For many people, selling RSUs at vest may be the cleanest default. The main reason: the full value at vest may already be taxed as ordinary income, so waiting to sell may not reduce that tax bill. After that, the choice may be less about taxes and more about stock risk, cash needs, and how much of your money may already be tied to your employer.

Here’s the short version:

- Vesting may trigger wage income based on the stock price on the vest date.

- Selling right away may mean little to no capital gain or loss.

- Holding for more than 1 year after vest may make later gains eligible for long-term capital gains rates, such as 0%, 15%, or 20% for some taxpayers.

- But holding may also leave you with more single-stock exposure tied to the same company that may already pay your salary and future equity.

- A common check: if you received the same after-tax amount in cash today, would you use it to buy your company’s stock?

- Federal RSU withholding may be only 22% on supplemental wages up to $1 million, which may leave a tax gap for higher earners.

- Broker forms may sometimes show $0 cost basis, so some taxpayers review basis reporting to avoid paying tax twice on the same income.

RSUs: Hold or Sell? The Right Strategy

Quick Comparison

| Choice | Tax at Vest | Later Tax Treatment | Stock Risk | Cash Access | Best Use Case |

|---|---|---|---|---|---|

| Sell all at vest | May already be owed as ordinary income | Usually little capital gain/loss at sale | Lower | Higher | People who may want to cut employer-stock exposure or cover taxes |

| Sell part | May already be owed as ordinary income | Tax applies only to shares kept after vest | Medium | Medium | People using a set cap for employer stock |

| Hold all | May already be owed as ordinary income | Later gains may be short-term or long-term depending on timing | Higher | Lower | People with low exposure and strong conviction |

If I boil the article down to one idea, it’s this: RSU decisions after vest may be a portfolio choice first and a tax-timing choice second.

How RSUs are taxed at vest and when you sell

When RSUs vest, the IRS generally treats the shares' fair market value as wage income even if you don't sell a single share. That means the tax bill may start at vest, not at sale.

The practical sticking points are pretty simple: withholding, cost basis, and when capital gains begin.

Ordinary income at vest and withholding shortfalls

At vest, employers often withhold federal tax on supplemental wages at 22% for amounts up to $1 million. For higher earners, that rate may be too low. So the amount withheld may not match the amount later owed.

Take one example: a $180,000 vest on top of a $220,000 salary may leave a large federal withholding gap. In cases like that, some people increase W-4 withholding from their regular paycheck or make quarterly estimated payments to lower the odds of an underpayment surprise.

And that's only part of the issue. Broker tax forms may add another wrinkle.

Brokers sometimes report $0 basis on Form 1099-B for RSU sales. If that happens, the sale may look more taxable than it may be. Many taxpayers adjust basis to the vest-date FMV on Form 8949 so the same income isn't taxed twice.

Capital gains start after vest, not at grant

Your cost basis is generally the fair market value on the vest date. Any gain or loss usually starts from that point forward. The grant date does not factor into this part of the tax math.

If you hold the shares and sell within one year after vesting, any gain may be treated as short-term capital gain, which is taxed at ordinary income rates. If you hold for more than one year after vesting, any added appreciation may qualify for long-term capital gains rates of 0%, 15%, or 20%. High earners may also owe the 3.8% Net Investment Income Tax.

One key point here: holding after vest may change the tax treatment of later price movement, but it does not change the fact that the vest itself was already taxed as income.

Tax treatment at each stage

Here's the tax treatment at each stage in one view.

| Event | Tax Character | Rate Type | Holding Period |

|---|---|---|---|

| Vesting | Ordinary income plus payroll taxes | Ordinary + FICA | N/A |

| Sale at vest | Capital Gain/Loss | Usually near zero | 0 days |

| Sale within 1 year | Capital Gain/Loss | Short-term (ordinary rates) | 1 day to 1 year |

| Sale after 1 year | Capital Gain/Loss | Long-term (0/15/20%) | More than 1 year |

Once the tax side makes sense, the next issue may be simpler in theory and harder in practice: whether holding the stock still fits your risk level and cash needs.

The real decision factors: concentration risk, cash needs, and conviction

Once you understand the tax mechanics, the harder question becomes: should you actually hold the stock? For most people, that choice may depend less on tax moves and more on how much of their financial life may already be tied to their employer.

How much employer stock is too much

Your salary, bonus, health insurance, career growth, and unvested equity may already be linked to one company. Add vested RSUs on top, and you may take on two-way risk: if the company hits a rough patch, your paycheck and your portfolio may drop at the same time.

Many financial planners suggest keeping a single-stock position below 10% to 15% of your overall investable portfolio. A common way to measure that is against liquid net worth: brokerage accounts, retirement accounts, and cash, not your home. Above 20%, the position may be viewed as an undiversified bet that calls for a deliberate, justified exception.

