Here’s the short answer: a qualified purchaser may face a much higher bar than an accredited investor. In many cases, accredited investor status is based on income or net worth, while qualified purchaser status is based on at least $5,000,000 in qualifying investments. That split may affect which private funds you may enter, including 3(c)(1) and 3(c)(7) funds.

If I wanted the fast version, I’d boil it down like this:

- Accredited investor may mean:

- $1,000,000+ net worth, excluding a primary home, or

- $200,000+ annual income, or $300,000+ with a spouse or spousal equivalent

- Qualified purchaser may mean:

- $5,000,000+ in qualifying investments for an individual or couple

- A person may qualify as accredited but still not qualify as a qualified purchaser

- The label may affect access to:

- Reg D private offerings

- 3(c)(1) funds with a 100-investor cap

- 3(c)(7) funds with up to 2,000 investors

A simple way to think about it: accredited investor looks at income or net worth; qualified purchaser looks at invested assets only. Your primary home generally does not count in either case.

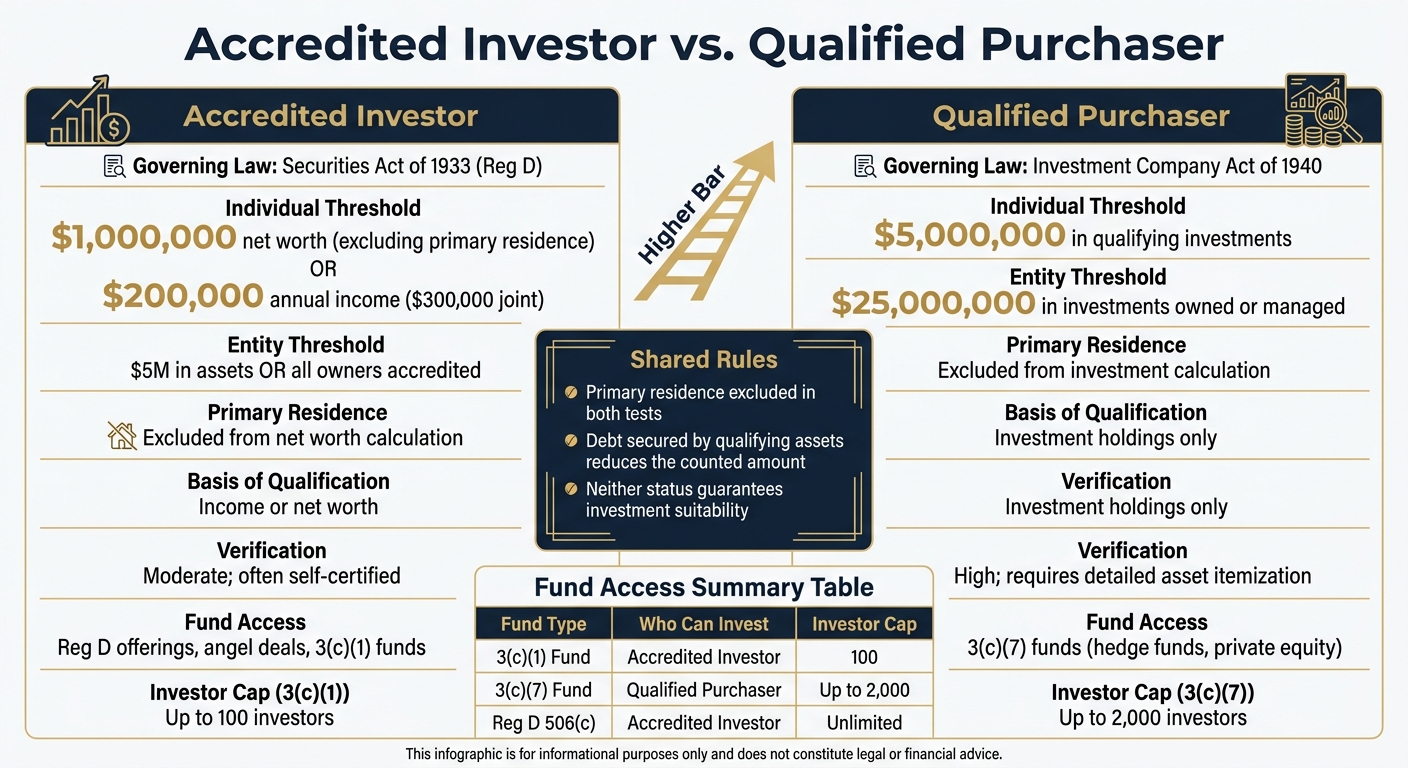

Accredited Investor vs Qualified Purchaser: Key Differences at a Glance

AdBits | Qualified Purchaser vs. Accredited Investor | What You NEED to Know

Quick Comparison

| Criteria | Accredited Investor | Qualified Purchaser |

|---|---|---|

| Main test | Income or net worth | Investment holdings |

| Individual threshold | $1,000,000 net worth or $200,000 income ($300,000 joint) | $5,000,000 in qualifying investments |

| Primary residence | Excluded | Excluded |

| Common fund access | Reg D, angel deals, 3(c)(1) funds | 3(c)(7) funds |

| Investor cap often linked to fund type | 100 for many 3(c)(1) funds | Up to 2,000 for many 3(c)(7) funds |

| Verification | Often lighter | Often more detailed |

So if I were skimming this topic, I’d focus on one question first: am I being tested on what I earn and own, or on how much I already have invested? That may tell me which bucket I may fit into.

Accredited investor: who qualifies and what it opens up

Accredited investor status may be the first private-market checkpoint. Many issuers look for it before they offer private deals. Here’s who may qualify.

Income, net worth, and entity eligibility

An individual may qualify through income above $200,000 per year, or $300,000 with a spouse or spousal equivalent, in each of the prior two years, with a reasonable expectation of the same this year.

The net worth path uses a different test. A person may qualify with net worth above $1,000,000, alone or with a spouse or spousal equivalent, while excluding the value of a primary residence.

Some license holders may also qualify. That includes people with a Series 7, Series 65, or Series 82 license in good standing.

Certain entities may qualify too. For example, some trusts, LLCs, and partnerships with more than $5,000,000 in assets may meet the standard if they were not formed just to buy the offered securities.

What accredited investor status typically gives you access to

