too. That may push your loan-to-value ratio above the lender’s maintenance threshold and trigger a maintenance call.

If that happens, you may need to add cash, pledge more eligible securities, or pay down the loan on short notice. If you can’t, the lender may sell your securities without notice. That sale may happen at low prices and may also create unintended capital gains taxes.

Is a PAL better than selling investments?

Not necessarily. A pledged asset line is a different tool, not flat-out better than selling.

Selling is usually the cleanest way to raise cash. It removes market and collateral risk in one move. But it may trigger capital gains, and it may change your allocation.

A PAL may make more sense in some cases when someone wants short-term liquidity without selling. That said, it adds debt, interest costs, and the risk of forced liquidation if the market falls.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.