Here’s a simple gut-check: if your employer handed you the same dollar amount as a cash bonus today, would you use that cash to buy company stock? If the answer is no, then holding the shares by default may amount to doing exactly that - just passively. Holding vested RSUs is the same as buying company stock with your after-tax proceeds.

Hidden exposure may also come from ESPP shares, unvested grants, and employer stock inside 401(k) funds. So your actual concentration may be higher than it first appears.

If your exposure may already be above your cap, selling at vest may become the default.

When immediate liquidity matters more than future upside

Even if concentration may be within range, cash needs may still make selling the better move.

If withholding falls short, selling at vest may cover the tax gap without a scramble later. Beyond taxes, near-term cash needs - a home down payment, paying off high-interest debt, or building a six-month emergency fund - may also justify cutting exposure fast. Future upside may be uncertain; a near-term goal may be more concrete.

"The decision to hold concentrated employer stock should be deliberate, not the result of inaction." - Progress Wealth Management

Using Mezzi to see your total exposure across accounts

Your cap only works if you can see every source of employer stock in one place. Mezzi is designed to show your employer-stock exposure across brokerage, retirement, ESPP, and unvested holdings, so you may compare the total against your concentration cap with a clearer view.

3 main strategies compared: sell now, sell part, or hold

Once you know your concentration level and cash needs, the decision may come down to three paths. Each one involves a different tradeoff between simplicity, upside, and concentration risk. The table below shows how each approach may affect risk, liquidity, and tax complexity.

Immediate sale at vest

Selling at vest turns the grant into cash right away and avoids future price risk. You may also have liquidity for any withholding gap and a simpler tax picture. In this setup, holding may be viewed as an active choice, not a default.

This path may fit best if your employer stock already makes up a meaningful share of your net worth, or if you have near-term financial goals that may benefit from more liquidity.

Partial sale with a rules-based cap on employer stock

A middle path is to sell only enough shares to keep your total employer-stock exposure below your preset cap. You hold the rest, which may leave room for some upside if the stock performs well.

Sell enough shares to keep total employer-stock exposure below your preset cap.

Comparison table: immediate sale vs. partial sale vs. holding

| Strategy | Concentration Risk | Liquidity | Tax Complexity | Upside Potential | Best Fit |

|---|---|---|---|---|---|

| Immediate Sale | Lowest | Highest | Simple | Market-based | Most employees; those needing cash or already overexposed |

| Partial Sale (Rules-based) | Moderate | Moderate | Moderate | Partial | Those with moderate conviction who want to manage risk without going all-in |

| Hold | Highest | Lowest | High | Highest | Those with low existing exposure and high conviction |

You may use this as the basis for a repeatable RSU rule at every vest.