Accredited status may open the door to private placements, angel deals, real estate syndications, and 3(c)(1) funds.

That said, this label points to financial capacity, not suitability. In plain English, meeting the threshold does not automatically mean a deal fits a person's goals, time horizon, or risk level.

It also may leave many larger private funds out of reach. Some private funds stop at the accredited investor line. Others use the stricter qualified purchaser standard instead.

Qualified purchaser: a higher bar with bigger implications

Qualified purchaser status sits on a stricter track under the Investment Company Act of 1940. It’s separate from accredited investor status.

The $5,000,000 investment threshold and other common paths

For an individual or a married couple, the main test is owning at least $5,000,000 in investments. That word matters: investments, not net worth.

Assets that generally count include stocks, bonds, fund interests, investment real estate, commodities held for investment, and cash. Some things usually do not count:

- Your primary residence

- Personal property

- Assets used directly in the active operation of a business

If debt is secured by those assets, that debt reduces the amount that counts toward the $5,000,000 threshold.

For most entities, the bar is higher: $25,000,000 in investments owned or managed.

Why qualified purchaser status matters for 3(c)(7) funds

This higher threshold matters because many private funds use it as the gatekeeper. QP status is the main requirement for investing in funds that rely on the Section 3(c)(7) exemption.

That group includes many large hedge funds and private equity funds that use this structure to take in more investors while staying exempt from SEC registration. Since every investor in a 3(c)(7) fund must be a qualified purchaser, these funds may accept up to 2,000 investors. That’s far above the 100-investor cap tied to 3(c)(1) funds.

The trade-offs may be meaningful. These offerings often involve more leverage, longer lockup periods, higher minimum commitments, and much less liquidity than many accredited investors may see elsewhere. And because 3(c)(7) funds are exempt from standard SEC registration, reporting may be less standardized. In practice, that may leave more of the due diligence work with the investor.

How Mezzi helps high-net-worth investors evaluate these funds

Before locking up capital for years, some investors review their current exposure first. Mezzi's X-Ray and overlap analysis show total exposure across ETFs, mutual funds, and stocks. That may make it easier to check for concentration before adding a private fund.

Mezzi also offers 24/7 monitoring with insights on concentration and asset allocation. That may be useful when part of a portfolio is tied up in a fund for a long period.

Qualified purchaser vs accredited investor: side-by-side comparison

These two labels come from different laws, look at different yardsticks, and may open the door to different types of investments. For individuals, qualified purchaser is a much tougher standard than accredited investor.

Thresholds, legal standards, and who fits each label

A simple example shows the gap. A physician earning $400,000 a year with a $2,000,000 net worth - with $1,200,000 of that tied up in home equity - may qualify as an accredited investor. But that same person may still fall short of the qualified purchaser test because their qualifying investments are well under $5,000,000.

Here’s the shortest practical comparison.

| Feature | Accredited Investor | Qualified Purchaser |

|---|---|---|

| Governing Law | Securities Act of 1933 (Reg D) | Investment Company Act of 1940 |

| Individual Threshold | $1M net worth or $200K income ($300K joint) | $5M in qualifying investments |

| Entity Threshold | $5M in assets OR all owners accredited | $25M in investments |

| Primary Residence | Excluded from net worth | Excluded from investments |

| Basis of Qualification | Income or net worth | Investment holdings only |

| Verification burden | Moderate; often self-certified | High; requires detailed asset breakdown |

The core difference is pretty simple:

- Accredited investor status looks at income or net worth

- Qualified purchaser status looks at investment holdings only

- Your primary residence does not count in either test

Fund access and due diligence expectations

The next split is about access. Each status may allow entry into different types of funds, and the diligence process may get more detailed as you move up the ladder. Accredited investors may access Reg D offerings, angel deals, and 3(c)(1) funds, which are capped at 100 investors. Qualified purchasers may access 3(c)(7) funds, which may accept up to 2,000 investors and often include hedge funds and private equity vehicles.

| Fund Type | Who Can Invest | Investor Cap |

|---|---|---|

| 3(c)(1) Fund | Accredited Investor | 100 |

| 3(c)(7) Fund | Qualified Purchaser | Up to 2,000 |

| Reg D 506(c) | Accredited Investor | Unlimited |

Verification also tends to get more detailed at the QP level. Accredited investor status is often self-certified. Qualified purchaser verification usually requires a full itemization of qualifying investments, along with any related debt that may need to be subtracted.

How to determine your status and what to do next

Once you know the difference, this checklist may help you confirm your status before committing capital.

A practical checklist before committing capital

Work through these steps before signing any subscription documents.

- Confirm your likely status. Calculate net worth for accredited investor status without including your primary residence. Then total only qualifying investments for the $5,000,000 qualified purchaser test.

- Review the fund's structure. Check whether the offering may be open to accredited investors or limited to qualified purchasers. This may be stated in the fund's subscription documents and private placement memorandum.

- After confirming status, check whether the fund fits your liquidity needs. Make sure you may handle the lockup period without disrupting your financial plan. Also consider whether the commitment may leave you more exposed to one asset class or manager.

- Evaluate tax consequences. Many private fund interests issue K-1s, which may make tax filing more complex. Review the expected tax treatment before you commit.

- Verify status with a professional. Rule 506(b) often allows self-certification. Rule 506(c) usually requires third-party verification from a CPA, attorney, or adviser.

A consolidated holdings view may make verification faster. Mezzi may help by consolidating your accounts in read-only mode, which may give your CPA or attorney a cleaner view of holdings and net worth for verification.

FAQs

Can I be accredited but not a qualified purchaser?

Yes. Accredited investor and qualified purchaser are two separate legal standards. Meeting one does not automatically mean you meet the other.

Accredited investor status is based on income or net worth under the Securities Act of 1933.

Qualified purchaser status follows a different set of rules under the Investment Company Act of 1940 and typically requires at least $5 million in owned investments.

What counts as qualifying investments for QP status?

For QP status, qualifying investments generally means at least $5 million in investable holdings for individuals, not total net worth.

That amount may include securities, investment real estate, cash and cash equivalents, commodity interests, certain financial contracts, and interests in other qualified-purchaser funds.

It generally does not include your primary residence, personal property, or assets used directly in an active business. Related liabilities may reduce the amount that counts.

How do I verify whether I qualify before investing?

The investment issuer is generally the party that checks whether you meet the required standards before you invest.

How that check happens may depend on the offering. In some cases, it may involve self-certification. In others, you may need to provide documents to the issuer, a lawyer, or an accountant.

Common documents may include:

- Tax returns or W-2s to show income

- Bank or brokerage statements to show net worth or investment thresholds

- Proof of Series 7, 65, or 82 licenses

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.