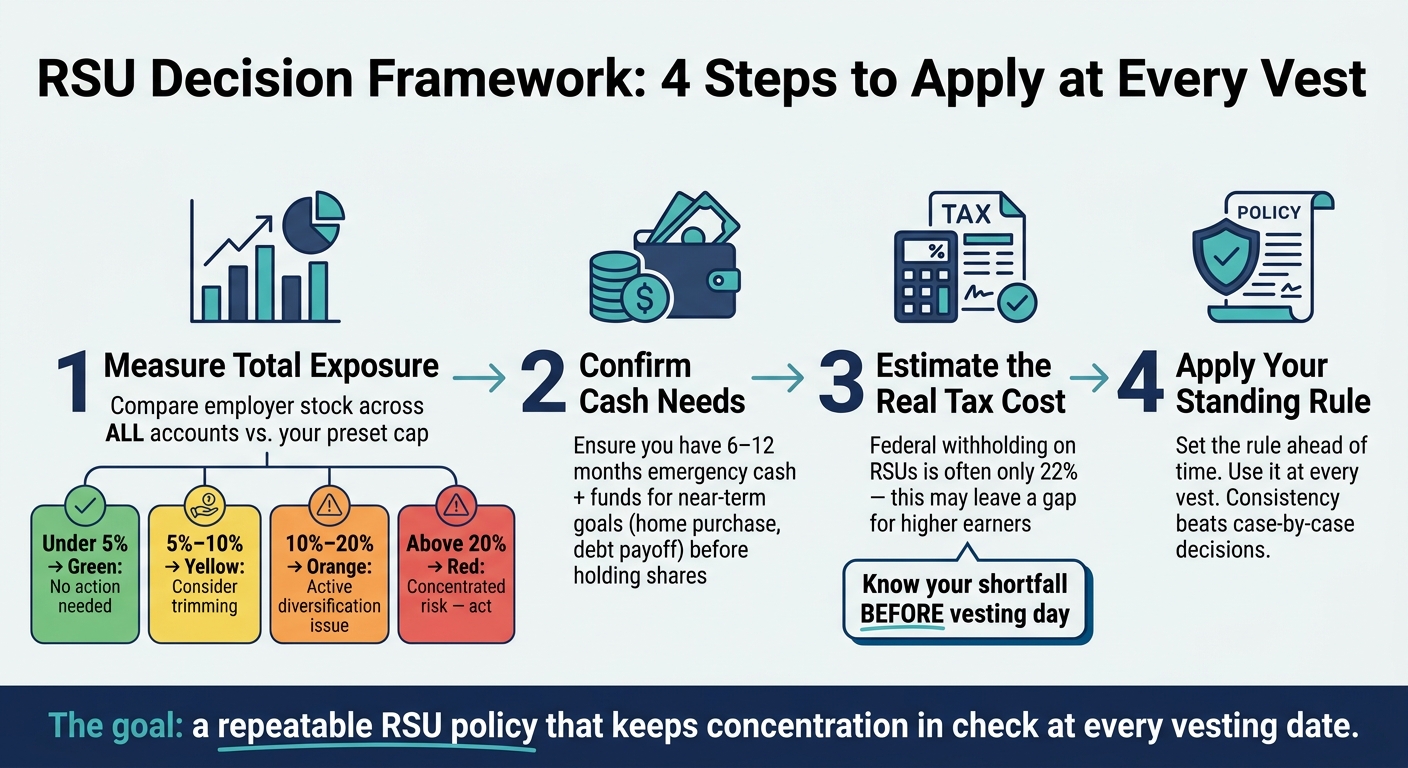

A repeatable framework for every future vesting date

RSU Decision Framework: 4-Step Policy for Every Vesting Date

Once you’ve decided whether to sell now, sell part, or hold, the next step is simple: use the same rule at every vest. That may sound basic, but consistency may matter more than trying to make a brand-new call each time.

A 4-step RSU policy you can apply at every vest

Run through these four checks at each vesting date:

- Measure total exposure. Compare employer stock across all accounts with your preset cap. Under 5% may need no action. At 5%–10%, some people trim. At 10%–20%, many people treat it as an active diversification issue. Above 20% may point to concentrated risk.

- Confirm cash needs. Check that you have 6–12 months of emergency cash and enough set aside for near-term goals, like a home purchase or debt payoff, before holding shares.

- Estimate the real tax cost. Employers often withhold 22% for federal taxes on RSUs, which may leave a gap for people in higher tax brackets. It may help to know that shortfall before vesting day.

- Apply your standing rule. Set the rule ahead of time, then use it at every vest.

This policy tends to work best when you can see your full employer-stock exposure across accounts.

How Mezzi supports ongoing RSU decisions

Mezzi connects your accounts in read-only mode, with the goal of showing employer-stock exposure, wash sale risk, and tax lots in one place.

Key takeaways

If you only keep a few points in mind, these are the ones to keep close:

- Vesting creates ordinary income equal to the vest-date fair market value.

- Long-term capital gains apply only to post-vest appreciation held for more than one year.

- Concentration risk often may matter more than tax optimization. Waiting 12 months for preferential rates may mean carrying single-stock risk for a full year. That tradeoff may make more sense when your existing exposure is already low.

- A rules-based policy may keep exposure from drifting higher over time. The point is consistency. Without a standing rule, exposure may grow quietly with each new vest.

FAQs

How do I know if I have too much company stock?

Ask yourself this: if this vest showed up as cash today, would you use that money to buy your employer’s stock? If the answer may be no, you may already hold more company stock than you’d pick on your own.

A common rule of thumb is that once a single stock reaches 10% of your liquid net worth, it may deserve a closer look. At 20%, some people may view the risk as excessive. And with employer stock, there’s an extra layer: your income and your career may already be tied to the same company. Owning more shares may stack that risk even further.

What if my RSU tax withholding is too low?

If your RSU tax withholding may be too low, you may end up with a tax bill in April or underpayment penalties. A common reason: employers often withhold at the flat 22% supplemental wage rate, which may be too low if you're in the 32% to 37% bracket.

Because RSUs are taxable when they vest, that gap may show up whether you hold the shares or sell them right away. Some people calculate the shortfall, then cover it in one of a few ways:

- Making estimated tax payments

- Increasing payroll withholding

- Setting aside cash

The main idea is pretty simple: the withholding on vesting may not match your full tax rate, and that difference may need to be covered elsewhere.

When does holding vested RSUs make sense?

Holding vested RSUs may make sense only when it reflects a deliberate investment choice, not a default habit.

Some people may choose to hold when the position represents a small share of net worth, often under 10%, and when they may have a high risk tolerance, a long time horizon, or a multi-year tax or liquidity plan. That might include waiting to sell in a year when ordinary income may be taxed at a lower rate.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.